フッ素エラストマー市場の機会、成長促進要因、業界動向分析、2025~2034年の予測

Fluoroelastomers Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 180 Pages

- 納期

- 2~3営業日

- 商品コード

- 1667009

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

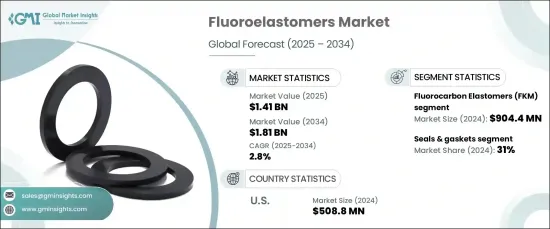

フッ素エラストマーの世界市場は、2024年には14億1,000万米ドルに達し、2025年から2034年にかけてCAGR 2.8%で成長すると予測されています。

この成長の主な要因は、優れた耐久性と過酷な環境への耐性を必要とする様々な産業で、高性能エラストマーに対する需要が高まっていることです。フッ素エラストマーは、極度の熱、化学物質、圧力に耐える独自の能力で知られ、自動車、航空宇宙、石油・ガスなどの重要な分野で採用が増加しています。産業が進化し、より弾力性のある材料が求められるようになるにつれ、フッ素エラストマーは、燃料システムやエンジン部品からシールやガスケットまで、多くの用途で不可欠な部品となっています。さらに、企業が持続可能性とエネルギー効率を優先する中、フッ素エラストマーは、長持ちする性能と環境基準を満たす能力で高い需要があります。

フッ素エラストマーは、主にフルオロカーボンエラストマー(FKM)とパーフルオロエラストマー(FFKM)に分類されます。2024年には、フルオロカーボンエラストマーが市場全体を支配し、収益全体の大きなシェアを占めています。これは、その卓越した熱安定性、耐薬品性、堅牢なシーリング・ソリューションを必要とする産業における幅広い用途に起因しています。これらのエラストマーは、エンジン、トランスミッション、燃料システムに使用されるガスケット、シール、Oリングによく見られます。一方、パーフルオロエラストマーは、耐薬品性と耐熱性が強化されているため、半導体や化学処理分野など、最高の信頼性が求められる産業における高度に特殊な用途に理想的であり、人気を集めています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 14億1,000万米ドル |

| 予測金額 | 18億1,000万米ドル |

| CAGR | 2.8% |

フッ素エラストマー市場の用途分野には、シール&ガスケット、Oリング、ホース&チューブ、その他特殊用途が含まれます。シールとガスケットは2024年の総収益の31%を占め、最大の市場シェアを占めており、予測期間を通じて力強い成長を維持すると予想されます。自動車産業はこの需要を大きく牽引しており、極度の熱や過酷な化学薬品に耐える能力を持つフッ素エラストマーに依存しています。航空宇宙用途で広く使用されているOリングは、重要部品の漏れ防止シールを確実にするため、引き続き高い需要があります。ホースとチューブも、さまざまな工業プロセスにおける流体の移送と封じ込めに重要な役割を果たしており、フッ素エラストマー市場の成長をさらに後押ししています。

米国では、フッ素エラストマー市場は2024年に5億880万米ドルを創出しました。この地域の成長を牽引しているのは、材料技術の進歩と、特に自動車、航空宇宙、エネルギー分野における高性能シーリング・ソリューションへの需要の高まりです。研究開発への継続的な投資とインフラの改善により、継続的な拡大が見込まれます。産業が進化し、より効率的で信頼性の高い材料を求めるようになるにつれ、米国のフッ素エラストマー市場は、従来の用途と新たな用途の両方を通じて、さらなる成長を遂げることになると思われます。

目次

第1章 調査手法と調査範囲

- 市場範囲と定義

- 基本推定と計算

- 予測計算

- データソース

- 1次データ

- 2次データ

- 有料情報源

- 公的情報源

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- バリューチェーンに影響を与える要因

- 利益率分析

- 破壊

- 将来の展望

- メーカー

- 流通業者

- サプライヤーの状況

- 利益率分析

- 主要ニュース

- 規制状況

- 影響要因

- 促進要因

- 自動車産業における需要の増加

- 航空宇宙用途での採用増加

- 化学加工産業の成長

- 業界の潜在的リスク&課題

- フッ素エラストマーのコスト高

- 促進要因

- 成長可能性分析

- ポーターの分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 競合のポジショニング・マトリックス

- 戦略展望マトリックス

第5章 市場規模・予測:製品別、2021年~2034年

- 主要動向

- フルオロカーボンエラストマー(FKM)

- パーフルオロエラストマー(FFKM)

第6章 市場規模・予測:用途別、2021年~2034年

- 主要動向

- Dシールとガスケット

- Oリング

- ホースとチューブ

- その他

第7章 市場規模・予測:最終用途産業別、2021年~2034年

- 主要動向

- 自動車

- 航空宇宙

- 石油・ガス

- 化学処理

第8章 市場規模・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- ラテンアメリカ

- ブラジル

- メキシコ

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第9章 企業プロファイル

- 3M

- AGC(Asahi Glass)

- Chemours

- Daikin Industries

- DowDuPont

- DuPont(E. I. du Pont de Nemours and Company)

- Gujarat Fluorochemicals

- HaloPolymer

- Mitsui Chemicals

- Momentive Performance Materials

- Saint-Gobain Performance Plastics

- Shin-Etsu Chemical

- Solvay

- Wacker Chemie

- Zeon Corporation

目次

The Global Fluoroelastomers Market is projected to reach USD 1.41 billion in 2024 and is expected to grow at a CAGR of 2.8% from 2025 to 2034. This growth is primarily driven by the rising demand for high-performance elastomers across various industries requiring superior durability and resistance to harsh environments. Fluoroelastomers, known for their unique ability to withstand extreme heat, chemicals, and pressures, are increasingly being adopted in critical sectors such as automotive, aerospace, and oil and gas. As industries evolve and demand more resilient materials, fluoroelastomers are becoming essential components in numerous applications, ranging from fuel systems and engine components to seals and gaskets. Furthermore, as companies prioritize sustainability and energy efficiency, fluoroelastomers are in high demand for their long-lasting performance and ability to meet environmental standards.

Fluoroelastomers are mainly categorized into fluorocarbon elastomers (FKM) and perfluoroelastomers (FFKM). In 2024, fluorocarbon elastomers dominated the market, accounting for a significant share of the overall revenue. This can be attributed to their exceptional thermal stability, chemical resistance, and wide range of uses in industries that require robust sealing solutions. These elastomers are commonly found in gaskets, seals, and o-rings used in engines, transmissions, and fuel systems. Perfluoroelastomers, on the other hand, are gaining traction due to their enhanced chemical and heat resistance, making them ideal for highly specialized applications in industries that demand the utmost reliability, such as semiconductor and chemical processing sectors.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.41 Billion |

| Forecast Value | $1.81 Billion |

| CAGR | 2.8% |

The application segment of the fluoroelastomers market includes seals & gaskets, o-rings, hoses & tubings, and other specialized applications. Seals and gaskets held the largest market share, accounting for 31% of the total revenue in 2024, and are expected to maintain strong growth throughout the forecast period. The automotive industry is a significant driver of this demand, relying on fluoroelastomers for their ability to withstand extreme heat and harsh chemicals. O-rings, widely used in aerospace applications, continue to be in high demand, as they ensure leak-proof seals in critical components. Hoses and tubings also play a vital role in fluid transfer and containment across various industrial processes, further bolstering the growth of the fluoroelastomers market.

In the U.S., the fluoroelastomers market generated USD 508.8 million in 2024. Growth in this region is driven by advancements in material technologies and a growing demand for high-performance sealing solutions, particularly in the automotive, aerospace, and energy sectors. Ongoing investments in research and development, along with infrastructure improvements, are expected to fuel continued expansion. As industries evolve and seek more efficient and reliable materials, the fluoroelastomers market in the U.S. is set to experience further growth through both traditional and emerging applications.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definition

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Key news & initiatives

- 3.5 Regulatory landscape

- 3.6 Impact forces

- 3.6.1 Growth drivers

- 3.6.1.1 Increasing demand in automotive industry

- 3.6.1.2 Rising adoption in aerospace applications

- 3.6.1.3 Growing chemical processing industries

- 3.6.2 Industry pitfalls & challenges

- 3.6.2.1 High cost of fluoroelastomers

- 3.6.1 Growth drivers

- 3.7 Growth potential analysis

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Size and Forecast, By Product, 2021-2034 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Fluorocarbon elastomers (FKM)

- 5.3 Perfluoroelastomers (FFKM)

Chapter 6 Market Size and Forecast, By Application, 2021-2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 D seals and gaskets

- 6.3 O-rings

- 6.4 Hoses and tubings

- 6.5 Others

Chapter 7 Market Size and Forecast, By End Use Industries, 2021-2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Automotive

- 7.3 Aerospace

- 7.4 Oil & gas

- 7.5 Chemical processing

Chapter 8 Market Size and Forecast, By Region, 2021-2034 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 UK

- 8.3.2 Germany

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Russia

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 South Korea

- 8.4.5 Australia

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.6 MEA

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 3M

- 9.2 AGC (Asahi Glass)

- 9.3 Chemours

- 9.4 Daikin Industries

- 9.5 DowDuPont

- 9.6 DuPont (E. I. du Pont de Nemours and Company)

- 9.7 Gujarat Fluorochemicals

- 9.8 HaloPolymer

- 9.9 Mitsui Chemicals

- 9.10 Momentive Performance Materials

- 9.11 Saint-Gobain Performance Plastics

- 9.12 Shin-Etsu Chemical

- 9.13 Solvay

- 9.14 Wacker Chemie

- 9.15 Zeon Corporation

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 180 Pages

- 納期

- 2~3営業日