|

市場調査レポート

商品コード

1876643

抗菌性タンパク質加水分解物市場の機会、成長要因、業界動向分析、および2025年から2034年までの予測Antimicrobial (Enzymatic) Protein Hydrolysates Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 抗菌性タンパク質加水分解物市場の機会、成長要因、業界動向分析、および2025年から2034年までの予測 |

|

出版日: 2025年11月13日

発行: Global Market Insights Inc.

ページ情報: 英文 210 Pages

納期: 2~3営業日

|

概要

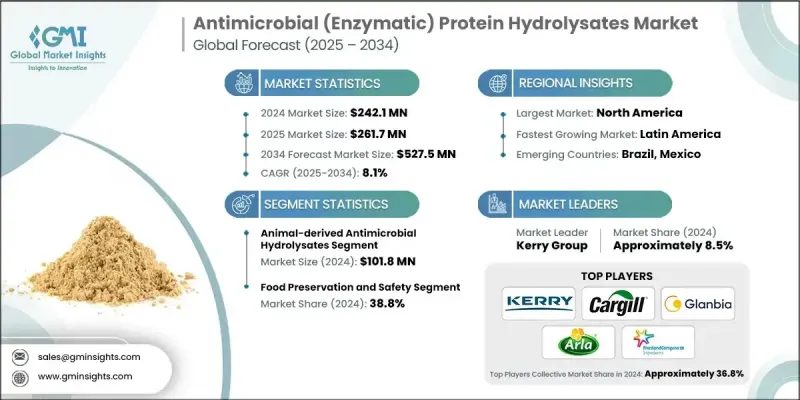

世界の抗菌(酵素)タンパク質加水分解物市場は、2024年に2億4,210万米ドルと評価され、2034年までにCAGR8.1%で成長し、5億2,750万米ドルに達すると予測されております。

食品メーカーや消費者がクリーンラベルへの期待に沿った天然保存ソリューションへ移行するにつれ、市場の勢いは高まっています。酵素処理された加水分解物は、栄養価を損なうことなく製品の鮮度を維持するため、合成保存料の代替としてより頻繁に選択されています。この動向は、抗生物質耐性に関する世界的な懸念の高まりによって支えられており、抗生物質過剰使用に寄与しない抗菌ツールの必要性を高めています。これらの加水分解物は食品および健康関連用途において効果的な微生物制御を提供するため、進化する規制要件や安全基準に強く適合します。健康とウェルネスへの関心の高まりも需要を後押ししており、現代の消費者は機能性と生物活性効果を併せ持つ原料を求めており、その重要性は基本的な保存効果を超えています。業界の重点が製品の安全性と品質を向上させる天然由来ソリューションへ移行する中、抗菌性タンパク質加水分解物は食品、栄養、関連分野全体で強力な普及が見込まれます。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測期間 | 2025-2034 |

| 開始時価値 | 2億4,210万米ドル |

| 予測金額 | 5億2,750万米ドル |

| CAGR | 8.1% |

動物由来抗菌加水分解物セグメントは、2024年に1億180万米ドルと評価され、2025年から2034年にかけて7.8%のCAGRで成長すると予想されています。その採用は、強力なペプチド活性と有利な規制上の受容性により、食品保存、臨床栄養、サプリメント製剤において増加を続けています。これらの加水分解物は、牛乳、肉、卵などのタンパク質源から一般的に製造され、安全性と強化された生物活性の両方が求められる高タンパク質製品や即食製品における抗菌性で高く評価されています。

食品保存・安全用途セグメントは2024年に9,370万米ドルの市場規模を記録し、2034年までCAGR7.4%で拡大が見込まれます。本セグメントでは、乳製品、加工食品、飲料、レトルト食品における微生物増殖抑制にタンパク質加水分解物が活用されています。合成保存料を天然由来のペプチド系代替品に置き換えることで、保存期間の延長と原材料表示の透明性維持を実現し、クリーンラベル要件の達成を支援します。

北米の抗菌(酵素)タンパク質加水分解物市場は、2024年に8,470万米ドルの規模を記録しました。クリーンラベル保存への関心の高まりと厳格な食品安全コンプライアンスにより、同地域での採用が増加しています。同地域では、機能性食品や栄養補助食品メーカーの強い存在感が強みとなっており、抗菌性と栄養特性を併せ持つ生物活性ペプチドの用途拡大を支えています。化学保存料使用削減に向けた規制圧力も食品企業に酵素加水分解物の採用を促しており、バイオテクノロジーやタンパク質加工技術への投資が継続されることで、食品・医療産業全体において製品品質の向上、プロファイリング精度の改善、スケーラビリティの強化が進んでいます。

抗菌(酵素)タンパク質加水分解物市場に参画する主要企業には、カーギル社、グランビア社、フリースランドキャンピナ・イングレディエンツ社、アーラ・フーズ・イングレディエンツ社、ケリー・グループなどが挙げられます。同市場の企業は、存在感を強化するため複数の戦略に注力しております。多くの企業が、ペプチドの純度、効力、安定性を向上させる先進的な酵素処理技術への投資を推進しております。食品メーカー、ニュートラシューティカルブランド、バイオテクノロジーパートナーとの協業を拡大し、複数分野における応用開発を加速させております。クリーンラベル配合の支援、カスタマイズされた抗菌ソリューション、機能プロファイルの強化への重点は、依然として中核的な優先事項です。また、優れた抗菌特性を持つ新規の生物活性ペプチドを特定するため、研究開発費の増額も進めています。生産能力の拡大、規制対応の強化、グローバル流通ネットワークの拡充は、競争力強化に寄与しています。

よくあるご質問

目次

第1章 調査手法

- 市場範囲と定義

- 調査設計

- 調査アプローチ

- データ収集方法

- データマイニングの情報源

- グローバル

- 地域別/国別

- 基本推定値と計算

- 基準年計算

- 市場推定における主要な動向

- 1次調査および検証

- 一次情報

- 予測モデル

- 調査前提条件と制限事項

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- 各段階における付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- 天然食品保存料に対する需要の高まり

- 抗生物質耐性への懸念の高まり

- 健康とウェルネスへの意識の高まり

- 機能性食品における応用拡大

- 業界の潜在的リスク&課題

- 高い生産・加工コスト

- 規制の複雑性と承認上の課題

- 保存期間の制限と安定性の課題

- 市場機会

- 乳業廃水の有効利用

- AIを活用したペプチド探索

- 化粧品分野における新興用途

- 植物性タンパク源の拡大

- 促進要因

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- ポーター分析

- PESTEL分析

- 価格動向

- 地域別

- 製品別

- 将来の市場動向

- 技術とイノベーションの動向

- 現在の技術動向

- 新興技術

- 特許状況

- 貿易統計(注:貿易統計は主要国のみ提供されます)

- 主要輸入国

- 主要輸出国

- 持続可能性と環境的側面

- 持続可能な実践

- 廃棄物削減戦略

- 生産におけるエネルギー効率

- 環境に配慮した取り組み

- カーボンフットプリントに関する考慮事項

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 地域別

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ地域

- 地域別

- 企業マトリクス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併・買収

- 提携・協力関係

- 新製品の発売

- 事業拡大計画

第5章 市場推計・予測:製品タイプ別、2021-2034

- 主要動向

- 動物由来抗菌性加水分解物

- 乳タンパク質加水分解物

- ホエイタンパク質加水分解物

- カゼイン加水分解物

- 魚タンパク質加水分解物

- 肉タンパク質加水分解物

- 卵タンパク質加水分解物

- 植物由来抗菌性加水分解物

- 大豆タンパク質加水分解物

- 小麦タンパク質加水分解物

- マメ科植物タンパク質加水分解物

- 穀物タンパク質加水分解物

- 種子タンパク質加水分解物

- 海洋由来抗菌性加水分解物

- 魚製品別加水分解物

- 藻類タンパク質加水分解物

- 海藻タンパク質加水分解物

- 甲殻類殻加水分解物

- 微生物由来抗菌性加水分解物

- 細菌発酵製品

- 真菌加水分解物

- 酵母由来ペプチド

第6章 市場推計・予測:用途別、2021-2034

- 主要動向

- 食品保存と安全性

- 天然保存料

- 抗菌コーティング

- 活性包装ソリューション

- 保存期間の延長

- 栄養補助食品

- スポーツ栄養

- 臨床栄養学

- 乳児用調製粉乳

- 栄養補助食品

- 機能性食品

- 飼料およびペットフード

- 成長促進剤

- 抗生物質代替品

- 消化器健康サポート

- 免疫システムの強化

- 医薬品・ヘルスケア

- 治療用ペプチド

- 創傷ケア製品

- 口腔ケア用途

- 外用抗菌剤

- 化粧品およびパーソナルケア

- 抗菌製剤

- スキンケア製品

- ヘアケア用途

- アンチエイジングソリューション

第7章 市場推計・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他欧州地域

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- その他アジア太平洋地域

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- その他ラテンアメリカ地域

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

- その他中東とアフリカ

第8章 企業プロファイル

- Kerry Group

- Cargill Inc.

- Glanbia plc

- Arla Foods Ingredients

- FrieslandCampina Ingredients

- DSM-Firmenich

- ADM(Archer Daniels Midland)

- AMCO Proteins

- Kemin Industries

- Titan Biotech

- BRF Ingredients

- Constantino &C Spa

- Crescent Biotech

- Aker Biomarine

- Biomega Group

- Essentia Protein Solutions