|

市場調査レポート

商品コード

1876794

人工内耳市場におけるビジネスチャンス、成長要因、業界動向分析、および2025年から2034年までの予測Cochlear Implants Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 人工内耳市場におけるビジネスチャンス、成長要因、業界動向分析、および2025年から2034年までの予測 |

|

出版日: 2025年11月12日

発行: Global Market Insights Inc.

ページ情報: 英文 140 Pages

納期: 2~3営業日

|

概要

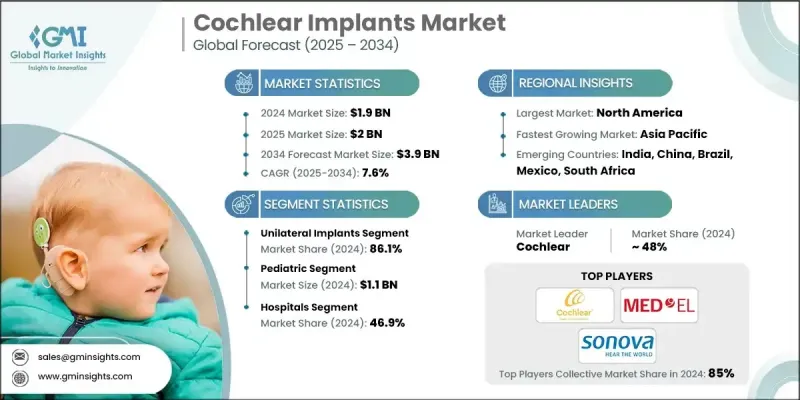

世界の人工内耳市場は、2024年に19億米ドルと評価され、2034年までにCAGR7.6%で成長し、39億米ドルに達すると予測されております。

市場拡大の主な要因としては、聴覚障害の有病率上昇、インプラント技術の革新、小児および高齢者における導入増加、ならびに広範な聴力スクリーニングプログラムと相まって高まる認知度が挙げられます。人工内耳は、損傷した内耳有毛細胞を迂回し、直接聴神経を刺激することで音の知覚を可能にする先進的な電子機器です。音信号を収集・処理・伝送する内部コンポーネントと外部コンポーネントで構成されています。音を増幅する補聴器とは異なり、人工内耳は音を電気信号に変換することで聴覚を部分的に回復させます。学校や病院における啓発活動の拡大と早期スクリーニングにより、適応患者の早期発見が可能となりました。また、聴覚学会、医療提供者、インプラントメーカー間の連携により患者教育が強化され、手術の受容性向上につながっています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年度 | 2025-2034 |

| 開始時価値 | 19億米ドル |

| 予測金額 | 39億米ドル |

| CAGR | 7.6% |

片側インプラントセグメントは、低コスト、手術の簡便さ、回復の早さ、そして臨床医による両側インプラントに対する選好により、2024年に86.1%のシェアを占めました。特に発展途上市場において、コスト面での優位性から、片側インプラントは患者様や医療提供者にとってより入手しやすい選択肢であり続けています。この手頃な価格設定は、両側インプラントの費用をかけずに聴力改善を求める個人による採用を促進しています。

病院セグメントは2024年に46.9%のシェアを生み出し、2025年から2034年にかけて17億米ドルに達すると予測されています。高齢化、騒音への長期間曝露、先天性疾患による感音性難聴症例の増加に伴い、病院で治療を求める患者が増加しています。病院は人工内耳手術を耳鼻咽喉科および聴覚学サービスに統合することで、患者ケアと収益源の強化というメリットを得ています。

北米の人工内耳市場は2024年に41.2%のシェアを占めました。同地域では加齢性・先天性を含む感音性難聴の罹患率が高く、早期診断・介入プログラムが推進されています。こうした取り組みが人工内耳の需要を大幅に押し上げ、市場の着実な成長を牽引しています。

人工内耳市場の主要企業には、MED-EL、Cochlear、Sonova、Envoy Medical、Nurotronなどが挙げられます。グローバル市場における各社は、市場基盤の強化に向け複数の戦略を展開しております。各社は、インプラントの機能性、快適性、および先進的な音声処理技術との互換性を高めるため、研究開発に投資しています。医療従事者向けの対象を絞った啓発キャンペーンや教育プログラムを通じて、小児および高齢者層への普及を拡大しています。病院や聴覚センターとの提携により、手術へのアクセスと患者の信頼を向上させています。発展途上市場への地理的拡大は未開拓の需要を取り込むのに役立ち、保険会社や政府との戦略的提携は手頃な価格と普及率を高めています。

よくあるご質問

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 業界への影響要因

- 促進要因

- 難聴の有病率の増加

- 技術的進歩

- 高まる意識と早期診断

- 政府による支援策の促進と償還状況の改善

- 業界の潜在的リスク&課題

- 人工内耳の高コスト

- 難聴に関する知識の不足

- 市場機会

- AI駆動型音声処理及び機械学習

- 促進要因

- 成長可能性分析

- 償還シナリオ

- 規制情勢

- 北米

- 欧州

- アジア太平洋地域

- LAMEA

- 技術動向

- 現在の技術動向

- 新興技術

- グローバル

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ地域

- 消費者経路

- 価格分析、2024

- 消費者洞察

- 政策環境

- リスク管理分析

- 研究開発

- オペレーションズ

- マーケティングと販売

- 品質

- 知的財産権

- 規制

- 情報技術

- 気候

- 財務

- 将来の市場動向

- サプライチェーンの動向と製造分析

- パイプライン分析

- ポーター分析

- PESTEL分析

- ギャップ分析

第4章 競合情勢

- イントロダクション

- 企業マトリックス分析

- 企業の市場シェア分析

- グローバル

- 北米

- 欧州

- アジア太平洋地域

- LAMEA地域

- 競合ポジショニングマトリックス

- 主要市場企業の競合分析

- 主な発展

- 合併・買収

- 提携・協業

- 新製品の発売

- 拡大計画

第5章 市場推計・予測:製品別、2021-2034

- 主要動向

- 片側インプラント

- 両側インプラント

第6章 市場推計・予測:患者タイプ別、2021-2034

- 主要動向

- 成人用

- 小児

第7章 市場推計・予測:最終用途別、2021-2034

- 主要動向

- 病院

- 耳鼻咽喉科クリニック

- 外来手術センター

第8章 市場推計・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋地域

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第9章 企業プロファイル

- Cochlear

- Envoy Medical

- MED-EL

- Nurotron

- Sonova