|

市場調査レポート

商品コード

1684194

実験室用真空ポンプ市場の機会、成長促進要因、産業動向分析、2025年~2034年予測Laboratory Vacuum Pumps Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 実験室用真空ポンプ市場の機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年01月03日

発行: Global Market Insights Inc.

ページ情報: 英文 135 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

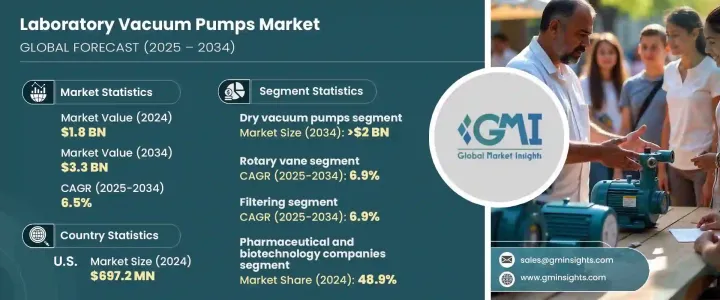

実験室用真空ポンプの世界市場は、2024年に18億米ドルと評価され、2025年から2034年にかけてCAGR 6.5%と予測されています。

この成長の主な要因は、製薬およびバイオテクノロジー分野の活況、研究開発(R&D)への投資の増加、高度な診断ソリューションへのニーズの高まりです。これらの業界の研究所は、医薬品開発、滅菌、乾燥などの重要な用途で真空ポンプに依存しています。慢性疾患の世界の流行が増加し続ける中、診断ツールやラボ機器に対する需要も増加し、真空ポンプ市場の拡大をさらに後押ししています。さらに、ヘルスケアの取り組みがより正確な診断と効率的な医薬品開発プロセスを推進する中、実験室用真空ポンプはこれらの進歩を確実に達成するために不可欠な役割を果たしています。

技術革新、特にオイルフリーでエネルギー効率の高い真空ポンプも市場の成長を後押ししています。持続可能性に対する意識の高まりと、実験機器に関する厳しい規制により、メーカーは現在、高性能で環境に優しいソリューションの開発に注力しています。このグリーン技術へのシフトは、規制上の要求を満たすだけでなく、多様な実験室環境における真空ポンプの応用範囲を拡大します。このように、真空ポンプは、効率性、持続可能性、性能を向上させ、研究室環境にとってますます不可欠なものとなりつつあります。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 18億米ドル |

| 予測金額 | 33億米ドル |

| CAGR | 6.5% |

市場は、ウェット真空ポンプ、真空ポンプ、ドライ真空ポンプなど製品タイプ別に区分されます。ドライ真空ポンプ分野が最も高い成長が見込まれており、CAGR 6.8%で成長し、2034年には20億米ドルに達すると予測されています。これらのポンプは、コンタミネーションのない運転と低メンテナンスの必要性から、医薬品やバイオテクノロジーなどの産業で特に支持されています。オイルフリーの設計は、純度が最重要視される環境では非常に重要であり、乾燥やろ過などの用途に非常に適しています。

技術に関しては、実験室用真空ポンプ市場はロータリーベーン、ロータリースクリュー、ロータリークロー、その他の技術に分けられます。ロータリーベーン真空ポンプ部門が優位を占め、CAGR 6.9%で成長し、2034年には15億米ドルに達する見込みです。これらのポンプは、ろ過、乾燥、蒸留などの用途において、その信頼性と多用途性で有名です。耐久性に優れた設計により安定した真空レベルが確保されるため、製薬会社や工業用研究室では不可欠なツールとなっています。

米国では、実験室用真空ポンプ市場は2024年に6億9,720万米ドルに達し、2025年から2034年までの予想CAGRは5.9%で、引き続き市場成長を牽引すると予測されています。この成長の原動力は、製薬・バイオテクノロジー分野における同国のリーダーシップであり、新たなヘルスケア構想や革新的な医薬品開発をサポートするための高度な実験機器に対する需要の高まりです。

目次

第1章 調査手法と調査範囲

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- 業界への影響要因

- 促進要因

- ヘルスケア分野での診断ラボ需要の増加

- 製薬およびバイオテクノロジー研究活動の成長

- 真空技術を必要とする高度医療機器の採用増加

- バイオ医薬品産業とワクチン生産の拡大

- 業界の潜在的リスク&課題

- 特定の真空ポンプのメンテナンス課題と運用コスト

- 促進要因

- 成長可能性分析

- 規制状況

- 技術情勢

- ギャップ分析

- ポーターの分析

- PESTEL分析

- 今後の市場動向

- バリューチェーン分析

第4章 競合情勢

- イントロダクション

- 企業マトリックス分析

- 企業シェア分析

- 主要市場プレーヤーの競合分析

- 競合のポジショニング・マトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:製品別、2021年~2034年

- 主要動向

- ドライ真空ポンプ

- 湿式真空ポンプ

- 複合真空ポンプ

第6章 市場推計・予測:技術別、2021年~2034年

- 主要動向

- ロータリーベーン

- ロータリースクリュー

- ロータリークロー

- その他の技術

第7章 市場推計・予測:用途別、2021~2034年

- 主要動向

- ろ過

- 乾燥

- 蒸留

- その他の用途

第8章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 製薬・バイオテクノロジー企業

- 病院、診断ラボ

- 学術・研究機関

- その他の最終用途

第9章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第10章 企業プロファイル

- Agilent

- Atlas Copco

- BUSCH

- DEKKER

- Ebara Technologies

- EDWARDS

- gast

- Graham

- KNF

- Leybold

- PFEIFFER

- SHIMADZU

- ULVAC

- VACUUBRAND

- WELCH

The Global Laboratory Vacuum Pumps Market was valued at USD 1.8 billion in 2024 and is projected to experience a CAGR of 6.5% from 2025 to 2034. This growth is primarily attributed to the booming pharmaceutical and biotechnology sectors, increasing investment in research and development (R&D), and the escalating need for advanced diagnostic solutions. Laboratories in these industries depend on vacuum pumps for critical applications such as drug development, sterilization, and drying. As the global prevalence of chronic diseases continues to rise, so does the demand for diagnostic tools and laboratory equipment, further driving the vacuum pump market expansion. Additionally, as healthcare initiatives push for more accurate diagnostics and efficient drug development processes, laboratory vacuum pumps play an essential role in ensuring these advancements can be achieved.

Technological innovations, particularly in oil-free and energy-efficient vacuum pumps, are also fueling market growth. With heightened awareness around sustainability and stringent regulations on laboratory equipment, manufacturers are now focusing on creating high-performance, eco-friendly solutions. This shift toward green technologies not only meets regulatory demands but also expands the range of applications for vacuum pumps in diverse laboratory environments. As such, vacuum pumps are becoming increasingly integral to laboratory settings, enhancing efficiency, sustainability, and performance.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.8 Billion |

| Forecast Value | $3.3 Billion |

| CAGR | 6.5% |

The market is segmented by product type, including wet vacuum pumps, vacuum pumps, and dry vacuum pumps. The dry vacuum pumps segment is expected to see the highest growth, projected to grow at a CAGR of 6.8%, reaching USD 2 billion by 2034. These pumps are especially favored in industries like pharmaceuticals and biotechnology for their contamination-free operation and low maintenance needs. Their oil-free design is critical in environments where purity is paramount, making them highly suitable for applications such as drying and filtration.

Regarding technology, the laboratory vacuum pumps market is divided into rotary vane, rotary screw, rotary claw, and other technologies. The rotary vane vacuum pump segment is set to dominate, expected to grow at a CAGR of 6.9%, reaching USD 1.5 billion by 2034. These pumps are renowned for their reliability and versatility in applications such as filtration, drying, and distillation. Their durable design ensures stable vacuum levels, making them an essential tool in both pharmaceutical and industrial laboratories.

In the U.S., the laboratory vacuum pumps market reached USD 697.2 million in 2024 and is projected to continue driving market growth, with an expected CAGR of 5.9% from 2025 to 2034. This growth is fueled by the nation's leadership in the pharmaceutical and biotechnology sectors, with increasing demand for advanced laboratory equipment to support new healthcare initiatives and innovative drug development.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing demand for diagnostic laboratories in the healthcare sector

- 3.2.1.2 Growth in pharmaceutical and biotechnology research activities

- 3.2.1.3 Rising adoption of advanced medical devices requiring vacuum technology

- 3.2.1.4 Expanding biopharmaceutical industry and vaccine production

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Maintenance challenges and operational costs of certain vacuum pumps

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Technology landscape

- 3.6 Gap analysis

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

- 3.9 Future market trends

- 3.10 Value chain analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Product, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Dry vacuum pumps

- 5.3 Wet vacuum pumps

- 5.4 Combination vacuum pumps

Chapter 6 Market Estimates and Forecast, By Technology, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Rotary vane

- 6.3 Rotary screw

- 6.4 Rotary claw

- 6.5 Other technologies

Chapter 7 Market Estimates and Forecast, By Application, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Filtering

- 7.3 Drying

- 7.4 Distillation

- 7.5 Other applications

Chapter 8 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Pharmaceutical and biotechnology companies

- 8.3 Hospitals and diagnostic labs

- 8.4 Academic and research institutes

- 8.5 Other end users

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Agilent

- 10.2 Atlas Copco

- 10.3 BUSCH

- 10.4 DEKKER

- 10.5 Ebara Technologies

- 10.6 EDWARDS

- 10.7 gast

- 10.8 Graham

- 10.9 KNF

- 10.10 Leybold

- 10.11 PFEIFFER

- 10.12 SHIMADZU

- 10.13 ULVAC

- 10.14 VACUUBRAND

- 10.15 WELCH