|

市場調査レポート

商品コード

1822614

建築用断熱材の市場機会と促進要因、業界動向分析、2025年~2034年予測Building Thermal Insulation Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 建築用断熱材の市場機会と促進要因、業界動向分析、2025年~2034年予測 |

|

出版日: 2025年08月20日

発行: Global Market Insights Inc.

ページ情報: 英文 170 Pages

納期: 2~3営業日

|

概要

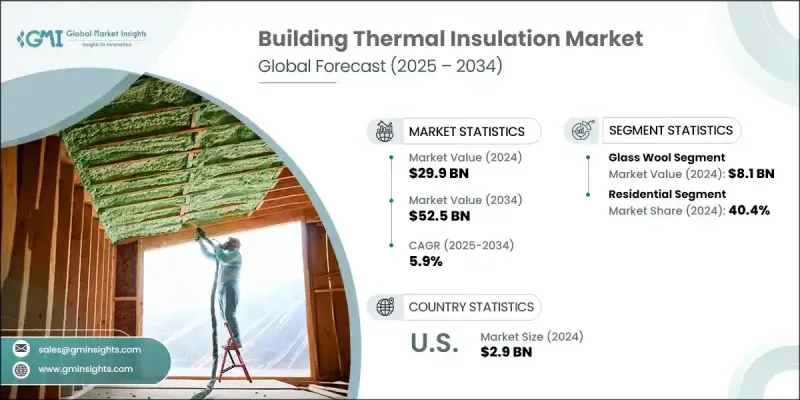

建築用断熱材の世界市場規模は2024年に299億米ドルとなり、CAGR 5.9%で成長し、2034年には525億米ドルに達すると予測されています。

環境意識の高まりと気候変動への懸念が、建設におけるエネルギー効率の高いソリューションの需要を促進しています。建築物はかなりのエネルギー消費を占めており、断熱材は冷暖房の必要性を減らし、温室効果ガスの排出を効果的に削減します。これは世界的な持続可能性への取り組みと一致し、環境に優しい断熱材の採用を後押ししています。

消費者、開発業者、請負業者は、持続可能でエネルギー効率の高い選択肢をますます好むようになり、天然素材やリサイクル素材から作られた製品の需要に拍車をかけています。LEEDやBREEAMのような規制の枠組みやグリーンビルディング認証は、エネルギー効率の高い断熱材をさらに促進し、税金の払い戻しのような財政的インセンティブは採用を後押しします。その結果、エネルギー効率の高い住宅や商業施設への投資は増加の一途をたどっており、断熱材はエネルギーコストの削減と環境への影響の最小化に不可欠な要素となっています。市場の成長は、より持続可能な構造物を建設するという集団的な焦点を反映しています。

| 市場規模 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 市場規模 | 299億米ドル |

| 予測金額 | 525億米ドル |

| CAGR | 5.9% |

市場は素材別にオープンセル型とクローズドセル型に区分されます。オープンセル素材は大きな牽引力を持っており、2024年には129億6,000万米ドルの貢献、2034年には238億4,000万米ドルに達すると予測されています。これらの材料はコスト効率が高く、住宅や商業用途、特に予算重視のプロジェクトで広く採用されています。また、防音性を高め、リサイクル材料から作られた環境に優しいオプションでグリーン建築をサポートします。オープンセル素材は、施工が容易で熱性能が高いことから、エネルギー効率を向上させるために古い建物を改修する際に好まれています。

販売チャネル別では、市場は直接販売と間接販売に分けられます。2024年のシェアは間接販売チャネルが45.01%で市場をリードし、2034年には196億9,000万米ドルに達すると予想されます。製造業者は、製品の入手と顧客へのリーチを効率化する販売業者、卸売業者、小売業者の広範なネットワークから利益を得ています。これらの仲介業者は物流の課題を軽減し、市場への浸透を高め、メーカーが製品開発とブランディングに集中できるよう支援します。間接チャネルはまた、オンライン・プラットフォームを通じて需要の高まりに対応し、買い手にとってのアクセシビリティと利便性を高めています。

米国は2024年の世界市場の売上高の53.5%を占め、2034年までのCAGRは6.3%と予測されています。同国の多様な建設産業と厳しいエネルギー効率規制が、高度な断熱ソリューションの需要を促進しています。税額控除やグリーン認証などの政府の取り組みが、断熱材の使用をさらに後押ししています。同国では断熱技術の革新が重視され、さまざまな気候帯で省エネソリューションが必要とされているため、引き続き市場の成長が促進されます。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- 業界への影響要因

- 促進要因

- エネルギー効率規制の強化

- 建設と都市化の進展

- 環境問題と持続可能性への取り組み

- 業界の潜在的リスク&課題

- 初期投資コストが高め

- 代替技術の利用可能性

- 機会

- 環境に優しいリサイクル素材の開発

- 改修・改築市場の成長

- 促進要因

- 成長可能性分析

- 将来の市場動向

- テクノロジーとイノベーションの情勢

- 現在の技術動向

- 新興技術

- 価格動向

- 地域別

- 素材別

- 規制情勢

- 標準とコンプライアンス要件

- 地域規制枠組み

- 認証基準

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 地域別

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画

第5章 市場推計・予測:材料別、2021-2034

- 主要動向

- グラスウール

- 石綿

- 発泡スチロール

- 押出ポリスチレン

- ポリウレタン

- その他

第6章 市場推計・予測:形態別、2021-2034

- 主要動向

- 毛布

- パネル

- フォーム

- その他

第7章 市場推計・予測:用途別、2021-2034

- 主要動向

- 壁断熱

- 内壁

- 外壁

- 空洞壁

- カーテンウォール

- 屋根断熱材

- 平らな屋根

- 傾斜屋根

- 床/スラブ

- その他

第8章 市場推計・予測:最終用途別、2021-2034

- 主要動向

- 住宅用

- 商業用

- 産業

第9章 市場推計・予測:流通チャネル別、2021-2034

- 主要動向

- 直接

- 間接的

第10章 市場推計・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- アジア太平洋地域

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第11章 企業プロファイル

- Armacell

- Burnett &Co

- Firestone Building Products

- GLT Products

- Johns Manville

- Kingspan Group

- Knauf Insulation

- Mapei

- NICHIAS Corporation

- Owens Corning

- Recticel Insulation

- Rockwool International

- Saint-Gobain Isover

- Siltherm

- URSA