代替燃料噴射システム市場の機会、成長促進要因、産業動向分析、2025~2034年の予測

Alternative Fuel Injection Systems Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 175 Pages

- 納期

- 2~3営業日

- 商品コード

- 1665434

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

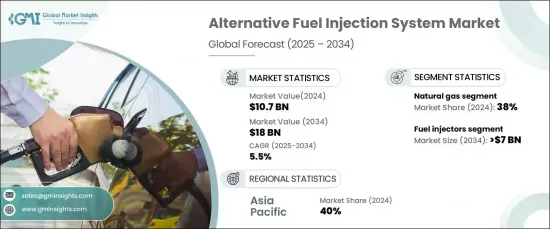

世界の代替燃料噴射システム市場は、2024年には107億米ドルとなり、2025年から2034年にかけて5.5%のCAGRで堅調に成長すると予測されています。

圧縮(CNG)や液化(LNG)形態の天然ガスなど、費用対効果が高く環境に優しい燃料オプションに対する需要の高まりが、この成長を後押ししています。これらの燃料は、バスやトラックなどのフリート車両にますます好まれるようになっており、燃焼効率を最大化するように設計された高度な噴射システムが必要とされています。

代替燃料噴射システム市場は、電子制御ユニット(ECU)、燃料インジェクター、燃料レール、圧力レギュレーターに区分されます。このうち、燃料噴射装置は2024年に市場シェアの40%を占め、2034年には70億米ドルに達すると予測されています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 107億米ドル |

| 予測金額 | 180億米ドル |

| CAGR | 5.5% |

インジェクター技術の革新は、正確な燃料供給を可能にすることで市場に革命をもたらし、エンジン効率の向上と無駄の削減を実現しています。水素や天然ガスのような代替燃料に対応する耐久性のあるインジェクターに対する需要の高まりは、より厳しい排出規制と性能の最適化の継続的な推進によってさらに加速しています。高強度合金や保護コーティングなど、材料科学の進歩がインジェクターの耐久性と機能性を高め、その採用を大幅に後押ししています。

市場は、水素、LPG、バイオ燃料、天然ガス、その他の代替燃料に分類されます。2024年には、天然ガス・セグメントが市場の38%を占め、最大のシェアを占めています。その人気は、従来の燃料に比べて価格が手ごろで炭素排出量が少ないことが主な理由であり、商業用車両や公共交通機関にとって魅力的な選択肢となっています。北米とアジア太平洋全域で政府の支援政策が天然ガスへの移行を加速させており、その背景には運用コストの削減と持続可能性の向上があります。天然ガス燃焼を最適化するために調整された先進燃料噴射システムは、この急増する需要に対応するために開発されています。

アジア太平洋地域は、2024年の代替燃料噴射システム市場の40%を占め、日本、インド、韓国などの国々がよりクリーンなエネルギー・ソリューションへのシフトの最前線にあります。この地域の各国政府は、補助金、税制優遇、助成金などさまざまな取り組みを通じて代替燃料を推進しています。都市汚染対策と大気質改善への取り組みが、先進燃料噴射技術の採用をさらに後押ししています。持続可能性とよりクリーンな輸送を重視するアジア太平洋地域は、今後も市場成長の重要な原動力であり続けると思われます。

目次

第1章 調査手法と調査範囲

- 調査デザイン

- 調査アプローチ

- データ収集方法

- 基本推定と計算

- 基準年の算出

- 市場推計の主要動向

- 予測モデル

- 1次調査と検証

- 一次情報

- データマイニングソース

- 市場範囲と定義

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- 原材料サプライヤー

- 部品サプライヤー

- メーカー

- エンドユーザー

- サプライヤーの状況

- 利益率分析

- 技術革新の状況

- 特許分析

- 主要ニュース&イニシアチブ

- 規制状況

- 価格分析

- 影響要因

- 促進要因

- 政府による厳しい排出ガス規制

- よりクリーンで持続可能な輸送ソリューションへの需要の高まり

- 代替燃料としての天然ガスと水素の採用増加

- 性能向上のための燃料噴射システムの技術進歩

- 業界の潜在的リスク&課題

- 代替燃料噴射システムの初期コストの高さ

- 代替燃料の入手可能性とインフラが限定的

- 促進要因

- 成長可能性分析

- ポーターの分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 競合のポジショニング・マトリックス

- 戦略展望マトリックス

第5章 市場推計・予測:燃料別、2021年~2034年

- 主要動向

- 天然ガス

- 水素

- LPG

- バイオ燃料

- その他

第6章 市場推計・予測:コンポーネント別、2021年~2034年

- 主要動向

- フューエルインジェクター

- フューエルレール

- 電子制御ユニット(ECU)

- 圧力調整器

第7章 市場推計・予測:技術別、2021年~2034年

- 主要動向

- ポート噴射

- ダイレクトインジェクション

- デュアル燃料システム

- シーケンシャルインジェクション

第8章 市場推計・予測:自動車別、2021年~2034年

- 主要動向

- 乗用車

- セダン

- ハッチバック

- SUV車

- 商用車

- 小型商用車(LCV)

- 大型商用車(HCV)

- オフロード車

- 建設機械

- 鉱山機械

第9章 市場推計・予測:販売チャネル別、2021年~2034年

- 主要動向

- OEM

- アフターマーケット

第10章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- 北欧

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- UAE

- 南アフリカ

- サウジアラビア

第11章 企業プロファイル

- Aptiv

- Bosch

- Continental

- Cummins

- Delphi(Phinia)

- Denso

- Eaton

- Honeywell

- Infineon

- Magneti Marelli

- Mitsubishi

- Pierburg

- Ricardo plc

- Schaeffler

- Tenneco

- Valeo

- Weichai

- Westport Fuel Systems

- Woodward

- Zexel

目次

The Global Alternative Fuel Injection Systems Market was valued at USD 10.7 billion in 2024 and is anticipated to grow at a robust CAGR of 5.5% between 2025 and 2034. The rising demand for cost-effective and eco-friendly fuel options, such as natural gas in its compressed (CNG) and liquefied (LNG) forms, is driving this growth. These fuels are increasingly preferred for fleet vehicles like buses and trucks, necessitating advanced injection systems designed to maximize combustion efficiency.

The alternative fuel injection systems market is segmented into electronic control units (ECUs), fuel injectors, fuel rails, and pressure regulators. Among these, the fuel injectors segment dominated in 2024, capturing 40% of the market share, and is projected to reach USD 7 billion by 2034.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $10.7 Billion |

| Forecast Value | $18 Billion |

| CAGR | 5.5% |

Innovations in injector technology are revolutionizing the market by enabling precise fuel delivery, which improves engine efficiency and reduces waste. The growing demand for durable injectors compatible with alternative fuels like hydrogen and natural gas is further fueled by stricter emission regulations and the ongoing push for performance optimization. Advances in materials science-such as high-strength alloys and protective coatings-are enhancing injector durability and functionality, significantly boosting their adoption.

The market is categorized into hydrogen, LPG, biofuels, natural gas, and other alternatives. In 2024, the natural gas segment held the largest share, accounting for 38% of the market. Its popularity is largely attributed to its affordability and lower carbon emissions compared to traditional fuels, making it an attractive choice for commercial fleets and public transportation. Supportive government policies across North America and Asia-Pacific are accelerating the transition to natural gas, driven by its potential to reduce operational costs and improve sustainability. Advanced fuel injection systems tailored for optimized natural gas combustion are being developed to meet this surging demand.

The Asia-Pacific region accounted for 40% of the alternative fuel injection systems market in 2024, with countries like Japan, India, and South Korea at the forefront of the shift toward cleaner energy solutions. Governments in this region are promoting alternative fuels through various initiatives, including subsidies, tax benefits, and grants. Efforts to combat urban pollution and enhance air quality are further propelling the adoption of advanced fuel injection technologies. With a strong emphasis on sustainability and cleaner transportation, Asia-Pacific is poised to remain a critical driver for market growth.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates & calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimation

- 1.3 Forecast model

- 1.4 Primary research and validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market scope & definition

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Raw material suppliers

- 3.1.2 Component suppliers

- 3.1.3 Manufacturers

- 3.1.4 End users

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Technology & innovation landscape

- 3.5 Patent analysis

- 3.6 Key news & initiatives

- 3.7 Regulatory landscape

- 3.8 Pricing analysis

- 3.9 Impact forces

- 3.9.1 Growth drivers

- 3.9.1.1 Stringent government regulations on emissions

- 3.9.1.2 Growing demand for cleaner and sustainable transportation solutions

- 3.9.1.3 Rising adoption of natural gas and hydrogen as alternative fuels

- 3.9.1.4 Technological advancements in fuel injection systems for enhanced performance

- 3.9.2 Industry pitfalls & challenges

- 3.9.2.1 High initial cost of alternative fuel injection systems

- 3.9.2.2 Limited availability and infrastructure for alternative fuels

- 3.9.1 Growth drivers

- 3.10 Growth potential analysis

- 3.11 Porter’s analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Fuel, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 Natural gas

- 5.3 Hydrogen

- 5.4 LPG

- 5.5 Biofuels

- 5.6 Others

Chapter 6 Market Estimates & Forecast, By Component, 2021 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 Fuel injectors

- 6.3 Fuel rails

- 6.4 Electronic Control Unit (ECU)

- 6.5 Pressure regulators

Chapter 7 Market Estimates & Forecast, By Technology, 2021 - 2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 Port injection

- 7.3 Direct injection

- 7.4 Dual fuel systems

- 7.5 Sequential injection

Chapter 8 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 Passenger cars

- 8.2.1 Sedans

- 8.2.2 Hatchbacks

- 8.2.3 SUVs

- 8.3 Commercial vehicles

- 8.3.1 Light Commercial Vehicles (LCV)

- 8.3.2 Heavy Commercial Vehicles (HCV)

- 8.4 Off-road Vehicles

- 8.4.1 Construction Equipment

- 8.4.2 Mining Equipment

Chapter 9 Market Estimates & Forecast, By Sales Channel, 2021 - 2034 ($Bn, Units)

- 9.1 Key trends

- 9.2 OEM

- 9.3 Aftermarket

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.3.7 Nordics

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Southeast Asia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 UAE

- 10.6.2 South Africa

- 10.6.3 Saudi Arabia

Chapter 11 Company Profiles

- 11.1 Aptiv

- 11.2 Bosch

- 11.3 Continental

- 11.4 Cummins

- 11.5 Delphi (Phinia)

- 11.6 Denso

- 11.7 Eaton

- 11.8 Honeywell

- 11.9 Infineon

- 11.10 Magneti Marelli

- 11.11 Mitsubishi

- 11.12 Pierburg

- 11.13 Ricardo plc

- 11.14 Schaeffler

- 11.15 Tenneco

- 11.16 Valeo

- 11.17 Weichai

- 11.18 Westport Fuel Systems

- 11.19 Woodward

- 11.20 Zexel

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 175 Pages

- 納期

- 2~3営業日