石油・ガスにおける検査用ドローン市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測

Inspection Drone in Oil and Gas Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 170 Pages

- 納期

- 2~3営業日

- 商品コード

- 1665414

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

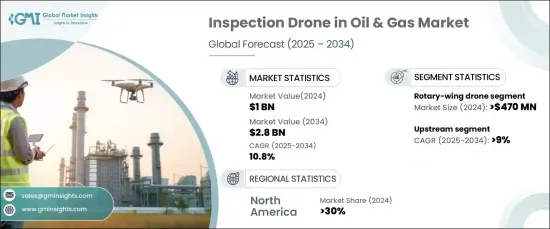

石油・ガスにおける検査用ドローンの世界市場は、2024年に10億米ドルと評価され、2025年から2034年にかけてCAGR 10.8%で成長すると予測されています。

この成長には、効率的な監視ソリューションに対する需要の高まりとドローン技術の急速な進歩が寄与しています。企業は、オペレーションの改善、リスクの低減、安全性の向上のために、革新的な検査システムの開発を優先しています。日常点検、インフラ評価、業務監視のためのドローンの利用増加により、同分野における従来の点検業務が大きく変化しています。安全性と環境コンプライアンスに対する規制要件の厳格化も、従来の方法に代わるより迅速で信頼性の高い代替手段を提供するドローン技術の採用を後押ししています。さらに、AIと機械学習をドローンシステムに組み込むことで、データ分析に革命をもたらし、リアルタイムの洞察と合理化された意思決定プロセスを可能にしています。自動化と業務効率の重視は、引き続き市場の軌道を形成しています。

市場はドローンの種類によって、回転翼ドローン、固定翼ドローン、ハイブリッドドローンに区分されます。回転翼ドローンは、2024年にかなりの市場シェアを占め、金額で4億7,000万米ドルを超えました。これらのドローンは、限られたスペースでホバリングして操縦する能力により広く好まれており、パイプラインやオフショアプラットフォームのような固定資産の検査に最適です。その使用は、従来の検査方法に関連する時間とコストを削減しながら、安全性と効率を向上させています。企業がますますAI対応技術を統合するにつれて、回転翼ドローンの需要は、リアルタイムのデータに基づく意思決定能力の向上を提供し、さらに成長すると予想されます。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 10億米ドル |

| 予測金額 | 28億米ドル |

| CAGR | 10.8% |

市場はまた、事業タイプ別に上流、中流、下流の各セグメントに分類されます。上流セグメントは、2025年から2034年にかけてCAGR 9%以上の堅調な伸びが予測されています。この成長は、特に遠隔地や困難な場所での探査現場、掘削作業、パイプラインの高度な監視に対するニーズの高まりに起因しています。ドローンは、安全性を高め、検査時間を最小化し、運用コストを最適化することで、上流作業にとって不可欠なツールになりつつあります。探査活動への投資の増加と持続可能性への注目は、このセグメントにおける検査用ドローンの需要をさらに増幅させています。

北米は2024年に世界市場をリードし、収益シェアの30%以上を獲得しました。特に米国は、業務効率と厳格な安全規制の遵守を重視しているため、大きな成長を遂げています。AIや機械学習のような先進技術をドローンシステムに統合することで、リアルタイムのデータ分析が可能になり、企業がプロセスを合理化し、潜在的な問題を迅速に特定し、ダウンタイムを削減するのに役立っています。イノベーションと効率性を重視するこの地域の姿勢は、引き続き市場の成長を後押ししています。

目次

第1章 調査手法と調査範囲

- 調査デザイン

- 調査アプローチ

- データ収集方法

- 基本推定と計算

- 基準年の算出

- 市場推計の主要動向

- 予測モデル

- 1次調査と検証

- 一次情報

- データマイニングソース

- 市場範囲と定義

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- サプライヤーの状況

- 部品メーカー

- メーカー

- 流通業者

- 最終用途

- 利益率分析

- 技術とイノベーションの展望

- 特許分析

- 規制状況

- 使用事例

- 使用事例1

- 利点

- 投資収益率

- 使用事例2

- 利点

- 投資利益率

- 使用事例1

- ケーススタディ

- ケーススタディ1

- 消費者名

- 課題

- 解決策

- 影響

- ケーススタディ2

- 消費者名

- 課題

- 解決策

- 影響

- ケーススタディ1

- 影響要因

- 促進要因

- リアルタイムモニタリングへの需要の高まり

- ドローンの技術的進歩

- 資産管理ソリューションに対する需要の高まり

- 遠隔検査における安全プロトコルの強化

- 業界の潜在的リスク&課題

- データ統合と分析における課題

- 高度なドローンシステムの導入に伴う高コスト

- 促進要因

- 成長可能性分析

- ポーターの分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 競合のポジショニング・マトリックス

- 戦略展望マトリックス

第5章 市場推計・予測:ドローン別、2021年~2034年

- 主要動向

- 固定翼ドローン

- 回転翼ドローン

- ハイブリッドドローン

第6章 市場推計・予測:ペイロード別、2021年~2034年

- 主要動向

- カメラ

- LiDAR

- ガス検知器

- その他

第7章 市場推計・予測:動作別、2021年~2034年

- 主要動向

- 上流

- 中流

- 下流

第8章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- パイプライン検査

- フレアスタック検査

- タンク検査

- 環境モニタリング

- 坑井検査

- その他

第9章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 国営石油会社(NOC)

- 独立系石油会社(IOC)

第10章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- 北欧

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- UAE

- 南アフリカ

- サウジアラビア

第11章 企業プロファイル

- 3D Robotics

- Airobotics

- Autel Robotics

- Cyberhawk

- DJI Enterprise

- DroneBase

- DroneDeploy

- FLIR Systems

- Flyability

- GRIFF Aviation

- IdeaForge

- InspecTech Aero Services

- Kespry

- Percepto

- PrecisionHawk

- Quantum Systems

- senseFly

- Sky-Futures(ICR Group)

- Terra Drone

- Vantage Robotics

目次

The Global Inspection Drone In Oil And Gas Market was valued at USD 1 billion in 2024 and is projected to grow at a CAGR of 10.8% from 2025 to 2034. This growth is fueled by the rising demand for efficient monitoring solutions and the rapid advancements in drone technology. Companies are prioritizing the development of innovative inspection systems to improve operations, reduce risks, and enhance safety. The increasing use of drones to conduct routine checks, assess infrastructure, and monitor operations has significantly transformed traditional inspection practices in the sector. Stricter regulatory requirements for safety and environmental compliance are also driving the adoption of drone technologies, which offer a faster and more reliable alternative to conventional methods. Additionally, incorporating AI and machine learning into drone systems is revolutionizing data analysis, enabling real-time insights and streamlined decision-making processes. The focus on automation and operational efficiency continues to shape the market's trajectory.

The market is segmented by drone type into rotary-wing, fixed-wing, and hybrid drones. Rotary-wing drones held a substantial market share in 2024, exceeding USD 470 million in value. These drones are widely preferred due to their ability to hover and maneuver in confined spaces, making them ideal for inspecting stationary assets like pipelines and offshore platforms. Their use enhances safety and efficiency while reducing the time and cost associated with traditional inspection methods. As companies increasingly integrate AI-enabled technologies, the demand for rotary-wing drones is expected to grow further, offering improved decision-making capabilities based on real-time data.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1 Billion |

| Forecast Value | $2.8 Billion |

| CAGR | 10.8% |

The market is also categorized by operation type into upstream, midstream, and downstream segments. The upstream segment is forecasted to witness a robust CAGR of over 9% between 2025 and 2034. This growth is attributed to the rising need for advanced monitoring of exploration sites, drilling operations, and pipelines, especially in remote and challenging locations. Drones are becoming an indispensable tool for upstream operations by enhancing safety, minimizing inspection times, and optimizing operational costs. Increased investments in exploration activities and a focus on sustainability further amplify the demand for inspection drones in this segment.

North America led the global market in 2024, capturing over 30% of the revenue share. The United States, in particular, has seen significant growth due to its emphasis on operational efficiency and compliance with stringent safety regulations. The integration of advanced technologies like AI and machine learning into drone systems is enabling real-time data analysis, helping companies streamline processes, identify potential issues quickly, and reduce downtime. The region's strong focus on innovation and efficiency continues to bolster market growth.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates & calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimation

- 1.3 Forecast model

- 1.4 Primary research and validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market scope & definition

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supplier landscape

- 3.2.1 Component providers

- 3.2.2 Manufacturer

- 3.2.3 Distributors

- 3.2.4 End use

- 3.3 Profit margin analysis

- 3.4 Technology & innovation landscape

- 3.5 Patent analysis

- 3.6 Regulatory landscape

- 3.7 Used cases

- 3.7.1 Used case 1

- 3.7.1.1 Benefits

- 3.7.1.2 ROI

- 3.7.2 Used case 2

- 3.7.2.1 Benefits

- 3.7.2.2 ROI

- 3.7.1 Used case 1

- 3.8 Case study

- 3.8.1 Case study 1

- 3.8.1.1 Consumer name

- 3.8.1.2 Challenge

- 3.8.1.3 Solution

- 3.8.1.4 Impact

- 3.8.2 Case study 2

- 3.8.2.1 Consumer name

- 3.8.2.2 Challenge

- 3.8.2.3 Solution

- 3.8.2.4 Impact

- 3.8.1 Case study 1

- 3.9 Impact forces

- 3.9.1 Growth drivers

- 3.9.1.1 Increasing demand for real-time monitoring

- 3.9.1.2 Technological advancements in drone capabilities

- 3.9.1.3 Rising demand for asset management solutions

- 3.9.1.4 Enhanced safety protocols for remote inspections

- 3.9.2 Industry pitfalls & challenges

- 3.9.2.1 Challenges in data integration and analysis

- 3.9.2.2 High costs associated with implementing advanced drone systems

- 3.9.1 Growth drivers

- 3.10 Growth potential analysis

- 3.11 Porter’s analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Drone, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 Fixed-wing drone

- 5.3 Rotary-wing drone

- 5.4 Hybrid drone

Chapter 6 Market Estimates & Forecast, By Payload, 2021 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 Cameras

- 6.3 LiDAR

- 6.4 Gas detectors

- 6.5 Others

Chapter 7 Market Estimates & Forecast, By Operation, 2021 - 2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 Upstream

- 7.3 Midstream

- 7.4 Downstream

Chapter 8 Market Estimates & Forecast, By Application, 2021 - 2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 Pipeline inspection

- 8.3 Flare stack inspection

- 8.4 Tank inspection

- 8.5 Environmental monitoring

- 8.6 Well site inspection

- 8.7 Others

Chapter 9 Market Estimates & Forecast, By End Use, 2021 - 2034 ($Bn, Units)

- 9.1 Key trends

- 9.2 National Oil Companies (NOCs)

- 9.3 Independent Oil Companies (IOCs)

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.3.7 Nordics

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Southeast Asia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 UAE

- 10.6.2 South Africa

- 10.6.3 Saudi Arabia

Chapter 11 Company Profiles

- 11.1 3D Robotics

- 11.2 Airobotics

- 11.3 Autel Robotics

- 11.4 Cyberhawk

- 11.5 DJI Enterprise

- 11.6 DroneBase

- 11.7 DroneDeploy

- 11.8 FLIR Systems

- 11.9 Flyability

- 11.10 GRIFF Aviation

- 11.11 IdeaForge

- 11.12 InspecTech Aero Services

- 11.13 Kespry

- 11.14 Percepto

- 11.15 PrecisionHawk

- 11.16 Quantum Systems

- 11.17 senseFly

- 11.18 Sky-Futures (ICR Group)

- 11.19 Terra Drone

- 11.20 Vantage Robotics

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 170 Pages

- 納期

- 2~3営業日