Infrastructure as Code市場の機会、成長促進要因、産業動向分析、2025~2034年の予測

Infrastructure as Code Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 180 Pages

- 納期

- 2~3営業日

- 商品コード

- 1666630

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

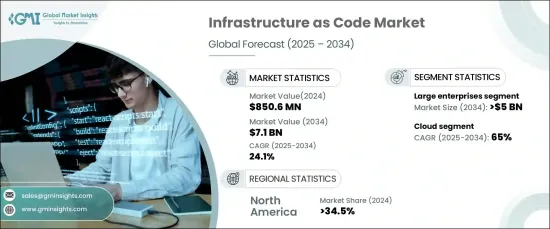

世界のInfrastructure As Code市場は、2024年に8億5,060万米ドルの評価額に達し、2025年から2034年にかけて24.1%のCAGRで著しい成長を遂げると予測されています。

この急成長の背景には、クラウドコンピューティングの採用が拡大し、マルチクラウド環境が好まれるようになっていることがあります。世界中の組織は、単一ベンダーへの依存を軽減し、運用コストを最適化し、さまざまなクラウドプラットフォームが提供する独自の機能を活用するために、複数のクラウドプロバイダーを活用しています。こうした戦略的シフトは、企業が複雑なITインフラを効率的に管理し、自動化することを可能にするIaCソリューションの需要を促進しています。さらに、DevOpsプラクティスの台頭と、拡張性、柔軟性、一貫性のあるインフラ管理ソリューションに対するニーズの高まりが、市場の成長をさらに後押ししています。また、各業界でデジタルトランスフォーメーションへの取り組みが急増していることも、IaCの採用を加速させています。業界全体でデジタル変革イニシアチブが急増したことで、企業は信頼性とセキュリティを確保しながら導入サイクルを加速することを目指しており、IaC の採用も拡大しています。

市場は企業規模別に中小企業(SME)と大企業に区分されます。2024年には、大企業の市場シェアが72%を占め、この分野での重要な役割を裏付けています。このセグメントは2034年までに50億米ドルを生み出すと見られています。大企業は通常、多様なワークロード、膨大なデータ、複雑なシステムを管理する高度なツールを必要とする複雑な業務を世界規模で展開しています。こうした企業は、ハイブリッドクラウドやマルチクラウド戦略を採用することが多く、IaCはITエコシステムの不可欠な要素となっています。インフラのプロビジョニング、構成、管理を自動化することで、IaCは運用効率を高め、人的ミスを減らし、ビジネスクリティカルなプロセスのシームレスな実行をサポートします。一貫性を維持しながらリソースをダイナミックに拡張できるIaaCは、今日のめまぐるしく変化するデジタル環境において、大企業の競争力を高めます。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 8億5,060万米ドル |

| 予測金額 | 71億米ドル |

| CAGR | 24.1% |

Infrastructure as Code市場は、展開タイプ別にオンプレミス型とクラウド型に分類されます。クラウド分野は2024年に65%のシェアを獲得しており、予測期間を通じてその主導権を維持すると予想されます。あらゆる規模の企業でクラウドコンピューティングの普及が進んでいるため、クラウドベースのリソースの管理を効率化できるIaCツールの需要が高まっています。クラウドプラットフォームは、効率的なセットアップ、構成、スケーリングを必要とするさまざまなサービスを提供しています。IaCによって、企業はコードを使用してこれらのプロセスを自動化し、一貫した展開を保証し、手動による介入を最小限に抑え、リソースの利用を最適化することができます。IaCとクラウドプラットフォームのこの相乗効果は、特に企業が俊敏性と革新性をますます優先するようになる中で、採用を推進する上で極めて重要です。

北米のInfrastructure as Code市場は、2024年の世界シェアの34.5%を占め、主導的地位を確固たるものにしています。この優位性は、同地域の先進的な技術環境と、クラウド・コンピューティングの導入に注力する姿勢に起因しています。特に米国は、最先端のクラウド・インフラストラクチャ・サービスと広く採用されているIaCツールを提供する大手テクノロジー企業を抱え、重要な役割を果たしています。これらの企業が確立された存在感を示すことで、活発なエコシステムが形成され、北米がIaCのイノベーションと成長の最前線に君臨し続けています。その強固な基盤とテクノロジーへの継続的な投資により、この地域は、効率的で自動化されたインフラ管理ソリューションに対する需要の高まりに対応できる体制を整えています。

目次

第1章 調査手法と調査範囲

- 調査デザイン

- 調査アプローチ

- データ収集方法

- 基本推定と計算

- 基準年の算出

- 市場推計の主要動向

- 予測モデル

- 1次調査と検証

- 一次情報

- データマイニングソース

- 市場定義

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- サプライヤーの状況

- クラウドサービスプロバイダー

- IaCツールプロバイダー

- セキュリティ・コンプライアンス・プロバイダー

- システムインテグレーター

- 最終用途

- 利益率分析

- テクノロジーとイノベーションの展望

- IaCの使用事例

- 主要ニュースとイニシアチブ

- 規制状況

- 影響要因

- 促進要因

- クラウド導入とマルチクラウド環境の拡大

- コスト効率とリソースの最適化

- DevOpsとCI/CDの採用の増加

- 俊敏性と展開の高速化

- 業界の潜在的リスク&課題

- 高まるセキュリティへの懸念

- 既存システムとの統合課題

- 促進要因

- 成長可能性分析

- ポーターの分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 競合のポジショニング・マトリックス

- 戦略展望マトリックス

第5章 市場推計・予測:アプローチ別、2021年~2034年

- 主要動向

- 宣言的

- 命令的

第6章 市場推計・予測:組織規模別、2021年~2034年

- 主要動向

- 中小企業

- 大企業

第7章 市場推計・予測:展開別、2021年~2034年

- 主要動向

- オンプレミス

- クラウド

第8章 市場推計・予測:インフラ別、2021年~2034年

- 主要動向

- ミュータブルIaC

- イミュータブルIaC

第9章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 政府機関

- IT&テレコム

- ヘルスケア

- BFSI

- 製造業

- 小売

- その他

第10章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- スペイン

- イタリア

- ロシア

- 北欧

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- ニュージーランド

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- UAE

- 南アフリカ

- サウジアラビア

第11章 企業プロファイル

- Alibaba Group

- Alpacked

- Amazon

- Cisco

- Crossplane

- Dell

- GitLab

- HashiCorp

- HPE

- IBM

- Microsoft

- Oracle

- Progress Software

- Pulumi

- Puppet

- Rackspace Technology

- Red Hat

- Snyk

- Zscaler

目次

The Global Infrastructure As Code Market reached a valuation of USD 850.6 million in 2024 and is projected to grow at a remarkable CAGR of 24.1% from 2025 to 2034. This rapid growth is fueled by the escalating adoption of cloud computing and the increasing preference for multi-cloud environments. Organizations worldwide are leveraging multiple cloud providers to mitigate dependency on a single vendor, optimize operational costs, and harness the unique features offered by various cloud platforms. These strategic shifts are driving the demand for IaC solutions, which enable businesses to efficiently manage and automate their complex IT infrastructures. Additionally, the rise of DevOps practices and the growing need for scalable, flexible, and consistent infrastructure management solutions are further propelling market growth. The surge in digital transformation initiatives across industries has also amplified the adoption of IaC, as enterprises aim to accelerate their deployment cycles while ensuring reliability and security.

The market is segmented by enterprise size into small and medium-sized enterprises (SME) and large enterprises. In 2024, large enterprises held a dominant 72% market share, underscoring their significant role in the sector. This segment is poised to generate USD 5 billion by 2034. Large organizations typically operate on a global scale with intricate operations that demand advanced tools to manage diverse workloads, extensive data, and complex systems. These businesses frequently adopt hybrid or multi-cloud strategies, making IaC an essential component of their IT ecosystem. By automating infrastructure provisioning, configuration, and management, IaC enhances operational efficiency, reduces human error, and supports the seamless execution of business-critical processes. The ability to scale resources dynamically while maintaining consistency gives large enterprises a competitive edge in today's fast-paced digital landscape.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $850.6 Million |

| Forecast Value | $7.1 Billion |

| CAGR | 24.1% |

Based on deployment type, the infrastructure as code market is categorized into on-premise and cloud solutions. The cloud segment captured a 65% share in 2024 and is expected to maintain its leadership throughout the forecast period. The growing prevalence of cloud computing among businesses of all sizes has spurred demand for IaC tools that can streamline the management of cloud-based resources. Cloud platforms offer an array of services that require efficient setup, configuration, and scaling. IaC allows organizations to automate these processes using code, ensuring consistent deployments, minimizing manual intervention, and optimizing resource utilization. This synergy between IaC and cloud platforms is pivotal in driving adoption, particularly as companies increasingly prioritize agility and innovation.

The North American infrastructure as code market accounted for 34.5% of the global share in 2024, solidifying its leadership position. This dominance stems from the region's advanced technological landscape and robust focus on cloud computing adoption. The United States, in particular, plays a critical role, housing major technology giants that offer cutting-edge cloud infrastructure services and widely adopted IaC tools. The established presence of these companies has created a thriving ecosystem, ensuring North America remains at the forefront of IaC innovation and growth. With its strong foundation and continued investments in technology, the region is well-positioned to capitalize on the growing demand for efficient, automated infrastructure management solutions.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry 360º synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supplier landscape

- 3.2.1 Cloud service providers

- 3.2.2 IaC tool providers

- 3.2.3 Security and compliance providers

- 3.2.4 System integrators

- 3.2.5 End Use

- 3.3 Profit margin analysis

- 3.4 Technology & innovation landscape

- 3.5 Use cases of IaC

- 3.6 Key news & initiatives

- 3.7 Regulatory landscape

- 3.8 Impact forces

- 3.8.1 Growth drivers

- 3.8.1.1 Growing cloud adoption and multi-cloud environments

- 3.8.1.2 Cost efficiency and resource optimization

- 3.8.1.3 Rising DevOps and CI/CD adoption

- 3.8.1.4 Agility and high speed of deployment

- 3.8.2 Industry pitfalls & challenges

- 3.8.2.1 Increasing security concerns

- 3.8.2.2 Integration challenges with existing systems

- 3.8.1 Growth drivers

- 3.9 Growth potential analysis

- 3.10 Porter’s analysis

- 3.11 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Approach, 2021 - 2034 ($Bn)

- 5.1 Key trends

- 5.2 Declarative

- 5.3 Imperative

Chapter 6 Market Estimates & Forecast, By Organization Size, 2021 - 2034 ($Bn)

- 6.1 Key trends

- 6.2 SME

- 6.3 Large Enterprises

Chapter 7 Market Estimates & Forecast, By Deployment, 2021 - 2034 ($Bn)

- 7.1 Key trends

- 7.2 On-premises

- 7.3 Cloud

Chapter 8 Market Estimates & Forecast, By Infrastructure, 2021 - 2034 ($Bn)

- 8.1 Key trends

- 8.2 Mutable IaC

- 8.3 Immutable IaC

Chapter 9 Market Estimates & Forecast, By End Use, 2021 - 2034 ($Bn)

- 9.1 Key trends

- 9.2 Government

- 9.3 IT & Telecom

- 9.4 Healthcare

- 9.5 BFSI

- 9.6 Manufacturing

- 9.7 Retail

- 9.8 Others

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Russia

- 10.3.7 Nordics

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 ANZ

- 10.4.6 Southeast Asia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 UAE

- 10.6.2 South Africa

- 10.6.3 Saudi Arabia

Chapter 11 Company Profiles

- 11.1 Alibaba Group

- 11.2 Alpacked

- 11.3 Amazon

- 11.4 Cisco

- 11.5 Crossplane

- 11.6 Dell

- 11.7 GitLab

- 11.8 Google

- 11.9 HashiCorp

- 11.10 HPE

- 11.11 IBM

- 11.12 Microsoft

- 11.13 Oracle

- 11.14 Progress Software

- 11.15 Pulumi

- 11.16 Puppet

- 11.17 Rackspace Technology

- 11.18 Red Hat

- 11.19 Snyk

- 11.20 Zscaler

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 180 Pages

- 納期

- 2~3営業日