|

市場調査レポート

商品コード

1684586

ヘルスケア包装の市場機会、成長促進要因、産業動向分析、2025年~2034年予測Healthcare Packaging Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| ヘルスケア包装の市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年01月07日

発行: Global Market Insights Inc.

ページ情報: 英文 210 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

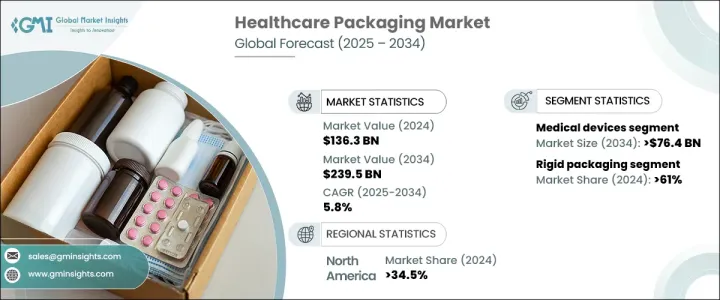

ヘルスケア包装の世界市場は2024年に1,363億米ドルとなり、2025年から2034年までのCAGRは5.8%と安定した成長が予測されています。

この市場の主な要因は、革新的で安全かつ持続可能な包装ソリューションに対するニーズの高まりです。近年、ヘルスケア業界は、生物製剤や特殊医薬品の特殊なニーズに対応するため、先進包装技術を採用しています。これと並行して、発展途上地域におけるヘルスケアへのアクセスが改善されつつあり、効果的かつ効率的な包装への需要が高まっています。

さらに、医薬品eコマースの台頭は、安全な輸送と保管をサポートする包装ソリューションに新たな機会をもたらしています。スマート包装の統合は、正確な投与とリアルタイムの情報提供により、患者のコンプライアンスをさらに強化しています。この動向はまた、サプライチェーンの効率を最適化し、コストを削減し、製品のトレーサビリティを向上させています。ヘルスケア分野が進化を続ける中、包装市場は医薬品・医療製品の安全性と品質を確保する上で重要な役割を果たすと思われます。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025年~2034年 |

| 開始金額 | 1,363億米ドル |

| 予測金額 | 2,395億米ドル |

| CAGR | 5.8% |

ヘルスケア包装市場は、硬質包装と軟質包装の2つの主要セグメントに分けられます。硬質包装が最大の市場シェアを占め、2024年には61%を占めました。このセグメントの優位性は、製品を保護し、繊細なヘルスケア製品の完全性を維持する能力によるところが大きいです。硬質包装にはポリプロピレンやポリカーボネートのような高性能材料が使用されることが多く、厳しいヘルスケアコンプライアンス規制を満たすために不可欠です。成形技術の継続的な進歩により、メーカーは軽量でありながら耐久性のある容器を製造できるようになり、必要な強度と保護を維持しながら輸送コストの削減に貢献しています。こうした材料とデザインの継続的な進化により、硬質包装は多くのヘルスケア用途で好ましい選択肢であり続けています。

エンドユーザー用途を見ると、ヘルスケア包装市場は医薬品と医療機器に分類されます。医療機器分野は最も高い成長率が見込まれており、CAGRは6.5%と予測されています。このセグメントは、医療機器技術の革新と、無菌で耐久性があり、ユーザーフレンドリーな包装ソリューションに対する需要の増加により、2034年までに764億米ドルに達すると予想されています。医療機器包装は、診断ツールや手術器具からインプラントに至るまで、幅広い製品の無菌性、耐久性、使いやすさといった厳しい要件を満たす必要があります。より先進的な医療機器が市場に登場するにつれ、包装ソリューションもそれに合わせて進化し、最大限の安全性と機能性を確保する必要があります。

北米では、ヘルスケア包装市場が優位性を維持し、2024年には市場シェアの34.5%を占めると予想されます。米国では、医療製品の技術進歩や患者の安全性重視の高まりを背景に、ヘルスケア分野における先進包装ソリューションの需要が大幅に増加しています。改ざん防止包装や子供が開けにくい包装のような技術革新は、医薬品と一般用医薬品の両方で高い需要を見ています。在宅ヘルスケアの台頭も、プレフィルドシリンジやブリスターパックなど、より便利で使いやすい包装形態へのニーズに拍車をかけています。これらの開発は、ヘルスケア業界全体でより効率的で効果的な包装ソリューションを求める幅広い動向を反映しています。

目次

第1章 調査手法と調査範囲

- 市場範囲と定義

- 基本推定と計算

- 予測計算

- データソース

- 一次

- 二次

- 有料ソース

- 公的ソース

第2章 エグゼクティブサマリー

第3章 業界洞察

- 業界エコシステム分析

- バリューチェーンに影響を与える要因

- 変革

- 将来の展望

- メーカー

- 流通業者

- 利益率分析

- 主なニュースと取り組み

- 規制状況

- 影響要因

- 成長促進要因

- リサイクル可能で持続可能な医療用包装の革新

- 在宅ヘルスケアと自己投与の動向の拡大

- 患者の安全とコンプライアンス包装に対する意識の高まり

- 先進包装ソリューションを必要とする生物製剤とバイオシミラーの成長

- 慢性疾患の増加による特殊包装ソリューションの需要拡大

- 業界の潜在的リスク・課題

- 新たな生物学的製剤の包装開発における課題

- ヘルスケア包装規制の地域格差

- 成長促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業市場シェア分析

- 競合のポジショニングマトリックス

- 戦略展望マトリックス

第5章 市場推計・予測:材料別、2021年~2034年

- 主要動向

- プラスチック

- 紙・板紙

- 金属

- ガラス

第6章 市場推計・予測:製品タイプ別、2021年~2034年

- 主要動向

- 硬質包装

- ボトル

- 箱・カートン

- トレイ

- プレフィラブル吸入器

- プレフィラブルシリンジ

- バイアル・アンプル

- 瓶・キャニスター

- その他

- 軟質包装

- バッグ・パウチ

- チューブ

- フィルム・ラミネート

- その他

第7章 市場推計・予測:包装タイプ別、2021年~2034年

- 主要動向

- 一次包装

- 二次包装

- 三次包装

第8章 市場推計・予測:最終用途別、2021-2034年

- 主要動向

- 医薬品

- 経口剤

- 注射剤

- 外用薬

- 点鼻薬

- その他

- 医療機器

- 使い捨て消耗品

- 治療機器

- モニタリング診断機器

- その他

第9章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- ラテンアメリカ

- ブラジル

- メキシコ

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第10章 企業プロファイル

- 3M

- Adelphi Group

- Amcor

- Aptar CSP Technologies

- Berry Global

- CCL Industries

- Constantia Flexibles

- DS Smith

- DuPont

- Eastman Chemical

- Gerresheimer

- Graphic Packaging

- Huhtamaki

- Mayr-Melnhof Karton

- Nelipak

- Oliver Healthcare

- Printpack

- ProAmpac

- Schott Pharma

- Sealed Air

- SGD Pharma

- Solventum

- Sonoco Products

- West Pharmaceutical

- WestRock

The Global Healthcare Packaging Market was valued at USD 136.3 billion in 2024, with projections indicating a steady growth rate of 5.8% CAGR from 2025 to 2034. This market is primarily fueled by the growing need for innovative, secure, and sustainable packaging solutions. In recent years, the healthcare industry has been embracing advanced packaging technologies to meet the specific needs of biologics and specialty drugs. Alongside this, access to healthcare in developing regions is improving, driving an increase in demand for effective and efficient packaging.

Additionally, the rise of pharmaceutical e-commerce is providing new opportunities for packaging solutions that support safe transportation and storage. The integration of smart packaging is further enhancing patient compliance by ensuring accurate dosing and providing real-time information. This trend is also optimizing supply chain efficiency, reducing costs, and improving product traceability. As the healthcare sector continues to evolve, the packaging market will play a critical role in ensuring the safety and quality of pharmaceutical and medical products.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $136.3 Billion |

| Forecast Value | $239.5 Billion |

| CAGR | 5.8% |

The healthcare packaging market is divided into two main segments: rigid and flexible packaging. Rigid packaging accounts for the largest market share, holding 61% in 2024. The dominance of this segment is largely due to its ability to protect products and maintain the integrity of sensitive healthcare products. Rigid packaging often employs high-performance materials like polypropylene and polycarbonate, essential for meeting stringent healthcare compliance regulations. With ongoing advancements in molding technologies, manufacturers are able to produce lightweight yet durable containers, helping reduce transportation costs while maintaining the necessary strength and protection. This continued evolution in materials and design is helping rigid packaging remain the preferred choice for many healthcare applications.

When examining end-user applications, the healthcare packaging market is categorized into pharmaceuticals and medical devices. The medical devices segment is expected to experience the highest growth rate, with a projected CAGR of 6.5%. This segment is expected to reach USD 76.4 billion by 2034, driven by innovations in medical device technology and the increasing demand for sterile, durable, and user-friendly packaging solutions. Medical device packaging must meet the demanding requirements of sterility, durability, and usability for a wide array of products, from diagnostic tools and surgical instruments to implants. As more advanced medical devices enter the market, the packaging solutions will need to evolve accordingly to ensure maximum safety and functionality.

In North America, the healthcare packaging market is expected to maintain its dominance, accounting for 34.5% of the market share in 2024. The U.S. is experiencing a significant increase in the demand for advanced packaging solutions within the healthcare sector, driven by technological advancements in medical products and a growing emphasis on patient safety. Innovations like tamper-evident and child-resistant packaging are seeing high demand for both pharmaceutical and over-the-counter products. The rise of home healthcare is also fueling the need for more convenient, user-friendly packaging formats, such as prefilled syringes and blister packs. These developments reflect a broader trend toward more efficient and effective packaging solutions across the healthcare industry.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Disruptions

- 3.1.3 Future outlook

- 3.1.4 Manufacturers

- 3.1.5 Distributors

- 3.2 Profit margin analysis

- 3.3 Key news & initiatives

- 3.4 Regulatory landscape

- 3.5 Impact forces

- 3.5.1 Growth drivers

- 3.5.1.1 Innovation in recyclable and sustainable medical packaging

- 3.5.1.2 Expanding home healthcare and self-administration trends

- 3.5.1.3 Rising awareness about patient safety and compliance packaging

- 3.5.1.4 Growth in biologics and biosimilars requiring advanced packaging solutions

- 3.5.1.5 Rising prevalence of chronic diseases boosting demand for specialized packaging solutions

- 3.5.2 Industry pitfalls & challenges

- 3.5.2.1 Challenges in developing packaging for emerging biologic therapies

- 3.5.2.2 Regional disparities in healthcare packaging regulations

- 3.5.1 Growth drivers

- 3.6 Growth potential analysis

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Material, 2021-2034 (USD Billion & Kilo Tons)

- 5.1 Key trends

- 5.2 Plastic

- 5.3 Paper & paperboard

- 5.4 Metal

- 5.5 Glass

Chapter 6 Market Estimates & Forecast, By Product Type, 2021-2034 (USD Billion & Kilo Tons)

- 6.1 Key trends

- 6.2 Rigid packaging

- 6.2.1 Bottles

- 6.2.2 Boxes & cartons

- 6.2.3 Trays

- 6.2.4 Pre-fillable inhalers

- 6.2.5 Pre-fillable syringes

- 6.2.6 Vials & ampoules

- 6.2.7 Jars & canisters

- 6.2.8 Others

- 6.3 Flexible packaging

- 6.3.1 Bags & pouches

- 6.3.2 Tubes

- 6.3.3 Films & laminates

- 6.3.4 Others

Chapter 7 Market Estimates & Forecast, By Packaging Type, 2021-2034 (USD Billion & Kilo Tons)

- 7.1 Key trends

- 7.2 Primary packaging

- 7.3 Secondary packaging

- 7.4 Tertiary packaging

Chapter 8 Market Estimates & Forecast, By End Use, 2021-2034 (USD Billion & Kilo Tons)

- 8.1 Key trends

- 8.2 Pharmaceuticals

- 8.2.1 Oral drug

- 8.2.2 Injectables

- 8.2.3 Topical drug

- 8.2.4 Nasal drug

- 8.2.5 Others

- 8.3 Medical devices

- 8.3.1 Disposable consumables

- 8.3.2 Therapeutic equipment

- 8.3.3 Monitoring & diagnostic equipment

- 8.3.4 Others

Chapter 9 Market Estimates & Forecast, By Region, 2021-2034 (USD Billion & Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 Australia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 3M

- 10.2 Adelphi Group

- 10.3 Amcor

- 10.4 Aptar CSP Technologies

- 10.5 Berry Global

- 10.6 CCL Industries

- 10.7 Constantia Flexibles

- 10.8 DS Smith

- 10.9 DuPont

- 10.10 Eastman Chemical

- 10.11 Gerresheimer

- 10.12 Graphic Packaging

- 10.13 Huhtamaki

- 10.14 Mayr-Melnhof Karton

- 10.15 Nelipak

- 10.16 Oliver Healthcare

- 10.17 Printpack

- 10.18 ProAmpac

- 10.19 Schott Pharma

- 10.20 Sealed Air

- 10.21 SGD Pharma

- 10.22 Solventum

- 10.23 Sonoco Products

- 10.24 West Pharmaceutical

- 10.25 WestRock