コネクタ市場のビジネスチャンス、成長要因、業界動向分析、および2026年~2035年の予測

Connector Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035- 発行日

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日

- 商品コード

- 1998851

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

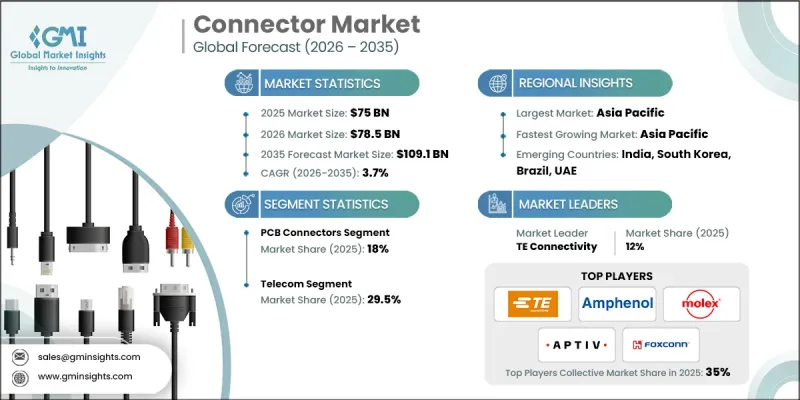

世界のコネクタ市場は、2025年に750億米ドルと評価され、CAGR 3.7%で成長し、2035年までに1,091億米ドルに達すると推定されています。

この市場は、民生用電子機器における充電インターフェースの標準化や、急速に拡大するEVインフラにおける車両と充電器の接続の統一を目指す規制当局の取り組みによって牽引されています。規制当局は、電子廃棄物の削減、デバイスエコシステムの合理化、およびOEMメーカーのコンプライアンス対応の簡素化を図るため、コネクタの統一性を重視しています。標準化されたレセプタクルは、ピン配置、安全プロトコル、および急速充電要件を定義し、材料の選択を見直し、多SKU生産の複雑さを軽減します。自動車分野では、電動化により、高出力で耐振動性・熱安定性に優れたコネクタへの需要が高まっています。一方、インターフェース規格の統合により、認証プロセスが加速し、相互運用可能な充電ネットワークが実現され、アフターマーケットの成長も後押しされています。一方、データセンターやハイパフォーマンスコンピューティングにおけるAIの導入拡大に伴い、高密度な計算ワークロードに対応するため、低挿入損失、厳密なスキュー制御、およびクロストーク低減を実現する、高速基板間コネクタ、メザニンコネクタ、光コネクタ、およびケーブルコネクタの需要が高まっています。

| 市場範囲 | |

|---|---|

| 開始年 | 2025年 |

| 予測期間 | 2026年~2035年 |

| 開始時の市場規模 | 750億米ドル |

| 予測額 | 1,091億米ドル |

| CAGR | 3.7% |

I/Oコネクタセグメントは、マルチプロトコル対応、サイバーセキュリティの強化、および高帯域幅のデジタル性能へのニーズに後押しされ、2035年までCAGR3.4%で成長すると予想されています。これらのコネクタは、高速かつ信頼性の高いデータ転送と、強化されたシールド性能を必要とする産業用コントローラ、ネットワーク機器、およびコンピューティングシステムにとって不可欠です。

通信セグメントは2025年に29.5%のシェアを占め、2035年までにCAGR 4.3%で成長すると予測されています。この成長は、帯域幅要件の高まり、高密度な5G/5G Advancedの展開、クラウドファーストのネットワークアーキテクチャ、および国際的な光ファイバーインフラの拡大によって牽引されています。この業界向けのコネクタは、超高速データ、低損失の光伝送、およびより高い周波数帯域に対応可能なRFインターフェースをサポートする必要があります。AI主導のネットワーク近代化により、高密度光コネクタ、モジュラー型相互接続、およびスケーラブルなファイバープラットフォームの採用がさらに増加しています。

2025年、米国のコネクタ市場は78%のシェアを占め、118億米ドルの市場規模を生み出しました。市場の拡大は、全国的なEV充電インフラの整備、テスト・計測用I/Oシステムの近代化、そしてAIワークロードを支えるハイパースケールクラウドの成長という3つの主要因によって牽引されています。高密度データセンターの増加に伴い、高密度ラックや液体冷却アーキテクチャ向けに設計された、耐熱性に優れた基板レベル相互接続、ファイバーアセンブリ、および電源コネクタへの需要が高まっています。

よくあるご質問

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 規制情勢

- 業界への影響要因

- 促進要因

- 自動車産業に対する明るい見通し

- 拡大する通信業界

- 急速な都市化と、民生用電子機器への需要拡大

- 業界の潜在的リスク&課題

- 低品質製品の流通が深刻化しています

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

- 新たな機会と動向

- デジタル化とIoTの統合

- 新興市場への進出

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 北米

- 欧州

- アジア太平洋地域

- 中東・アフリカ

- ラテンアメリカ

- 競合ベンチマーキング

- 戦略的ダッシュボード

- イノベーション・技術動向

第5章 市場規模・予測:製品別、2022-2035

- PCBコネクタ

- I/Oコネクタ

- 円形コネクタ

- 光ファイバーコネクタ

- RF同軸コネクタ

- その他

第6章 市場規模・予測:最終用途別、2022-2035

- 通信

- 交通機関

- 自動車

- コンピュータおよび周辺機器

- その他の産業

第7章 市場規模・予測:地域別、2022-2035

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- フランス

- スペイン

- 英国

- イタリア

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- 中東・アフリカ

- アラブ首長国連邦

- サウジアラビア

- 南アフリカ

- ラテンアメリカ

- ブラジル

- アルゼンチン

第8章 企業プロファイル

- 3M

- Ametek

- Amphenol

- Aptiv

- AVX

- Fischer Connectors

- Foxconn

- GTK

- Hirose Electric

- Japan Aviation Electronics

- Lapp Group

- LOTES

- Luxshare Precision

- Mencom

- Molex

- Phoenix Contact

- Rosenberger

- Samtec Inc.

- TE Connectivity

- Yazaki

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日