|

市場調査レポート

商品コード

1684578

アルミ缶の市場機会、成長促進要因、産業動向分析、2025年~2034年予測Aluminum Cans Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| アルミ缶の市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年01月06日

発行: Global Market Insights Inc.

ページ情報: 英文 200 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

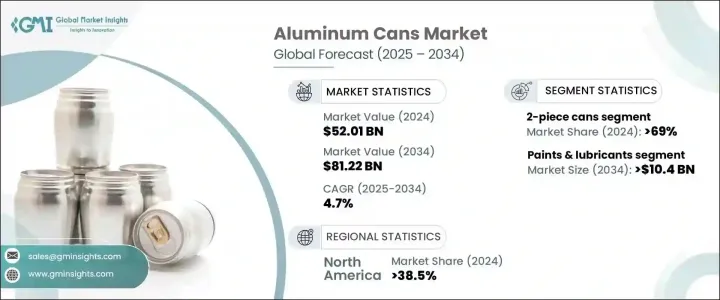

世界のアルミ缶市場は、2024年に520億1,000万米ドルと評価され、2025年から2034年にかけてCAGR4.7%で成長すると予測されています。

持続可能性と利便性が市場動向を形成する主な要因であり、アルミ缶はリサイクル可能で環境に優しい利点があることから支持を集めています。消費者の選好の変化が需要をさらに刺激し、プレミアム飲料のアルミ缶パッケージ化が進んでいます。健康志向の消費者は高品質の製品を求めるため、アルミ缶入りのプレミアムウォーター、クラフトソーダ、エナジードリンクの需要が急増しています。さらに、ブランドは世界の持続可能性の目標に沿い、プラスチック廃棄物を減らすためにアルミ缶を採用しています。印刷やブランディングの技術的進歩も製品の魅力を高め、飲料メーカーにとってアルミ缶は魅力的な選択肢となっています。このシフトは、業界全体で持続可能な包装ソリューションへの動きが広がっていることを反映しています。

市場は製品タイプ別に1ピース缶、2ピース缶、3ピース缶に区分され、2ピース缶が業界をリードし、2024年の市場シェアは69%を超えました。これらの缶は、費用対効果、軽量構造、材料要件の削減により、生産コストと環境への影響を低減するため、人気を集めています。そのデザインは輸送費と二酸化炭素排出を最小限に抑え、世界的に好まれる選択肢となっています。飲料分野では、その耐久性と酸素や汚染物質から保護する能力により、2ピースアルミ缶が広く採用されており、より長い賞味期限を保証しています。ブランド化技術の向上は、特にアルミ缶の需要が増え続けているアルコール飲料分野で、市場の成長をさらに促進しています。リサイクル効率が高く、国際的な環境規制を遵守しているため、アルミ缶はメーカーや消費者に好まれる選択肢となっています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025年~2034年 |

| 開始金額 | 520億1,000万米ドル |

| 予測金額 | 812億2,000万米ドル |

| CAGR | 4.7% |

エンドユーザー別では、食品、飲料、パーソナルケア・化粧品、医薬品、塗料・潤滑油、その他に分類されます。塗料・潤滑油分野はCAGR8.1%以上で成長し、2034年には104億米ドルを超えると予想されます。アルミ缶は、その軽量性、漏れ防止、耐腐食性により、製品の完全性を維持するのに役立つため、この分野で広く使用されています。代替包装と比較して、アルミ缶は、持続可能性への取り組みに沿いながら、安全な保管と輸送を保証する、よりコスト効率の高いソリューションを提供します。高性能のコーティング剤や潤滑剤に対する需要の増加は、アルミ缶の採用をさらに加速させています。アルミ缶は製品を過酷な条件下から保護し、乾燥や漏れを防ぐからです。包装技術の先進化により、こぼれにくい設計や耐タンパー性も強化され、アルミ缶は産業分野でますます好まれる選択肢となっています。都市化と工業化の動向の高まりは、効率的な包装ソリューションへの需要を高め、市場拡大に寄与しています。

2024年の市場は、米国の旺盛な需要に牽引されて北米が38.5%のシェアを占め、市場をリードしました。消費者は持続可能でリサイクル可能な包装をますます好むようになっており、飲料メーカーは軽量容器とリサイクル技術の向上に注力するようになっています。プレミアム飲料の台頭は、カスタマイズされた視覚に訴えるアルミ缶の需要をさらに促進しています。企業のプラスチック離れが進むにつれ、アルミ包装が脚光を浴びています。インドでは、環境意識の高まりとコスト効率の高い製造工程により、市場が急成長しています。地元メーカーは、国内外の市場に適した軽量でリサイクル可能な缶を開発しています。持続可能性と手頃な価格への注目の高まりは、特に清涼飲料とビール業界において市場の成長を持続させると予想されます。

目次

第1章 調査手法と調査範囲

- 市場範囲と定義

- 基本推定と計算

- 予測計算

- データソース

- 一次

- 二次

- 有料ソース

- 公的ソース

第2章 エグゼクティブサマリー

第3章 業界洞察

- 業界エコシステム分析

- バリューチェーンに影響を与える要因

- 変革

- 将来の展望

- メーカー

- 流通業者

- 利益率分析

- 主なニュースと取り組み

- 規制状況

- 影響要因

- 成長促進要因

- プレミアム飲料ブランドがアルミ缶の需要を牽引

- 鮮度保持パッケージとしてのアルミ缶に対するポジティブな認識

- アルミ缶のリサイクル率の高さが市場の需要を高める

- レディ・トゥ・ドリンク(RTD)飲料の需要急増

- 飲料ブランドと包装の戦略的パートナーシップ

- 業界の潜在的リスク・課題

- 輸送中の缶のへこみや損傷に対する脆弱性

- 包装基準の規制障壁と遵守コスト

- 成長促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業市場シェア分析

- 競合のポジショニングマトリックス

- 戦略展望マトリックス

第5章 市場推計・予測:製品タイプ別、2021年~2034年

- 主要動向

- 1ピース缶

- 2ピース缶

- 3ピース缶

第6章 市場推計・予測:容量別、2021年~2034年

- 主要動向

- 200ml以下

- 201~450ml

- 451~700ml

- 701~1000ml

- 1000ml以上

第7章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 食品

- 飲料

- パーソナルケア・化粧品

- 医薬品

- 塗料・潤滑油

- その他

第8章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- ラテンアメリカ

- ブラジル

- メキシコ

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第9章 企業プロファイル

- Ajanta Bottle

- Albott Containers

- Baixicans

- Ball Corporation

- Canpack

- CCL Industries

- Ceylon Beverage Can

- Crown Holdings

- Envases Group

- GZI Industries

- Nampak

- Orora Packaging

- Scan Holdings

- Shiba Containers

- Silgan Containers

- Swan Industries

- Thai Beverage Can

- Toyo Seikan

The Global Aluminum Cans Market, valued at USD 52.01 billion in 2024, is set to grow at a CAGR of 4.7% from 2025 to 2034. Sustainability and convenience are key drivers shaping market trends, as aluminum cans gain traction due to their recyclability and eco-friendly benefits. Changing consumer preferences have further fueled demand, with premium beverages increasingly packaged in aluminum cans. Health-conscious consumers seek high-quality products, leading to a surge in demand for premium water, craft sodas, and energy drinks in aluminum packaging. Additionally, brands are adopting aluminum cans to align with global sustainability goals and reduce plastic waste. Technological advancements in printing and branding also enhance product appeal, making aluminum cans an attractive choice for beverage companies. This shift reflects a broader move toward sustainable packaging solutions across industries.

The market is segmented by product type into 1-piece, 2-piece, and 3-piece cans, with 2-piece cans leading the industry, holding over 69% market share in 2024. These cans are gaining popularity due to their cost-effectiveness, lightweight structure, and reduced material requirements, which lower production costs and environmental impact. Their design minimizes transportation expenses and carbon emissions, making them a preferred choice globally. The beverage sector widely adopts 2-piece aluminum cans for their durability and ability to protect against oxygen and contaminants, ensuring a longer shelf life. Improved branding techniques further enhance market growth, particularly in the alcoholic beverage segment, where demand for aluminum cans continues to rise. The recycling efficiency and adherence to international environmental regulations make these cans a preferred option among manufacturers and consumers.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $52.01 Billion |

| Forecast Value | $81.22 Billion |

| CAGR | 4.7% |

By end-user, the market is categorized into food, beverage, personal care & cosmetics, pharmaceuticals, paints & lubricants, and others. The paints & lubricants segment is expected to grow at a CAGR of over 8.1% and exceed USD 10.4 billion by 2034. Aluminum cans are widely used in this sector due to their lightweight, leak-proof, and corrosion-resistant properties, which help maintain product integrity. Compared to alternative packaging, aluminum cans offer a more cost-effective solution that ensures safe storage and transportation while aligning with sustainability initiatives. Increasing demand for high-performance coatings and lubricants has further accelerated the adoption of aluminum cans, as they protect products from exposure to harsh conditions and prevent drying or leakage. Advancements in packaging technology have also enhanced spill-proof designs and tamper resistance, making aluminum cans an increasingly preferred choice in the industrial sector. The rising trend of urbanization and industrialization is driving higher demand for efficient packaging solutions, contributing to market expansion.

North America led the market in 2024, holding a 38.5% share, driven by strong demand in the United States. Consumers increasingly prefer sustainable and recyclable packaging, prompting beverage manufacturers to focus on lightweight containers and improved recycling technologies. The rise of premium beverages has further fueled demand for customized and visually appealing aluminum cans. As businesses shift away from plastic, aluminum packaging has gained prominence. In India, the market is experiencing rapid growth due to rising environmental awareness and cost-effective manufacturing processes. Local manufacturers are developing lightweight, recyclable cans suitable for domestic and international markets. The increasing focus on sustainability and affordability is expected to sustain market growth, particularly in the soft drink and beer industries.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Disruptions

- 3.1.3 Future outlook

- 3.1.4 Manufacturers

- 3.1.5 Distributors

- 3.2 Profit margin analysis

- 3.3 Key news & initiatives

- 3.4 Regulatory landscape

- 3.5 Impact forces

- 3.5.1 Growth drivers

- 3.5.1.1 Premium beverage brands driving demand for aluminum cans

- 3.5.1.2 Positive perception of aluminum cans as a freshness retention packaging

- 3.5.1.3 High recycling rate of aluminum cans enhancing market demand

- 3.5.1.4 Surge in demand for ready-to-drink (RTD) beverages

- 3.5.1.5 Strategic partnerships between beverage brands and packaging

- 3.5.2 Industry pitfalls & challenges

- 3.5.2.1 Vulnerability of cans to denting and damage during transportation

- 3.5.2.2 Regulatory barriers and compliance costs for packaging standards

- 3.5.1 Growth drivers

- 3.6 Growth potential analysis

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Product Type, 2021-2034 (USD Billion & Kilo Tons)

- 5.1 Key trends

- 5.2 1-piece cans

- 5.3 2-piece cans

- 5.4 3-piece cans

Chapter 6 Market Estimates & Forecast, By Capacity, 2021-2034 (USD Billion & Kilo Tons)

- 6.1 Key trends

- 6.2 Up to 200 ml

- 6.3 201 to 450 ml

- 6.4 451 to 700 ml

- 6.5 701 to 1000 ml

- 6.6 more than 1000 ml

Chapter 7 Market Estimates & Forecast, By End Use, 2021-2034 (USD Billion & Kilo Tons)

- 7.1 Key trends

- 7.2 Food

- 7.3 Beverage

- 7.4 Personal care & cosmetic

- 7.5 Pharmaceutical

- 7.6 Paints & lubricants

- 7.7 Others

Chapter 8 Market Estimates & Forecast, By Region, 2021-2034 (USD Billion & Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 UK

- 8.3.2 Germany

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Russia

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 South Korea

- 8.4.5 Australia

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.6 MEA

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Ajanta Bottle

- 9.2 Albott Containers

- 9.3 Baixicans

- 9.4 Ball Corporation

- 9.5 Canpack

- 9.6 CCL Industries

- 9.7 Ceylon Beverage Can

- 9.8 Crown Holdings

- 9.9 Envases Group

- 9.10 GZI Industries

- 9.11 Nampak

- 9.12 Orora Packaging

- 9.13 Scan Holdings

- 9.14 Shiba Containers

- 9.15 Silgan Containers

- 9.16 Swan Industries

- 9.17 Thai Beverage Can

- 9.18 Toyo Seikan