|

市場調査レポート

商品コード

1666646

圧力センサー市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測Pressure Sensor Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 圧力センサー市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2024年12月31日

発行: Global Market Insights Inc.

ページ情報: 英文 210 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

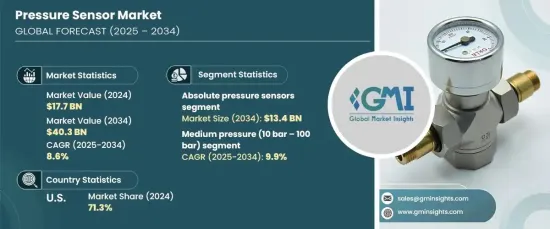

世界の圧力センサー市場は2024年に177億米ドルに達し、2025年から2034年にかけてCAGR 8.6%で拡大すると予測されています。

この急成長の主な要因は、小型化、スペクトル分解能の向上、幅広い産業で利用可能な費用対効果の高いシステムの開発など、センサー技術の継続的な進歩にあります。

自動車、ヘルスケア、産業オートメーション、航空宇宙などの分野で、よりスマートで信頼性の高いセンシング・ソリューションへの需要が高まるにつれ、圧力センサーは多くの重要なアプリケーションに不可欠なコンポーネントとなっています。その汎用性と精度により、エンジン管理から環境モニタリングに至るまで、多くのシステムの円滑な運用に不可欠なものとなっています。自動化への依存の高まりと、高性能機械における精度へのニーズの高まりが、市場成長の原動力となっています。スマートテクノロジーとインフラ開発への大規模な投資により、先進的な圧力センサーの需要は今後数年で急増する見込みです。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 177億米ドル |

| 予測金額 | 403億米ドル |

| CAGR | 8.6% |

圧力センサーは製品タイプ別に分類され、差圧、絶対圧、真空、密閉、マルチレンジ、ゲージ圧力センサーが最も一般的に使用されています。このうち、絶対圧力センサーが市場で最大のシェアを占めており、2034年までに134億米ドルに達すると予測されています。これらのセンサーは、完全な真空に関連して圧力を測定するように設計されているため、航空宇宙、自動車、環境モニタリングなど、高い精度が要求される用途に不可欠です。大気圧の変動にもかかわらず一貫して機能する能力を持つため、精度が譲れない環境では欠かせないです。

市場はまた、低圧(10barまで)、中圧(10barから100bar)、高圧(100bar以上)の圧力レンジによっても区分されます。10バールから100バールの範囲で作動する中圧セグメントは、2025年から2034年までのCAGRが9.9%と予測され、最も急成長しているカテゴリーです。これらのセンサーは、製造、自動車、産業オートメーションなどの産業で重要な役割を果たしています。油圧・空圧システムの監視と制御に不可欠で、さまざまな機械やプロセスの安定性と効率を保証します。

2024年、米国は圧力センサーの世界市場で71.3%という圧倒的なシェアを占めています。同国の主導的地位は、高度な技術インフラ、強力な自動車部門、産業オートメーションとヘルスケアへの多額の投資に起因しています。これらの産業が革新を続けるにつれて、圧力センサーの需要は増加し続けると予想されます。特に高精度と信頼性が要求される分野では、技術とインフラの進歩が続いており、米国は依然として世界市場の主要プレーヤーです。

目次

第1章 調査手法と調査範囲

- 市場範囲と定義

- 基本推定と計算

- 予測計算

- データソース

- 1次データ

- 2次データ

- 有料情報源

- 公的情報源

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- バリューチェーンに影響を与える要因

- 利益率分析

- 破壊

- 将来の展望

- メーカー

- 流通業者

- サプライヤーの状況

- 利益率分析

- 主要ニュース

- 規制状況

- 影響要因

- 促進要因

- 自動車技術の進歩

- 産業オートメーションの成長

- 家電製品の拡大

- ヘルスケアモニタリングへの注目の高まり

- 業界の潜在的リスク&課題

- 高い製造コスト

- 統合とキャリブレーションの複雑さ

- 促進要因

- 成長可能性分析

- ポーターの分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 競合のポジショニング・マトリックス

- 戦略展望マトリックス

第5章 市場推計・予測:製品タイプ別、2021年~2034年

- 主要動向

- 絶対圧力センサー

- ゲージ圧力センサー

- 差圧力センサー

- 真空圧力センサー

- 密閉式圧力センサー

- マルチレンジ圧力センサー

- その他

第6章 市場推計・予測:技術別、2021年~2034年

- 主要動向

- ピエゾ抵抗

- 静電容量式

- 電磁式

- 共振固体

- 光学

- その他

第7章 市場推計・予測:出力タイプ別、2021年~2034年

- 主要動向

- アナログ出力

- デジタル出力

第8章 市場推計・予測:圧力レンジ別、2021年~2034年

- 主要動向

- 低圧(10 barまで)

- 中圧(10 bar~100 bar)

- 高圧(100 bar以上)

第9章 市場推計・予測:業界別、2021年~2034年

- 主要動向

- 自動車

- ヘルスケア

- 工業製造

- エネルギー・電力

- 家電

- 航空宇宙・防衛

- 石油・ガス

- その他

第10章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- ラテンアメリカ

- ブラジル

- メキシコ

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第11章 企業プロファイル

- Analog Devices Inc.(ADI)

- APG(American Pressure Gauge)

- Bosch Sensortec

- Delphi Technologies

- Emerson Electric Co.

- First Sensor AG

- FUTEK Advanced Sensor Technology

- Hitec Products

- Honeywell International Inc.

- Infineon Technologies AG

- Kistler Instrumente AG

- Murata Manufacturing Co., Ltd.

- NXP Semiconductors

- Panasonic Corporation

- Sensata Technologies

- STMicroelectronics

- TE Connectivity

- Texas Instruments(TI)

The Global Pressure Sensor Market reached USD 17.7 billion in 2024 and is projected to expand at a CAGR of 8.6% between 2025 and 2034. This surge is primarily fueled by continuous advancements in sensor technology, including miniaturization, improved spectral resolution, and the development of cost-effective systems that are accessible to a wide range of industries.

As the demand for smarter and more reliable sensing solutions increases across sectors such as automotive, healthcare, industrial automation, and aerospace, pressure sensors have become essential components for many critical applications. Their versatility and accuracy make them integral to the smooth operation of numerous systems, from engine management to environmental monitoring. The growing reliance on automation, coupled with the rising need for precision in high-performance machinery, is driving market growth. With significant investments in smart technologies and infrastructure development, the demand for advanced pressure sensors is set to escalate in the coming years.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $17.7 billion |

| Forecast Value | $40.3 billion |

| CAGR | 8.6% |

Pressure sensors are categorized by product type, with differential, absolute, vacuum, sealed, multi-range, and gauge pressure sensors being the most commonly used. Among these, the absolute pressure sensor segment holds the largest share of the market and is projected to reach USD 13.4 billion by 2034. These sensors are designed to measure pressure in relation to a perfect vacuum, making them crucial for applications requiring high levels of precision, such as in aerospace, automotive, and environmental monitoring. With their ability to function consistently despite fluctuations in atmospheric pressure, they are indispensable in environments where accuracy is non-negotiable.

The market is also segmented by pressure range, including low (up to 10 bar), medium (10 bar to 100 bar), and high-pressure (above 100 bar) sensors. The medium-pressure segment, operating within the 10 bar to 100 bar range, is the fastest-growing category, with a projected CAGR of 9.9% from 2025 to 2034. These sensors play a vital role in industries such as manufacturing, automotive, and industrial automation. They are essential for the monitoring and control of hydraulic and pneumatic systems, which ensure the stability and efficiency of various machinery and processes.

In 2024, the U.S. dominated the global pressure sensor market, holding a commanding 71.3% share. The country's leading position is attributed to its advanced technological infrastructure, strong automotive sector, and significant investments in industrial automation and healthcare. As these industries continue to innovate, the demand for pressure sensors is expected to keep rising. With ongoing advancements in technology and infrastructure, particularly in areas requiring high precision and reliability, the U.S. remains a key player in the global market.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Key news & initiatives

- 3.5 Regulatory landscape

- 3.6 Impact forces

- 3.6.1 Growth drivers

- 3.6.1.1 Advancements in automotive technologies

- 3.6.1.2 Growth in industrial automation

- 3.6.1.3 Expansion of consumer electronics

- 3.6.1.4 Increased focus on healthcare monitoring

- 3.6.2 Industry pitfalls & challenges

- 3.6.2.1 High manufacturing costs

- 3.6.2.2 Integration and calibration complexities

- 3.6.1 Growth drivers

- 3.7 Growth potential analysis

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Product Type, 2021-2034 (USD Million & Volume Units)

- 5.1 Key trends

- 5.2 Absolute pressure sensors

- 5.3 Gauge pressure sensors

- 5.4 Differential pressure sensors

- 5.5 Vacuum pressure sensors

- 5.6 Sealed pressure sensors

- 5.7 Multi-range pressure sensors

- 5.8 Others

Chapter 6 Market Estimates & Forecast, By Technology, 2021-2034 (USD Million & Units)

- 6.1 Key trends

- 6.2 Piezoresistive

- 6.3 Capacitive

- 6.4 Electromagnetic

- 6.5 Resonant solid-state

- 6.6 Optical

- 6.7 Others

Chapter 7 Market Estimates & Forecast, By Output Type, 2021-2034 (USD Million & Units)

- 7.1 Key trends

- 7.2 Analog output

- 7.3 Digital output

Chapter 8 Market Estimates & Forecast, By Pressure Range, 2021-2034 (USD Million & Units)

- 8.1 Key trends

- 8.2 Low pressure (Up to 10 bar)

- 8.3 Medium pressure (10 bar – 100 bar)

- 8.4 High pressure (Above 100 bar)

Chapter 9 Market Estimates & Forecast, By Industry Vertical, 2021-2034 (USD Million & Units)

- 9.1 Key trends

- 9.2 Automotive

- 9.3 Healthcare

- 9.4 Industrial manufacturing

- 9.5 Energy and power

- 9.6 Consumer electronics

- 9.7 Aerospace & defense

- 9.8 Oil & gas

- 9.9 Others

Chapter 10 Market Estimates & Forecast, By Region, 2021-2034 (USD Million & Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 Australia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Analog Devices Inc. (ADI)

- 11.2 APG (American Pressure Gauge)

- 11.3 Bosch Sensortec

- 11.4 Delphi Technologies

- 11.5 Emerson Electric Co.

- 11.6 First Sensor AG

- 11.7 FUTEK Advanced Sensor Technology

- 11.8 Hitec Products

- 11.9 Honeywell International Inc.

- 11.10 Infineon Technologies AG

- 11.11 Kistler Instrumente AG

- 11.12 Murata Manufacturing Co., Ltd.

- 11.13 NXP Semiconductors

- 11.14 Panasonic Corporation

- 11.15 Sensata Technologies

- 11.16 STMicroelectronics

- 11.17 TE Connectivity

- 11.18 Texas Instruments (TI)