|

市場調査レポート

商品コード

1684530

ラインプリンターの市場機会、成長促進要因、産業動向分析、2025~2034年予測Line Printer Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| ラインプリンターの市場機会、成長促進要因、産業動向分析、2025~2034年予測 |

|

出版日: 2025年01月02日

発行: Global Market Insights Inc.

ページ情報: 英文 220 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

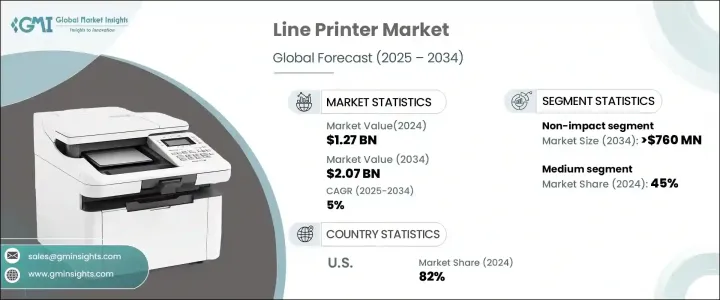

2024年に12億7,000万米ドルと評価された世界のラインプリンター市場は、2025年から2034年にかけてCAGR 5%と予測され、着実な成長軌道に乗っています。

この上昇動向は、印刷技術の急速な進歩と、様々な業界における大量印刷ソリューションへのニーズの高まりによって後押しされています。ラインプリンターは、効率的で大規模な印刷に依存して業務を合理化する企業や組織にとって、依然として不可欠です。これらのデバイスは、明確で正確な文書作成が重要な物流、製造、小売、ビジネスサービスなどの分野で特に好まれています。企業が費用対効果の高い高速印刷ソリューションを求め続けていることから、ラインプリンターの需要は今後数年間で大幅に増加すると予想されます。さらに、新技術の統合によってラインプリンターの性能は向上し、効率性と正確性を優先する環境では不可欠なものとなっています。

市場は、インパクト型ラインプリンターとノンインパクト型ラインプリンターの2つに大別されます。非衝撃型ラインプリンターは、2024年に7億6,000万米ドルを生み出し、今後数年間で大幅な成長が予測されています。これらのプリンターは、感熱印刷や静電印刷などの高度な技術によって達成される優れた印刷品質によって際立っています。これらの技術が提供する精度は高品質の出力を保証し、ノンインパクト・プリンターを医薬品、自動車、エレクトロニクスなどの産業で普及させています。これらの分野では、鮮明なラベル、コード、小さなテキストを作成する能力が不可欠であり、ノンインパクトプリンタはこれらの要求をシームレスに満たします。企業が印刷物の精度と品質を優先し続ける中、ノンインパクト・ラインプリンターの採用はさらに加速すると予想されます。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 12億7,000万米ドル |

| 予測金額 | 20億7,000万米ドル |

| CAGR | 5% |

印刷速度別に分類すると、ラインプリンターは低速タイプ、中速タイプ、高速タイプに分かれます。2024年に市場の45%を占めた中速ラインプリンターは、今後も旺盛な需要を維持するとみられます。これらのプリンターは、手頃な価格、スピード、性能のバランスが絶妙で、定期的で費用対効果の高い印刷ソリューションを必要とする企業にとって好ましい選択肢となっています。大量の報告書、出荷ラベル、請求書の作成などの作業では効率性が求められるが、中速ラインプリンターはまさにそれを実現します。ビジネスの拡大に伴い、信頼性が高く拡張性の高い印刷ソリューションへのニーズは高まり続けており、中速ラインプリンターの需要はさらに高まっています。

2024年には、北米が世界のラインプリンター市場で82%の圧倒的シェアを獲得しました。この牙城は、物流、製造、小売、ビジネスサービスなど、大量かつ連続的な印刷が業務に不可欠な業界からの需要が高いことが主な要因です。高速ラインプリンターは、こうした環境において重要な役割を果たしており、取引ログ、請求書、出荷ラベルの迅速な作成を可能にしています。特にビジネスや小売の分野では、リアルタイムのトランザクション処理が重視されるようになり、高速ラインプリンターの採用が増加しています。必要な文書を迅速かつ効率的に作成できるラインプリンターは、この地域の企業にとって不可欠な資産となっています。

目次

第1章 調査手法と調査範囲

- 市場範囲と定義

- 基本推定と計算

- 予測計算

- データソース

- 1次データ

- 2次データ

- 有料情報源

- 公的情報源

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- バリューチェーンに影響を与える要因。

- 利益率分析

- 破壊

- 将来の展望

- メーカー

- 流通業者

- サプライヤーの状況

- 利益率分析

- 主要ニュース&イニシアチブ

- 規制状況

- 影響要因

- 促進要因

- 小売部門の増加

- 製造業の成長

- 業界の潜在的リスク&課題

- 市場の飽和と激しい競合

- 持続可能性への懸念

- 促進要因

- 技術概要

- 成長可能性分析

- ポーターの分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 競合のポジショニング・マトリックス

- 戦略展望マトリックス

第5章 市場推計・予測:技術別、2021年~2034年

- 主要動向

- インパクトプリンタ

- ドラムプリンター

- チェーンプリンター

- バンドプリンター

- ドットマトリクスプリンター

- ノンインパクトラインプリンタ

- サーマルラインプリンタ

- 静電印刷機

第6章 市場推計・予測:印刷速度別、2021年~2034年

- 主要動向

- 低速

- 中位

- 高速

第7章 市場推計・予測:用途別、2021~2034年

- 主要動向

- トランザクション印刷

- レポート印刷

- バーコード・ラベル印刷

- 文書印刷

- その他(連続紙印刷など)

第8章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 製造業および産業部門

- 小売・物流

- 銀行・金融サービス

- ヘルスケア

- 政府・公共部門

- 通信・IT

- その他(ホスピタリティなど)

第9章 市場推計・予測:流通チャネル別、2021年~2034年

- 主要動向

- 直接販売

- 間接販売

第10章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- ラテンアメリカ

- ブラジル

- メキシコ

- 中東・アフリカ

- UAE

- サウジアラビア

- 南アフリカ

第11章 企業プロファイル

- Printronix

- TallyGenicom

- Oki Electric Industry

- Epson

- Lexmark International

- Fujitsu

- Ricoh Company

- Brother Industries

- Hewlett-Packard Development Company

- Xerox Corporation

- Konica Minolta

- Kyocera Corporation

- Canon

- Seiko Epson Corporation

- Sharp Corporation

The Global Line Printer Market, valued at USD 1.27 billion in 2024, is on a steady growth trajectory, with a projected CAGR of 5% between 2025 and 2034. This upward trend is fueled by rapid advancements in printing technology and the increasing need for high-volume printing solutions across various industries. Line printers remain essential for businesses and organizations that rely on efficient, large-scale printing to streamline operations. These devices are particularly favored in sectors like logistics, manufacturing, retail, and business services, where clear, precise documentation is critical. With companies continually seeking cost-effective and high-speed printing solutions, the demand for line printers is expected to rise significantly in the coming years. Furthermore, the integration of newer technologies has elevated the performance of line printers, making them indispensable in environments that prioritize efficiency and accuracy.

The market is divided into two primary categories: impact and non-impact line printers. Non-impact line printers, which generated USD 760 million in 2024, are predicted to witness substantial growth in the years ahead. These printers stand out due to their superior print quality, achieved through advanced technologies such as thermal and electrostatic printing. The precision these technologies offer ensures high-quality output, making non-impact printers popular in industries like pharmaceuticals, automotive, and electronics. In these sectors, the ability to produce clear labels, codes, and small text is vital, and non-impact printers meet these demands seamlessly. As businesses continue to prioritize accuracy and quality in printed materials, the adoption of non-impact line printers is expected to accelerate further.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.27 Billion |

| Forecast Value | $2.07 Billion |

| CAGR | 5% |

When categorized by printing speed, line printers are segmented into slow, medium, and fast types. Medium-speed line printers, which accounted for 45% of the market in 2024, are set to maintain strong demand. These printers strike the perfect balance between affordability, speed, and performance, making them the preferred choice for businesses requiring regular and cost-effective printing solutions. Tasks such as generating mass reports, shipping labels, and invoices demand efficiency, and mid-speed line printers deliver precisely that. As businesses expand, the need for reliable and scalable printing solutions continues to grow, further driving the demand for medium-speed printers.

In 2024, North America captured a dominant 82% share of the global line printer market. This stronghold is largely attributed to the high demand from industries such as logistics, manufacturing, retail, and business services, where high-volume and continuous printing is integral to operations. High-speed line printers play a crucial role in these environments, enabling rapid production of transaction logs, invoices, and shipping labels. With the increasing emphasis on real-time transaction processing, especially in the business and retail sectors, the adoption of high-speed line printers is on the rise. Their ability to produce necessary documents quickly and efficiently makes them an indispensable asset for businesses in the region.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations.

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain.

- 3.1.2 Profit margin analysis.

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Supplier landscape

- 3.3 Profit margin analysis.

- 3.4 Key news & initiatives

- 3.5 Regulatory landscape

- 3.6 Impact forces

- 3.6.1 Growth drivers

- 3.6.1.1 Increasing retail units

- 3.6.1.2 Growing manufacturing industry

- 3.6.2 Industry pitfalls & challenges

- 3.6.2.1 Market saturation and intense competition

- 3.6.2.2 Sustainability concerns

- 3.6.1 Growth drivers

- 3.7 Technological overview

- 3.8 Growth potential analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Technology, 2021-2034 (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Impact line printers

- 5.2.1 Drum printers

- 5.2.2 Chain printers

- 5.2.3 Band printers

- 5.2.4 Dot matrix printers

- 5.3 Non-impact line printers

- 5.3.1 Thermal line printers

- 5.3.2 Electrostatic printers

Chapter 6 Market Estimates & Forecast, By Print Speed, 2021-2034 (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Low

- 6.3 Mid

- 6.4 High

Chapter 7 Market Estimates & Forecast, By Application, 2021-2034 (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Transaction printouts

- 7.3 Report printing

- 7.4 Barcode and label printing

- 7.5 Document printing

- 7.6 Others (continuous paper printing, etc.)

Chapter 8 Market Estimates & Forecast, By End-use, 2021-2034 (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 Manufacturing and industrial sector

- 8.3 Retail and logistics

- 8.4 Banking and financial services

- 8.5 Healthcare

- 8.6 Government and public sector

- 8.7 Telecommunication and IT

- 8.8 Others (hospitality, etc.)

Chapter 9 Market Estimates & Forecast, By Distribution Channel, 2021-2034 (USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 Direct

- 9.3 Indirect

Chapter 10 Market Estimates & Forecast, By Region, 2021-2034 (USD Billion) (Thousand Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 Australia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.6 MEA

- 10.6.1 UAE

- 10.6.2 Saudi Arabia

- 10.6.3 South Africa

Chapter 11 Company Profiles

- 11.1 Printronix

- 11.2 TallyGenicom

- 11.3 Oki Electric Industry

- 11.4 Epson

- 11.5 Lexmark International

- 11.6 Fujitsu

- 11.7 Ricoh Company

- 11.8 Brother Industries

- 11.9 Hewlett-Packard Development Company

- 11.10 Xerox Corporation

- 11.11 Konica Minolta

- 11.12 Kyocera Corporation

- 11.13 Canon

- 11.14 Seiko Epson Corporation

- 11.15 Sharp Corporation