|

市場調査レポート

商品コード

1666945

人工知能ツールキットの市場機会、成長促進要因、産業動向分析、2025年~2034年予測Artificial Intelligence Toolkit Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 人工知能ツールキットの市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2024年12月03日

発行: Global Market Insights Inc.

ページ情報: 英文 180 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

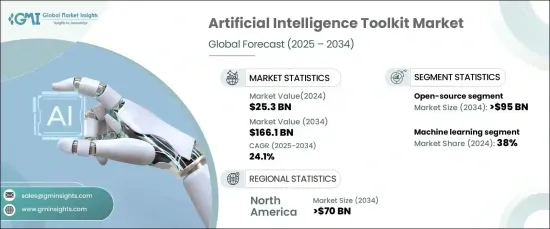

世界の人工知能ツールキット市場は、2024年に253億米ドルとなり、2025年から2034年にかけて24.1%という驚異的なCAGRで成長すると予測されています。

ヘルスケア、金融、eコマース、製造業などの業界全体でAI駆動型ソリューションの採用が急増していることが、この堅調な成長に拍車をかけています。画像認識、自然言語処理(NLP)、レコメンデーションシステムなどの用途で機械学習(ML)やディープラーニングモデルを設計・導入するために、AIツールキットを利用する企業が増えています。

AIの研究と技術の急速な進歩は、市場の拡大を加速させる態勢を整えています。アルゴリズム、モデルアーキテクチャ、最先端技術の革新により、複雑な課題を解決し、業務効率を高めることができる高度なAIツールキットへの需要が高まっています。企業が競合情勢で優位に立とうとする中、強力で拡張性の高いAIソリューションの必要性はかつてないほど高まっています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025年~2034年 |

| 開始金額 | 253億米ドル |

| 予測金額 | 1,661億米ドル |

| CAGR | 24.1% |

市場はタイプ別にオープンソースと商用AIツールキットに区分されます。2024年には、オープンソースのツールキットが市場シェアの55%を占め、2034年には950億米ドルに達すると予測されています。オープンソースのAIツールキットは、費用対効果、柔軟性、カスタマイズの容易さにより特に魅力的です。これらのツールは、開発者、特に新興企業や中小企業(SME)に、独自のニーズに合わせた手頃な価格でありながら堅牢なソリューションを提供することで、開発者に力を与えます。

用途別に見ると、市場は機械学習、自然言語処理、コンピュータビジョン、その他に分類されます。2024年には機械学習が市場をリードし、シェアの38%を占めました。この優位性は、多様な分野にわたる広範な有用性を反映しています。MLツールキットは、企業がデータ分析を自動化し、予測モデルを構築し、インテリジェントな意思決定プロセスを促進することを可能にします。ヘルスケア、金融、小売などの業界は、イノベーションを推進し、成果を最適化するためにMLを特に活用しています。

北米のAIツールキット市場は、2024年には40%の圧倒的なシェアを占め、2034年には700億米ドルに達すると予想されています。この成長の原動力となっているのは、強固な技術インフラ、AI研究への多額の投資、さまざまな業界でAIが広く採用されていることです。米国は、技術革新におけるリーダーシップを活用し、この地域の主要プレーヤーとして際立っています。ヘルスケア、金融、小売、自動車などの分野でAI導入が進んでいることが、北米市場の優位性をさらに際立たせています。

目次

第1章 調査手法と調査範囲

- 調査デザイン

- 調査アプローチ

- データ収集方法

- 基本推定と計算

- 基準年の算出

- 市場推計の主要動向

- 予測モデル

- 一次調査と検証

- 一次ソース

- データマイニングソース

- 市場定義

第2章 エグゼクティブサマリー

第3章 業界洞察

- 業界エコシステム分析

- サプライヤーの状況

- テクノロジープロバイダー

- クラウドサービスプロバイダー

- データプロバイダー

- AIソリューション・プロバイダー

- 最終用途

- 利益率分析

- 一般的なAIツールキットの比較分析

- ツールキットのライセンスモデルとコスト構造

- テクノロジーとイノベーションの展望

- 主要ニュースとイニシアチブ

- 規制状況

- 影響要因

- 成長促進要因

- 業界全体におけるAIとMLの採用の増加

- AIのセキュリティとプライバシーへの関心の高まり

- AIツールへの投資の増加

- 自動化とデジタル化への志向の高まり

- 業界の潜在的リスク・課題

- 複雑性への懸念

- セキュリティとプライバシーに関する懸念

- 成長促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業市場シェア分析

- 競合のポジショニングマトリックス

- 戦略展望マトリックス

第5章 市場推計・予測:タイプ別、2021年~2034年

- 主要動向

- オープンソース

- 商用

第6章 市場推計・予測:コンポーネント別、2021年~2034年

- 主要動向

- ハードウェア

- ソフトウェア

- サービス

第7章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- 自然言語処理

- 機械学習

- コンピュータビジョン

- その他

第8章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- IT・通信

- 小売・eコマース

- BFSI

- 製造業

- エネルギー・公益事業

- 政府機関

- その他

第9章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- スペイン

- イタリア

- ロシア

- 北欧

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- ニュージーランド

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- UAE

- 南アフリカ

- サウジアラビア

第10章 企業プロファイル

- Amazon

- C3.ai

- Databricks

- DataRobot

- Google LLC

- H2O.ai

- HPE

- Intel

- Meta Platform(Facebook)

- Microsoft

- NVIDIA

- OpenAI

- Oracle

- Salesforce

- SAP

- SAS

- Scale AI

- Teradata

- Thales

- UiPath

The Global Artificial Intelligence Toolkit Market was valued at USD 25.3 billion in 2024 and is projected to grow at an impressive CAGR of 24.1% from 2025 to 2034. The surge in adoption of AI-driven solutions across industries such as healthcare, finance, e-commerce, and manufacturing is fueling this robust growth. Businesses increasingly rely on AI toolkits to design and deploy machine learning (ML) and deep learning models for applications, including image recognition, natural language processing (NLP), and recommendation systems.

Rapid advancements in AI research and technology are poised to accelerate market expansion. Innovations in algorithms, model architectures, and cutting-edge techniques are boosting demand for advanced AI toolkits capable of solving complex challenges and enhancing operational efficiency. As businesses seek to stay ahead in a competitive landscape, the need for powerful and scalable AI solutions has never been greater.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $25.3 Billion |

| Forecast Value | $166.1 Billion |

| CAGR | 24.1% |

The market is segmented by type into open-source and commercial AI toolkits. In 2024, open-source toolkits accounted for 55% of the market share, with projections to reach USD 95 billion by 2034. Open-source AI toolkits are particularly appealing due to their cost-effectiveness, flexibility, and ease of customization. These tools empower developers, especially startups and small-to-medium enterprises (SME), by offering affordable yet robust solutions tailored to their unique needs.

By application, the market is categorized into machine learning, natural language processing, computer vision, and others. Machine learning led the market in 2024, capturing 38% of the share. This dominance reflects its extensive utility across diverse sectors. ML toolkits enable businesses to automate data analysis, build predictive models, and facilitate intelligent decision-making processes. Industries such as healthcare, finance, and retail are particularly leveraging ML to drive innovation and optimize outcomes.

North America AI toolkit market held a commanding 40% share in 2024, with expectations to generate USD 70 billion by 2034. This growth is driven by a robust technological infrastructure, significant investment in AI research, and widespread adoption of AI across various industries. The United States stands out as a key player in the region, leveraging its leadership in technological innovation. High AI adoption in sectors like healthcare, finance, retail, and automotive further underscores North America's market dominance.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supplier landscape

- 3.2.1 Technology providers

- 3.2.2 Cloud service providers

- 3.2.3 Data providers

- 3.2.4 AI solution providers

- 3.2.5 End use

- 3.3 Profit margin analysis

- 3.4 Comparative analysis of popular AI toolkits

- 3.5 Toolkit licensing models and cost structures

- 3.6 Technology & innovation landscape

- 3.7 Key news & initiatives

- 3.8 Regulatory landscape

- 3.9 Impact forces

- 3.9.1 Growth drivers

- 3.9.1.1 Increasing adoption of AI and ML across industries

- 3.9.1.2 Growing focus on AI security and privacy

- 3.9.1.3 Increasing investment in AI tools

- 3.9.1.4 Rise in inclination towards automation and digitalization

- 3.9.2 Industry pitfalls & challenges

- 3.9.2.1 Complexity concerns

- 3.9.2.2 Security and privacy concerns

- 3.9.1 Growth drivers

- 3.10 Growth potential analysis

- 3.11 Porter’s analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Type, 2021 - 2034 ($Bn)

- 5.1 Key trends

- 5.2 Open source

- 5.3 Commercial

Chapter 6 Market Estimates & Forecast, By Component, 2021 - 2034 ($Bn)

- 6.1 Key trends

- 6.2 Hardware

- 6.3 Software

- 6.4 Services

Chapter 7 Market Estimates & Forecast, By Application, 2021 - 2034 ($Bn)

- 7.1 Key trends

- 7.2 Natural language processing

- 7.3 Machine learning

- 7.4 Computer vision

- 7.5 Others

Chapter 8 Market Estimates & Forecast, By End Use, 2021 - 2034 ($Bn)

- 8.1 Key trends

- 8.2 IT & telecom

- 8.3 Retail and e-commerce

- 8.4 BFSI

- 8.5 Manufacturing

- 8.6 Energy and utility

- 8.7 Government

- 8.8 Others

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Russia

- 9.3.7 Nordics

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 ANZ

- 9.4.6 Southeast Asia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 South Africa

- 9.6.3 Saudi Arabia

Chapter 10 Company Profiles

- 10.1 Amazon

- 10.2 C3.ai

- 10.3 Databricks

- 10.4 DataRobot

- 10.5 Google LLC

- 10.6 H2O.ai

- 10.7 HPE

- 10.8 Intel

- 10.9 Meta Platform (Facebook)

- 10.10 Microsoft

- 10.11 NVIDIA

- 10.12 OpenAI

- 10.13 Oracle

- 10.14 Salesforce

- 10.15 SAP

- 10.16 SAS

- 10.17 Scale AI

- 10.18 Teradata

- 10.19 Thales

- 10.20 UiPath