|

市場調査レポート

商品コード

1666710

パイプ断熱材の市場機会、成長促進要因、産業動向分析、2025年~2034年予測Pipe Insulation Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| パイプ断熱材の市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2024年12月26日

発行: Global Market Insights Inc.

ページ情報: 英文 220 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

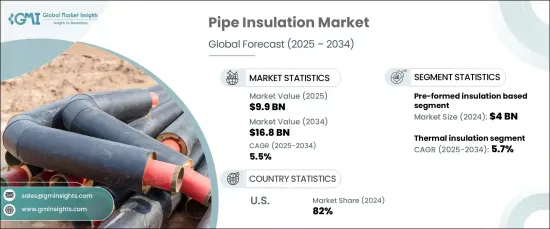

世界のパイプ断熱材市場は2024年に99億米ドルとなり、2025年から2034年にかけてCAGR5.5%で成長すると予測されています。

この成長は、エネルギー効率への注目の高まり、規制基準の遵守、持続可能な建設手法の採用の高まりが主な要因です。パイプ断熱材は、冷暖房システムのエネルギー損失を効果的に最小化し、住宅、商業、工業環境におけるエネルギー効率の改善に貢献します。

エネルギーコストが上昇を続け、二酸化炭素排出量の削減が急務となる中、パイプ断熱材はエネルギー消費全体を削減する実用的なソリューションとして注目を集めています。配管システムの温度を一定に保ち、暖房や冷房に必要なエネルギーを削減することで、長期的なコスト削減と持続可能性のメリットをもたらします。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025年~2034年 |

| 開始金額 | 99億米ドル |

| 予測金額 | 168億米ドル |

| CAGR | 5.5% |

市場は製品タイプ別に、成形前断熱材、硬質ボード断熱材、ブランケット断熱材、ロール断熱材、スプレーフォーム断熱材、その他に区分されます。このうち、成形前断熱材は主要セグメントとして頭角を現し、2024年には約40億米ドルの収益を生み出します。このセグメントは、ユーザーフレンドリーな設置プロセスと様々なパイプ寸法や構成に対応する能力により、着実に成長すると予測されています。ガラス繊維やミネラルウールなどの材料を使用して製造される予備成形断熱材は、人件費と設置時間を削減するため、あらゆる分野で好まれています。

機能別に見ると、市場は断熱、防音、防火、その他に分類されます。断熱材は2024年に市場シェアの約40%を占め、予測期間中にCAGR5.7%で成長すると予測されています。断熱材の主な役割は、パイプ内の温度を一定に保つことで、エネルギーの浪費を最小限に抑え、工業プロセスのパフォーマンスを最適化します。この機能は、効率と操業コストの削減が優先される製造やエネルギー生産のような分野で特に重要です。

地域別では、米国が北米のパイプ断熱材市場の約82%という大きなシェアを占めています。建築基準法の厳格化とエネルギー効率の義務化が、高度な断熱ソリューションの需要を促進しています。規制の枠組みはHVACや配管システムのエネルギー損失を減らすことを目的としており、高性能断熱材の採用を後押ししています。

パイプ断熱材市場は、省エネルギー重視の高まりと、効率的で持続可能なインフラソリューションの必要性によって、力強い成長が見込まれています。

目次

第1章 調査手法と調査範囲

- 市場範囲と定義

- 基本推定と計算

- 予測計算

- データソース

- 一次

- 二次

- 有料ソース

- 公的ソース

第2章 エグゼクティブサマリー

第3章 業界洞察

- 業界エコシステム分析

- バリューチェーンに影響を与える要因

- 利益率分析

- 変革

- 将来の展望

- メーカー

- 流通業者

- サプライヤーの状況

- 利益率分析

- 主要ニュースと取り組み

- 規制状況

- 影響要因

- 成長促進要因

- 建設活動の増加

- 製品革新の進展

- 業界の潜在的リスク・課題

- 市場の飽和と激しい競合

- 持続可能性への懸念

- 成長促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業市場シェア分析

- 競合のポジショニングマトリックス

- 戦略展望マトリックス

第5章 市場推計・予測:製品タイプ別、2021年~2035年

- 主要動向

- 予備成形断熱材

- 硬質ボード断熱材

- ブランケット断熱材

- ロール断熱材

- スプレーフォーム断熱材

- その他(ルースフィル断熱材など)

第6章 市場推計・予測:材料タイプ別、2021年~2035年

- 主要動向

- ガラス繊維

- ミネラルウール

- ポリウレタン

- ポリエチレン

- エラストマーフォーム

- ゴム

- その他(ケイ酸カルシウムなど)

第7章 市場推計・予測:機能別、2021年~2035年

- 主要動向

- 断熱

- 遮音

- 防火

- その他(結露防止など)

第8章 市場推計・予測:最終用途別、2021年~2035年

- 主要動向

- 住宅用

- 商業用

- 産業用

- 石油・ガス

- 化学

- エネルギー・電力

- 海洋

- その他(製薬など)

第9章 市場推計・予測:流通チャネル別、2021年~2035年

- 主要動向

- 直接

- 間接

第10章 市場推計・予測:地域別、2021年~2035年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- ラテンアメリカ

- ブラジル

- メキシコ

- 中東・アフリカ

- UAE

- サウジアラビア

- 南アフリカ

第11章 企業プロファイル

- 3M

- Alfa Laval

- Armacell International

- BASF

- Covestro

- Huntsman Corporation

- Insulation Technologies

- Johns Manville

- Kingspan Group

- Knauf Insulation

- Owens Corning

- Rockwool International

- Saint Gobain

- Shenzhen Lanxuan Industrial

- Thermaflex

The Global Pipe Insulation Market was valued at USD 9.9 billion in 2024 and is expected to grow at a CAGR of 5.5% from 2025 to 2034. This growth is largely driven by the increasing focus on energy efficiency, compliance with regulatory standards, and the rising adoption of sustainable construction practices. Insulating pipes effectively minimizes energy loss in heating and cooling systems, contributing to improved energy efficiency in residential, commercial, and industrial settings.

As energy costs continue to climb and the urgency to reduce carbon emissions intensifies, pipe insulation is gaining prominence as a practical solution to lower overall energy consumption. It helps maintain consistent temperatures in piping systems, reducing the energy required for heating or cooling, thus offering long-term cost savings and sustainability benefits.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $9.9 Billion |

| Forecast Value | $16.8 Billion |

| CAGR | 5.5% |

The market is segmented by product type into pre-formed insulation, rigid board insulation, blanket insulation, roll insulation, spray foam insulation, and others. Among these, pre-formed insulation emerged as a leading segment, generating approximately USD 4 billion in revenue in 2024. This segment is projected to grow steadily, owing to its user-friendly installation process and ability to accommodate various pipe dimensions and configurations. Manufactured using materials such as fiberglass and mineral wool, pre-formed insulation reduces labor costs and installation time, making it a preferred choice across sectors.

By function, the market is categorized into thermal insulation, acoustic insulation, fire protection, and others. Thermal insulation accounted for around 40% of the market share in 2024 and is anticipated to grow at a CAGR of 5.7% over the forecast period. Its primary role is to maintain temperature consistency in pipes, thus minimizing energy waste and optimizing performance in industrial processes. This functionality is particularly important in sectors like manufacturing and energy production, where efficiency and operational cost reduction are priorities.

Regionally, the United States dominates the North America pipe insulation market, holding a substantial share of approximately 82%. Stricter building codes and energy-efficiency mandates are fueling demand for advanced insulation solutions. Regulatory frameworks aim to reduce energy loss in HVAC and plumbing systems, boosting the adoption of high-performance insulation materials.

The pipe insulation market is poised for robust growth, driven by the increasing emphasis on energy conservation and the need for efficient and sustainable infrastructure solutions.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2035

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Key news & initiatives

- 3.5 Regulatory landscape

- 3.6 Impact forces

- 3.6.1 Growth drivers

- 3.6.1.1 Increasing construction activities

- 3.6.1.2 Growing product innovation

- 3.6.2 Industry pitfalls & challenges

- 3.6.2.1 Market saturation and intense competition

- 3.6.2.2 Sustainability concerns

- 3.6.1 Growth drivers

- 3.7 Growth potential analysis

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2023

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Product Type, 2021-2035 (USD Million) (Thousand Square Feet)

- 5.1 Key trends

- 5.2 Pre-formed insulation

- 5.3 Rigid board insulation

- 5.4 Blanket insulation

- 5.5 Roll insulation

- 5.6 Spray Foam insulation

- 5.7 Others (loose fill insulation, etc.)

Chapter 6 Market Estimates & Forecast, By Material Type, 2021-2035 (USD Million) (Thousand Square Feet)

- 6.1 Key trends

- 6.2 Fiberglass

- 6.3 Mineral wool

- 6.4 Polyurethane

- 6.5 Polyethylene

- 6.6 Elastomeric foam

- 6.7 Rubber

- 6.8 Others (calcium silicate, etc.)

Chapter 7 Market Estimates & Forecast, By Function, 2021-2035 (USD Million) (Thousand Square Feet)

- 7.1 Key trends

- 7.2 Thermal insulation

- 7.3 Acoustic insulation

- 7.4 Fire protection

- 7.5 Others (condensation control, etc.)

Chapter 8 Market Estimates & Forecast, By End Use, 2021-2035 (USD Million) (Thousand Square Feet)

- 8.1 Key trends

- 8.2 Residential

- 8.3 Commercial

- 8.4 Industrial

- 8.4.1 Oil & gas

- 8.4.2 Chemical

- 8.4.3 Energy & power

- 8.4.4 Marine

- 8.4.5 Others (pharmaceutical, etc.)

Chapter 9 Market Estimates & Forecast, By Distribution Channel, 2021-2035 (USD Million) (Thousand Square Feet)

- 9.1 Key trends

- 9.2 Direct

- 9.3 Indirect

Chapter 10 Market Estimates & Forecast, By Region, 2021-2035 (USD Million) (Thousand Square Feet)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 Australia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.6 MEA

- 10.6.1 UAE

- 10.6.2 Saudi Arabia

- 10.6.3 South Africa

Chapter 11 Company Profiles

- 11.1 3M

- 11.2 Alfa Laval

- 11.3 Armacell International

- 11.4 BASF

- 11.5 Covestro

- 11.6 Huntsman Corporation

- 11.7 Insulation Technologies

- 11.8 Johns Manville

- 11.9 Kingspan Group

- 11.10 Knauf Insulation

- 11.11 Owens Corning

- 11.12 Rockwool International

- 11.13 Saint Gobain

- 11.14 Shenzhen Lanxuan Industrial

- 11.15 Thermaflex