航空機ヘルスモニタリングシステム市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測

Aircraft Health Monitoring System Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 230 Pages

- 納期

- 2~3営業日

- 商品コード

- 1667139

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

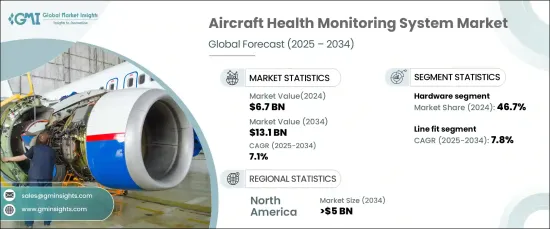

世界の航空機ヘルスモニタリングシステム市場は、2024年には67億米ドルと評価され、2025年から2034年にかけてCAGR 7.1%で成長すると予測されています。

航空部門では、予知保全の重視が高まっており、計画外のダウンタイムを最小限に抑えながら、運用効率に革命をもたらしています。先進技術によってリアルタイムのデータ収集と分析が可能になり、オペレーターは潜在的な故障を特定して予防措置を講じることができます。この進化は、包括的な監視と予測的洞察を提供するモノのインターネット(IoT)デバイスとビッグデータ分析の統合によって推進されています。航空会社やフリートオペレーターは、安全性の確保、メンテナンススケジュールの最適化、コスト削減のために、こうしたシステムの採用を増やしています。

航空機に設置されたIoTセンサーは、エンジン性能、温度、振動、燃料効率などの重要な運航データを取得します。この情報は、クラウドベースの分析プラットフォームを通じて処理され、異常の特定、メンテナンスの必要性の予測、システム全体の信頼性の向上が図られます。航空機システムと地上業務間のシームレスな通信は、統合された航空ネットワークを育み、意思決定プロセスと業務効率を向上させています。これらの技術がより高度になるにつれて、民間航空、民間航空、軍事航空全体での採用が大幅に増加すると予想されます。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 67億米ドル |

| 予測金額 | 131億米ドル |

| CAGR | 7.1% |

市場はソリューション別にハードウェア、ソフトウェア、サービスに区分され、2024年にはハードウェア分野が46.7%で最大のシェアを占めています。センサーやデータ収集装置などのハードウェア・コンポーネントは、エンジン性能のモニタリングにおいて重要な役割を果たします。これらの装置は、温度、圧力、振動などのパラメータを正確に測定し、潜在的な問題の早期発見を可能にします。ハードウェア技術の進歩により、コンポーネントの小型化、軽量化、耐久性の向上が進み、効率性と設置の容易性が向上しています。IoTシステムとの統合により、シームレスなデータ共有やクラウドベースの分析が可能になり、機能性がさらに向上しています。事業者は、信頼性が高く、費用対効果が高く、保守が簡単なハードウェア・ソリューションを優先します。

市場はラインフィットとレトロフィットに分けられ、ラインフィットは予測期間中にCAGR 7.8%で成長すると予測されます。ラインフィットでは、航空機の製造工程中にヘルスモニタリングシステムを設置し、特定のモデルとの互換性を確保し、システム統合を強化します。このアプローチにより、導入コストが削減され、メンテナンスが簡素化されるため、オペレーターやメーカーに好まれる選択肢となっています。新しい航空機の需要が高まるにつれ、ラインフィットセグメントは大きな成長を遂げると思われます。

北米市場は、米国の堅調な航空宇宙部門に牽引され、2034年までに50億米ドルを超えると予測されています。この地域は、大手航空会社、相手先商標製品メーカーの存在、機械学習とIoT技術の進歩から恩恵を受け、航空機ヘルスモニタリングシステムの採用を強化しています。

目次

第1章 調査手法と調査範囲

- 市場範囲と定義

- 基本推定と計算

- 予測計算

- データソース

- 1次データ

- 2次データ

- 有料情報源

- 公的情報源

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- バリューチェーンに影響を与える要因

- 利益率分析

- 破壊

- 将来の展望

- メーカー

- 流通業者

- サプライヤーの状況

- 利益率分析

- 主要ニュースと取り組み

- 規制状況

- 影響要因

- 促進要因

- 航空分野における予知保全の需要の高まり

- IoTとビッグデータ分析の統合の進展

- 航空機の大型化と運航効率化ニーズの高まり

- 厳しい安全規制がヘルスモニタリングの採用を促進

- 診断のためのリアルタイムデータ分析への注目の高まり

- 業界の潜在的リスク&課題

- 導入コストが高く、小規模な航空会社での導入が制限される

- システムの信頼性と信用に影響するデータセキュリティの懸念

- 促進要因

- 成長可能性分析

- ポーターの分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 競合のポジショニング・マトリックス

- 戦略展望マトリックス

第5章 市場推計・予測:ソリューション別、2021年~2034年

- 主要動向

- ハードウェア

- センサー

- エンジンと補助動力装置

- 航空構造

- 補助システム

- アビオニクス

- フライトデータ管理システム

- コネクテッド航空機ソリューション

- 地上サーバー

- センサー

- ソフトウェア

- 機内ソフトウェア

- 診断飛行データ解析

- 予知飛行データ解析ソフトウェア

- サービス

第6章 市場推計・予測:システム別、2021年~2034年

- 主要動向

- エンジンヘルスモニタリング

- 構造ヘルスモニタリング

- コンポーネントヘルスモニタリング

第7章 市場推計・予測:技術別、2021~2034年

- 主要動向

- 診断

- 予後

- 適応制御

- 処方的

第8章 市場推計・予測:動作モード別、2021年~2034年

- 主要動向

- リアルタイム

- 非リアルタイム

第9章 市場推計・予測:フィット別、2021年~2034年

- 主要動向

- ラインフィット

- レトロフィット

第10章 市場推計・予測:2021年~2034年:設置場所別

- 主要動向

- 機内

- 地上

第11章 市場推計・予測:プラットフォーム別、2021~2034年

- 主要動向

- 民間

- 軍事

- 先進エアモビリティ

第12章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- ラテンアメリカ

- ブラジル

- メキシコ

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第13章 企業プロファイル

- Air France KLM

- Airbus SE

- Boeing

- Curtiss-Wright Corporation

- Embraer

- FLYHT Aerospace Solutions Ltd.

- General Electric

- Honeywell International Inc

- Lufthansa

- Meggitt PLC

- Rolls-Royce PLC

- Safran Group

- Teledyne Controls LLC

目次

The Global Aircraft Health Monitoring System Market was valued at USD 6.7 billion in 2024 and is projected to grow at a CAGR of 7.1% from 2025 to 2034. Increasing emphasis on predictive maintenance within the aviation sector is revolutionizing operational efficiency while minimizing unplanned downtime. Advanced technologies are enabling real-time data collection and analysis, allowing operators to identify potential failures and take preventive actions. This evolution is being driven by the integration of Internet of Things (IoT) devices and big data analytics, which provide comprehensive monitoring and predictive insights. Airlines and fleet operators are increasingly adopting these systems to ensure safety, optimize maintenance schedules, and reduce costs.

IoT sensors installed on aircraft capture critical operational data, such as engine performance, temperature, vibration, and fuel efficiency. This information is processed through cloud-based analytics platforms to identify anomalies, forecast maintenance needs, and enhance overall system reliability. The seamless communication between aircraft systems and ground operations fosters an integrated aviation network, improving decision-making processes and operational efficiency. As these technologies become more advanced, their adoption across commercial, private, and military aviation is expected to grow significantly.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $6.7 Billion |

| Forecast Value | $13.1 Billion |

| CAGR | 7.1% |

The market is segmented by solution into hardware, software, and services, with the hardware segment holding the largest share at 46.7% in 2024. Hardware components, including sensors and data acquisition devices, play a critical role in monitoring engine performance. These devices provide precise measurements of parameters such as temperature, pressure, and vibration, enabling early detection of potential issues. Advancements in hardware technology have resulted in smaller, lighter, and more durable components, enhancing efficiency and ease of installation. Integration with IoT systems further improves functionality by enabling seamless data sharing and cloud-based analysis. Operators prioritize hardware solutions that are reliable, cost-effective, and simple to maintain.

By fit, the market is divided into line fit and retrofit, with the line fit segment expected to grow at a CAGR of 7.8% during the forecast period. Line fit involves installing health monitoring systems during the aircraft manufacturing process, ensuring compatibility with specific models, and enhancing system integration. This approach reduces implementation costs and simplifies maintenance, making it a preferred choice for operators and manufacturers alike. As the demand for new aircraft rises, the line fit segment is set to experience significant growth.

The North American market is projected to exceed USD 5 billion by 2034, driven by a robust aerospace sector in the United States. The region benefits from the presence of major airlines, original equipment manufacturers, and advancements in machine learning and IoT technologies, bolstering the adoption of aircraft health monitoring systems.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Key news & initiatives

- 3.5 Regulatory landscape

- 3.6 Impact forces

- 3.6.1 Growth drivers

- 3.6.1.1 Increasing demand for predictive maintenance in aviation sector

- 3.6.1.2 Advancements in IoT and big data analytics integration

- 3.6.1.3 Rising aircraft fleet size and operational efficiency needs

- 3.6.1.4 Stringent safety regulations driving health monitoring adoption

- 3.6.1.5 Growing focus on real-time data analysis for diagnostics

- 3.6.2 Industry pitfalls & challenges

- 3.6.2.1 High implementation costs limiting adoption in smaller airlines

- 3.6.2.2 Data security concerns impacting system reliability and trust

- 3.6.1 Growth drivers

- 3.7 Growth potential analysis

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Solution, 2021-2034 (USD Million)

- 5.1 Key trends

- 5.2 Hardware

- 5.2.1 Sensors

- 5.2.1.1 Engines and auxiliary power units

- 5.2.1.2 Aerostructures

- 5.2.1.3 Ancillary systems

- 5.2.2 Avionics

- 5.2.3 Flight data management systems

- 5.2.4 Connected aircraft solutions

- 5.2.5 Ground servers

- 5.2.1 Sensors

- 5.3 Software

- 5.3.1 Onboard software

- 5.3.2 Diagnostic flight data analysis

- 5.3.3 Prognostic flight data analysis software

- 5.4 Services

Chapter 6 Market Estimates & Forecast, By System, 2021-2034 (USD Million)

- 6.1 Key trends

- 6.2 Engine health monitoring

- 6.3 Structural health monitoring

- 6.4 Component health monitoring

Chapter 7 Market Estimates & Forecast, By Technology, 2021-2034 (USD Million)

- 7.1 Key trends

- 7.2 Diagnostic

- 7.3 Prognostic

- 7.4 Adaptive control

- 7.5 Prescriptive

Chapter 8 Market Estimates & Forecast, By Operation Mode, 2021-2034 (USD Million)

- 8.1 Key trends

- 8.2 Real time

- 8.3 Non-Real time

Chapter 9 Market Estimates & Forecast, By Fit, 2021-2034 (USD Million)

- 9.1 Key trends

- 9.2 Line fit

- 9.3 Retro fit

Chapter 10 Market Estimates & Forecast, By Installation, 2021-2034 (USD Million)

- 10.1 Key trends

- 10.2 On board

- 10.3 On ground

Chapter 11 Market Estimates & Forecast, By Platform, 2021-2034 (USD Million)

- 11.1 Key trends

- 11.2 Civil

- 11.3 Military

- 11.4 Advanced air mobility

Chapter 12 Market Estimates & Forecast, By Region, 2021-2034 (USD Million)

- 12.1 Key trends

- 12.2 North America

- 12.2.1 U.S.

- 12.2.2 Canada

- 12.3 Europe

- 12.3.1 UK

- 12.3.2 Germany

- 12.3.3 France

- 12.3.4 Italy

- 12.3.5 Spain

- 12.3.6 Russia

- 12.4 Asia Pacific

- 12.4.1 China

- 12.4.2 India

- 12.4.3 Japan

- 12.4.4 South Korea

- 12.4.5 Australia

- 12.5 Latin America

- 12.5.1 Brazil

- 12.5.2 Mexico

- 12.6 MEA

- 12.6.1 South Africa

- 12.6.2 Saudi Arabia

- 12.6.3 UAE

Chapter 13 Company Profiles

- 13.1 Air France KLM

- 13.2 Airbus SE

- 13.3 Boeing

- 13.4 Curtiss-Wright Corporation

- 13.5 Embraer

- 13.6 FLYHT Aerospace Solutions Ltd.

- 13.7 General Electric

- 13.8 Honeywell International Inc

- 13.9 Lufthansa

- 13.10 Meggitt PLC

- 13.11 Rolls-Royce PLC

- 13.12 Safran Group

- 13.13 Teledyne Controls LLC

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 230 Pages

- 納期

- 2~3営業日