コンクリート繊維の市場機会、成長促進要因、産業動向分析、2025年~2034年予測

Concrete Fibers Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 235 Pages

- 納期

- 2~3営業日

- 商品コード

- 1666581

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

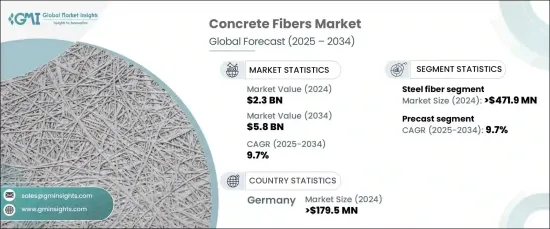

世界のコンクリート繊維市場は、2024年に23億米ドルとなり、2025年から2034年の推定CAGRは9.7%で、力強い成長の態勢を整えています。

この急増は、建設、インフラ、産業用途でコンクリート繊維の使用が増加していることに起因しています。合成繊維、スチール繊維、ガラス繊維、天然繊維を含むこれらの繊維は、コンクリートの強度、耐久性、ひび割れ抵抗性を向上させる上で重要な役割を果たし、現代の建設慣行において不可欠なものとなっています。

建設業界では、コンクリート繊維は住宅、商業、工業構造物の性能と耐用年数を向上させ、同時にメンテナンスコストを削減するために採用されています。特に道路、橋、トンネルなど高い耐久性が要求されるインフラプロジェクトでは、重い荷重や厳しい環境条件に耐えるために繊維補強コンクリートが使用されています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025年~2034年 |

| 開始金額 | 23億米ドル |

| 予測金額 | 58億米ドル |

| CAGR | 9.7% |

持続可能でコスト効率の高い建築ソリューションが重視されるようになり、コンクリート繊維の需要が高まっています。これらの材料は、鉄筋のような伝統的な補強方法への依存を減らし、グリーンな建設慣行や都市開発への世界の後押しと一致します。コンクリート繊維の採用は、発展途上地域におけるインフラの近代化と都市化を目指したイニシアチブによっても支えられており、市場全体の拡大を後押ししています。

スチールファイバー分野は2024年に4億7,190万米ドルを生み出し、2034年までCAGR9%で成長すると予測されています。卓越した機械的特性、高い引張強度、耐久性で知られるスチールファイバーは、耐荷重性と耐衝撃性の強化が必要な用途で広く好まれています。従来の補強方法に取って代わるその能力は、頑丈な建設に不可欠です。

同様に、プレキャストコンクリート分野は2024年に7億2,160万米ドルを占め、2025年から2034年にかけてCAGR9.7%で成長すると予測されています。プレキャストコンクリートに繊維補強材を使用することで、ひび割れ、収縮、環境ストレスに対する耐性が向上し、精密さと耐久性を必要とする建設に好ましい選択肢となります。

ドイツのコンクリート繊維市場は2024年に1億7,950万米ドルを記録し、2034年までのCAGRは8.5%と予想されます。強力な建設部門、持続可能な慣行への注力、大規模なインフラ投資がその主導的地位に貢献しています。建設技術の進歩と、耐久性に優れ、効率的で環境に優しい建材への需要の増加に伴い、コンクリート繊維市場は今後数年で著しい成長を遂げると思われます。

目次

第1章 調査手法と調査範囲

- 市場範囲と定義

- 基本推定と計算

- 予測計算

- データソース

- 一次

- 二次

- 有料ソース

- 公的ソース

第2章 エグゼクティブサマリー

第3章 業界洞察

- 業界エコシステム分析

- バリューチェーンに影響を与える要因

- 利益率分析

- 変革

- 将来の展望

- メーカー

- 流通業者

- サプライヤーの状況

- 利益率分析

- 主要ニュース

- 規制状況

- 影響要因

- 成長促進要因

- 北米:米国の商業建設業界の回復

- アジア太平洋:建設業界の成長

- アジア太平洋と中東のインフラプロジェクトの増加

- 業界の潜在的リスク・課題

- 原材料価格の変動

- 成長促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業市場シェア分析

- 競合のポジショニングマトリックス

- 戦略展望マトリックス

第5章 市場推計・予測:製品別、2021年~2034年

- 主要動向

- スチール繊維

- 合成繊維

- ポリプロピレン

- ナイロン

- ポリエステル

- その他

- ガラス繊維

- 天然繊維

- バサルト繊維

第6章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- 舗装

- 吹付けコンクリート

- プレキャスト

- スラブ

- 複合金属デッキ

- その他

第7章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 住宅

- 産業・商業インフラ

- 道路・橋梁

- その他

第8章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- ラテンアメリカ

- ブラジル

- メキシコ

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第9章 企業プロファイル

- BASF SE

- ABC Polymer Industries

- Bekaert SA

- CEMEX S.A.B. de C.V.

- Fibercon International

- GCP Applied Technologies

- Nycon Corporation

- Owens Corning

- Sika AG

- The Euclid Chemical Company

目次

The Global Concrete Fibers Market was valued at USD 2.3 billion in 2024 and is poised for robust growth, with an estimated CAGR of 9.7% during 2025 - 2034. This surge is attributed to the increasing use of concrete fibers across construction, infrastructure, and industrial applications. These fibers, including synthetic, steel, glass, and natural variants, play a critical role in enhancing the strength, durability, and crack resistance of concrete, making them indispensable in modern construction practices.

In the construction industry, concrete fibers are being adopted to improve the performance and longevity of residential, commercial, and industrial structures while reducing maintenance costs. Infrastructure projects, especially those requiring high durability, such as roads, bridges, and tunnels, use fiber-reinforced concrete to withstand heavy loads and challenging environmental conditions.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.3 Billion |

| Forecast Value | $5.8 Billion |

| CAGR | 9.7% |

A growing emphasis on sustainable and cost-efficient building solutions drives the demand for concrete fibers. These materials reduce reliance on traditional reinforcement methods like steel bars, aligning with the global push toward green construction practices and urban development. The adoption of concrete fibers is also supported by initiatives aimed at infrastructure modernization and urbanization in developing regions, fueling overall market expansion.

The steel fiber segment generated USD 471.9 million in 2024 and is projected to grow at a CAGR of 9% through 2034. Known for their exceptional mechanical properties, high tensile strength, and durability, steel fibers are widely preferred in applications requiring enhanced load-bearing capacity and impact resistance. Their ability to replace conventional reinforcement methods makes them vital in heavy-duty construction.

Similarly, the precast concrete segment accounted for USD 721.6 million in 2024 and is forecasted to grow at a 9.7% CAGR during 2025-2034. Using fiber reinforcement in precast concrete improves its resistance to cracking, shrinkage, and environmental stress, making it a preferred choice for construction requiring precision and durability.

Germany concrete fibers market recorded USD 179.5 million in 2024, with an expected CAGR of 8.5% through 2034. Its strong construction sector, focus on sustainable practices, and significant infrastructure investments contribute to its leading position. With advancements in construction technologies and increasing demand for durable, efficient, and eco-friendly building materials, the concrete fibers market is set to achieve remarkable growth in the coming years.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Key news & initiatives

- 3.5 Regulatory landscape

- 3.6 Impact forces

- 3.6.1 Growth drivers

- 3.6.1.1 North America: Recovering U.S. commercial construction industry

- 3.6.1.2 Asia Pacific: Growing construction industry

- 3.6.1.3 Increasing Asia pacific and Middle east infrastructure projects

- 3.6.2 Industry pitfalls & challenges

- 3.6.2.1 Fluctuating raw material prices

- 3.6.1 Growth drivers

- 3.7 Growth potential analysis

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Product, 2021-2034 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Steel fibers

- 5.3 Synthetic fibers

- 5.3.1 Polypropylene

- 5.3.2 Nylon

- 5.3.3 Polyester

- 5.3.4 Others

- 5.4 Glass fibers

- 5.5 Natural fibers

- 5.6 Basalt fibers

Chapter 6 Market Estimates & Forecast, By Application, 2021-2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Pavement

- 6.3 Shotcrete

- 6.4 Precast

- 6.5 Slabs on grade

- 6.6 Composite metal decks

- 6.7 Others

Chapter 7 Market Estimates & Forecast, By End Use, 2021-2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Residential

- 7.3 Industrial & commercial infrastructure

- 7.4 Roads & bridges

- 7.5 Others

Chapter 8 Market Estimates & Forecast, By Region, 2021-2034 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 UK

- 8.3.2 Germany

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Russia

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 South Korea

- 8.4.5 Australia

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.6 MEA

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 BASF SE

- 9.2 ABC Polymer Industries

- 9.3 Bekaert SA

- 9.4 CEMEX S.A.B. de C.V.

- 9.5 Fibercon International

- 9.6 GCP Applied Technologies

- 9.7 Nycon Corporation

- 9.8 Owens Corning

- 9.9 Sika AG

- 9.10 The Euclid Chemical Company

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 235 Pages

- 納期

- 2~3営業日