|

市場調査レポート

商品コード

1684579

エポキシ活性希釈剤の市場機会、成長促進要因、産業動向分析、2025年~2034年予測Epoxy Active Diluent Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| エポキシ活性希釈剤の市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年01月06日

発行: Global Market Insights Inc.

ページ情報: 英文 235 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

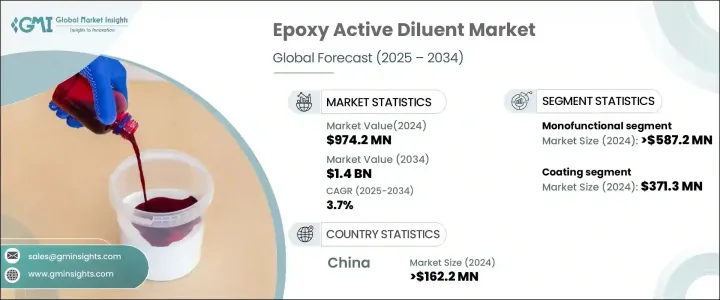

エポキシ活性希釈剤の世界市場は2024年に9億7,420万米ドルとなり、2025年から2034年にかけてCAGR3.7%で成長すると予測されています。

コーティング、接着剤、複合材料におけるエポキシ樹脂の需要の増加が、この成長の原動力となっています。これらの希釈剤は樹脂の粘度を下げ、加工や塗布を容易にするという重要な役割を果たしています。耐久性と効率を向上させる高性能材料を求める製造業者によって、その用途はさまざまな産業で拡大しています。長持ちする保護性能と美観を兼ね備えた優れた塗料を求める動きは、市場の拡大にさらに拍車をかけています。

環境に優しい製品へのシフトが市場情勢を形成しています。エポキシ活性希釈剤は、従来の溶剤よりも揮発性有機化合物(VOC)の排出量が少ないため、企業が持続可能性を重視する中で好ましい選択肢となっています。さらに、バイオベースの希釈剤の進歩は、世界の規制に合わせて、環境に配慮した代替品を提供しています。産業界が性能と環境基準を満たすために革新的な配合を取り入れることで、市場は着実に成長する見込みです。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025年~2034年 |

| 開始金額 | 9億7,420万米ドル |

| 予測金額 | 14億米ドル |

| CAGR | 3.7% |

単官能性セグメントは、2024年に5億8,720万米ドル以上を生み出し、2034年までCAGR3.9%で拡大します。その優位性は、工業用途における汎用性と信頼性に起因します。これらの希釈剤は、より優れた硬化特性、耐薬品性、接着性を保証するため、高精度の用途に不可欠です。単官能性希釈剤の需要は、粘度制御と加工効率の向上が好まれる産業界で牽引され続けています。その予測可能な性能により、特殊なコーティングや配合に不可欠であり、市場でのリーダーシップを強化しています。

2024年の売上高は3億7,130万米ドルで塗料分野が市場をリードし、2025年から2034年にかけてCAGR3.8%で成長すると予想されています。エポキシ系コーティングの広範な採用は、優れた接着性、耐久性、環境要因への耐性を提供する能力に起因しています。製品の寿命と美観を向上させるために、エポキシ系コーティングへの依存度が高まっています。メーカーが効率性と持続可能性を優先するにつれて、コーティングの需要は増加の一途をたどっており、主要な用途分野としての地位を固めています。

中国は2024年に1億6,220万米ドルを超え、CAGR3.4%で成長すると予想されています。世界市場における中国の支配的地位は、強力な製造基盤とコスト効率の高い高性能材料に対する需要の高まりによってもたらされています。同国で進行中の工業化とインフラプロジェクトは、エポキシ樹脂の大幅な消費に寄与しています。さらに、持続可能性を促進する規制措置により、低VOCで環境に優しいソリューションへの移行が加速しています。中国は依然として生産と消費の主要プレーヤーであり、世界市場における影響力を強めています。

目次

第1章 調査手法と調査範囲

- 市場範囲と定義

- 基本推定と計算

- 予測計算

- データソース

- 一次

- 二次

- 有料ソース

- 公的ソース

第2章 エグゼクティブサマリー

第3章 業界洞察

- 業界エコシステム分析

- バリューチェーンに影響を与える要因

- 利益率分析

- 変革

- 将来の展望

- メーカー

- 流通業者

- サプライヤーの状況

- 利益率分析

- 主要ニュース

- 規制状況

- 影響要因

- 成長促進要因

- 自動車・航空宇宙分野での軽量材料需要の増加

- 建設・インフラプロジェクトの拡大

- 業界の潜在的リスク・課題

- 原材料価格の変動

- 成長促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業市場シェア分析

- 競合のポジショニングマトリックス

- 戦略展望マトリックス

第5章 市場推計・予測:タイプ別、2021年~2034年

- 主要動向

- 単官能性

- 二官能性

- その他

第6章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- コーティング

- 工業用塗料

- マリンコーティング

- 保護塗料

- 接着剤・シーリング剤

- 構造用接着剤

- 非構造用接着剤

- 複合材料

- 電気・電子

- 建築

- その他

第7章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- ラテンアメリカ

- ブラジル

- メキシコ

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第8章 企業プロファイル

- Adeka Corporation

- Aditya Birla Chemicals

- Anhui Hengyuan(Group)

- EMS-GRILTECH

- Evonik Industries

- Hexion Inc.

- Hubei Green Home Chemical

- Huntsman Corporation

- Kukdo Chemical

- Leuna Harze GmbH

- Olin Corporation

- Sanmu Group

The Global Epoxy Active Diluent Market was valued at USD 974.2 million in 2024 and is projected to grow at a CAGR of 3.7% from 2025 to 2034. The increasing demand for epoxy resins in coatings, adhesives, and composites is driving this growth. These diluents play a critical role in reducing resin viscosity, making them easier to process and apply. Their use is expanding across multiple industries as manufacturers seek high-performance materials that enhance durability and efficiency. The push for superior coatings that offer long-lasting protection and aesthetic appeal is further fueling market expansion.

The shift toward environmentally friendly products is shaping the market landscape. Epoxy active diluents emit lower levels of volatile organic compounds (VOCs) than traditional solvents, making them a preferred choice as companies focus on sustainability. Additionally, advancements in bio-based diluents are providing eco-conscious alternatives, aligning with global regulations. The market is poised to grow steadily as industries integrate innovative formulations to meet performance and environmental standards.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $974.2 million |

| Forecast Value | $1.4 billion |

| CAGR | 3.7% |

The monofunctional segment generated over USD 587.2 million in 2024 and is set to expand at a CAGR of 3.9% through 2034. Its dominance is attributed to versatility and reliability in industrial applications. These diluents ensure better curing properties, chemical resistance, and adhesion, making them essential for high-precision applications. Industries favoring controlled viscosity and improved processing efficiency continue to drive the demand for monofunctional diluents. Their predictable performance makes them indispensable for specialized coatings and formulations, reinforcing their market leadership.

The coatings segment led the market with USD 371.3 million in revenue in 2024 and is expected to grow at a 3.8% CAGR from 2025 to 2034. The widespread adoption of epoxy-based coatings stems from their ability to provide excellent adhesion, durability, and resistance to environmental factors. Industries increasingly rely on these coatings to enhance product longevity and aesthetic value. As manufacturers prioritize efficiency and sustainability, demand for coatings continues to rise, solidifying their position as the leading application segment.

China accounted for over USD 162.2 million in 2024 and is expected to grow at a 3.4% CAGR. Its dominant position in the global market is driven by a strong manufacturing base and rising demand for cost-effective, high-performance materials. The country's ongoing industrialization and infrastructure projects contribute to substantial consumption of epoxy resins. Moreover, regulatory measures promoting sustainability are accelerating the transition toward low-VOC and eco-friendly solutions. China remains a key player in production and consumption, strengthening its influence in the global market.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Key news & initiatives

- 3.5 Regulatory landscape

- 3.6 Impact forces

- 3.6.1 Growth drivers

- 3.6.1.1 Increasing demand for lightweight materials in automotive and aerospace

- 3.6.1.2 Expansion of construction and infrastructure projects

- 3.6.2 Industry pitfalls & challenges

- 3.6.2.1 Fluctuating raw material prices

- 3.6.1 Growth drivers

- 3.7 Growth potential analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Type, 2021-2034 (USD Million) (Kilo Tons)

- 5.1 Key trends

- 5.2 Monofunctional

- 5.3 Difunctional

- 5.4 Others

Chapter 6 Market Estimates & Forecast, By Application, 2021-2034 (USD Million) (Kilo Tons)

- 6.1 Key trends

- 6.2 Coatings

- 6.2.1 Industrial coatings

- 6.2.2 Marine coatings

- 6.2.3 Protective coatings

- 6.3 Adhesives and sealants

- 6.3.1 Structural adhesives

- 6.3.2 Non-structural adhesives

- 6.4 Composite material

- 6.5 Electrical and electronics

- 6.6 Construction

- 6.7 Others

Chapter 7 Market Estimates & Forecast, By Region, 2021-2034 (USD Million) (Kilo Tons)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 UK

- 7.3.2 Germany

- 7.3.3 France

- 7.3.4 Italy

- 7.3.5 Spain

- 7.3.6 Russia

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 India

- 7.4.3 Japan

- 7.4.4 South Korea

- 7.4.5 Australia

- 7.5 Latin America

- 7.5.1 Brazil

- 7.5.2 Mexico

- 7.6 MEA

- 7.6.1 South Africa

- 7.6.2 Saudi Arabia

- 7.6.3 UAE

Chapter 8 Company Profiles

- 8.1 Adeka Corporation

- 8.2 Aditya Birla Chemicals

- 8.3 Anhui Hengyuan (Group)

- 8.4 EMS-GRILTECH

- 8.5 Evonik Industries

- 8.6 Hexion Inc.

- 8.7 Hubei Green Home Chemical

- 8.8 Huntsman Corporation

- 8.9 Kukdo Chemical

- 8.10 Leuna Harze GmbH

- 8.11 Olin Corporation

- 8.12 Sanmu Group