農業用肥料散布機の市場機会、成長促進要因、産業動向分析、2025年~2034年予測

Agriculture Fertilizer Spreader Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 175 Pages

- 納期

- 2~3営業日

- 商品コード

- 1665378

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

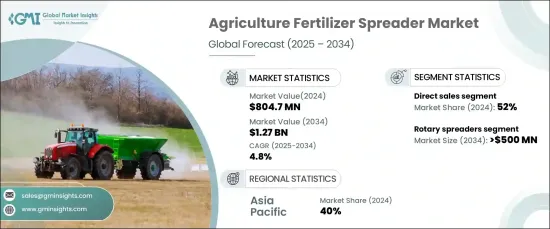

農業用肥料散布機の世界市場は、2024年に8億470万米ドルと評価され、2025~2034年にかけてCAGR 4.8%で成長すると予測されています。

この拡大は、人口増加に伴う世界の食糧需要の増加が原動力となっています。都市化や環境課題によって耕地が減少する中、効率的な農業技術が不可欠となっています。肥料散布機は、養分を正確に散布し、無駄を最小限に抑え、作物の収量を高めるという重要な役割を果たします。この効率性は持続可能性の目標にも合致しており、食料生産を向上させながら環境への影響を減らすことができます。土壌の劣化、気候変動、不適切な農業プラクティスといった課題が、土壌浸食や養分の損失に対処するこのような先進的なツールの必要性を高めています。可変施肥量や土壌モニタリングなどの先進技術を搭載した最新の肥料散布機は、世界の食糧安全保障を確保し、農業生産を最適化するために不可欠です。

農業の近代化を促進する政府の取り組みは、市場の成長をさらに後押しします。補助金、助成金、財政的インセンティブは、農業従事者が肥料散布機のような先進機器を導入することを奨励しています。例えば、農業経済国の予算の大部分は食糧と肥料の補助金に割り当てられており、農業の近代化に対するコミットメントが強調されています。こうした財政支援は、先端機器への初期投資を支援するだけでなく、小規模農業従事者が経済的障壁を克服するのを助け、より広範な導入を促進します。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025~2034年 |

| 開始金額 | 8億470万米ドル |

| 予測金額 | 12億7,000万米ドル |

| CAGR | 4.8% |

市場は、ロータリー、乾式、落下式、振り子式、液体散布機など、散布機タイプによって区分されます。このうち、回転式散布機は2024年に40%以上の圧倒的な市場シェアを占め、2034年には5億米ドルを超えると予測されています。その人気の理由は、広い面積を効率的にカバーし、多様な種類の肥料を扱えることにあります。この適応性により、さまざまな農業用途に適しており、農業セクター全体の需要を高めています。

肥料散布機の流通は直接販売、小売、オンラインプラットフォームを通じて行われ、2024年には直接販売が52%で市場をリードします。農業従事者が直接販売を好むのは、個による相談に応じ、ニーズに合った機器を確実に提供するためです。これらのチャネルはまた、アフターサービス、保証、リースや割賦プランのような柔軟な資金調達オプションを促進し、特に発展途上地域の農業従事者が容易にアクセスできるようにします。

アジア太平洋は2024年に40%のシェアを占め、中国のような国々が市場を牽引しています。この地域では、労働力不足と食糧需要の増加に対応するため、農業の機械化が急速に進んでいます。肥料散布機は、農法の近代化を目指す政府の施策やイニシアティブに支えられ、生産性を向上させるために不可欠です。精密農業技術やサステイナブル農法の採用は、これらのツールに対する需要をさらに加速させ、効率的な資源利用と環境への影響の低減を確実なものにしています。

目次

第1章 調査手法と調査範囲

- 調査デザイン

- 調査アプローチ

- データ収集方法

- 基本推定と計算

- 基準年の算出

- 市場推定の主要動向

- 予測モデル

- 一次調査と検証

- 一次情報

- データマイニングソース

- 市場スコープと定義

第2章 エグゼクティブサマリー

第3章 産業洞察

- エコシステム分析

- 原料・部品サプライヤー

- メーカー

- 技術プロバイダー

- 流通業者

- エンドユーザー

- サプライヤーの状況

- 利益率分析

- 技術とイノベーションの展望

- 特許分析

- 主要ニュース&イニシアチブ

- 規制状況

- 価格分析

- 影響要因

- 促進要因

- 世界の食糧需要の増加により、効率的な農法が必要となります。

- GPS対応散布機などの精密農業技術の採用

- 持続可能性への取り組みが効率的な肥料散布ツールの需要を促進

- 近代的農業機器に対する政府の補助金と支援

- 産業の潜在的リスク・課題

- 先進的肥料散布機の初期コストの高さ

- 小規模農業従事者の認識と技術的専門知識の欠如

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 競合のポジショニングマトリックス

- 戦略展望マトリックス

第5章 市場推定・予測:散布機別、2021~2034年

- 主要動向

- ロータリー散布機

- 乾式散布機

- 落下式散布機

- 振り子式散布機

- 液体散布機

第6章 市場推定・予測:肥料別、2021~2034年

- 主要動向

- 粒状肥料

- 液体肥料

- 有機肥料

- 化学肥料

第7章 市場推定・予測:技術別、2021~2034年

- 主要動向

- 手動式

- 油圧式

- GPS対応

- 可変レート技術(VRT)

- 無線通信システム

第8章 市場推定・予測:動力源別、2021~2034年

- 主要動向

- トラクター搭載型

- 自走式

- 手押し式

- ATV/UTV搭載

第9章 市場推定・予測:用途別、2021~2034年

- 主要動向

- 畝作物

- 果樹園

- 業務用芝生と庭園

第10章 市場推定・予測:流通チャネル別、2021~2034年

- 主要動向

- 直接販売

- 小売

- オンラインプラットフォーム

第11章 地域別市場推定・予測:地域別、2021~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- 北欧

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- アラブ首長国連邦

- 南アフリカ

- サウジアラビア

第12章 企業プロファイル

- AGCO

- Bogballe

- Bredal

- Claas

- CNH Industrial

- Dalton

- Fertilizer Equipment Specialists

- IRIS Spreaders

- John Deere

- Kasco Manufacturing

- Kubota

- Kuhn

- Kverneland

- Mahindra &Mahindra

- Maschio Gaspardo

- Monosem

- Rauch Landmaschinenfabrik

- Sulky Burel

- Techint

- Vicon

目次

The Global Agriculture Fertilizer Spreader Market, valued at USD 804.7 million in 2024, is projected to grow at a 4.8% CAGR from 2025 to 2034. This expansion is driven by the rising global demand for food, necessitated by population growth. As urbanization and environmental challenges reduce arable land, efficient farming techniques become essential. Fertilizer spreaders play a critical role by applying nutrients precisely, minimizing waste, and boosting crop yields. This efficiency also aligns with sustainability objectives, reducing environmental impact while improving food production. Challenges like soil degradation, climate change, and poor agricultural practices exacerbate the need for such advanced tools, which address soil erosion and nutrient loss. Modern fertilizer spreaders, featuring advanced technologies like variable rate application and soil monitoring, are indispensable for ensuring global food security and optimizing agricultural output.

Government initiatives promoting agricultural modernization further bolster market growth. Subsidies, grants, and financial incentives encourage farmers to adopt advanced equipment like fertilizer spreaders. For instance, a significant portion of budgets in agrarian economies is allocated to food and fertilizer subsidies, underscoring the commitment to modernizing agriculture. These financial aids not only support the initial investment in advanced tools but also help small-scale farmers overcome economic barriers, fostering broader adoption.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $804.7 Million |

| Forecast Value | $1.27 Billion |

| CAGR | 4.8% |

The market is segmented based on spreader types, including rotary, dry, drop, pendulum, and liquid spreaders. Among these, rotary spreaders held a dominant market share of over 40% in 2024, with projections exceeding USD 500 million by 2034. Their popularity stems from their ability to cover large areas efficiently and handle diverse fertilizer types. This adaptability makes them suitable for various agricultural applications, enhancing their demand across the farming sector.

The distribution of fertilizer spreaders occurs through direct sales, retail, and online platforms, with direct sales leading the market at 52% in 2024. Farmers favor direct sales due to personalized consultations and tailored solutions that ensure the right equipment for their needs. These channels also facilitate after-sales services, warranties, and flexible financing options like leasing and installment plans, enabling easier access for farmers, particularly in developing regions.

Asia Pacific dominated the market with a 40% share in 2024, led by countries like China. The region is experiencing rapid agricultural mechanization to address labor shortages and increasing food demands. Fertilizer spreaders are integral to improving productivity supported by government policies and initiatives aimed at modernizing farming practices. The adoption of precision farming techniques and sustainable practices further accelerates the demand for these tools, ensuring efficient resource use and reduced environmental impact.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates & calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimation

- 1.3 Forecast model

- 1.4 Primary research and validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market scope & definition

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Raw material and component suppliers

- 3.1.2 Manufacturers

- 3.1.3 Technology providers

- 3.1.4 Distributors

- 3.1.5 End users

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Technology & innovation landscape

- 3.5 Patent analysis

- 3.6 Key news & initiatives

- 3.7 Regulatory landscape

- 3.8 Pricing analysis

- 3.9 Impact forces

- 3.9.1 Growth drivers

- 3.9.1.1 Increasing global food demand necessitates efficient agricultural practices

- 3.9.1.2 Adoption of precision agriculture technologies such as GPS-enabled spreaders

- 3.9.1.3 Sustainability efforts drive demand for efficient fertilizer application tools

- 3.9.1.4 Government subsidies and support for modern farming equipment

- 3.9.2 Industry pitfalls & challenges

- 3.9.2.1 High initial costs of advanced fertilizer spreaders

- 3.9.2.2 Lack of awareness and technical expertise among small-scale farmers

- 3.9.1 Growth drivers

- 3.10 Growth potential analysis

- 3.11 Porter’s analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Spreader, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 Rotary spreaders

- 5.3 Dry spreaders

- 5.4 Drop spreaders

- 5.5 Pendulum spreaders

- 5.6 Liquid spreaders

Chapter 6 Market Estimates & Forecast, By Fertilizer, 2021 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 Granular fertilizers

- 6.3 Liquid fertilizers

- 6.4 Organic fertilizers

- 6.5 Chemical fertilizers

Chapter 7 Market Estimates & Forecast, By Technology, 2021 - 2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 Manual

- 7.3 Hydraulic

- 7.4 GPS-enabled

- 7.5 Variable rate technology (VRT)

- 7.6 Wireless communication systems

Chapter 8 Market Estimates & Forecast, By Power Source, 2021 - 2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 Tractor-mounted

- 8.3 Self-propelled

- 8.4 Hand-pushed

- 8.5 ATV/UTV mounted

Chapter 9 Market Estimates & Forecast, By Application, 2021 - 2034 ($Bn, Units)

- 9.1 Key trends

- 9.2 Row crops

- 9.3 Orchards

- 9.4 Commercial lawns & gardens

Chapter 10 Market Estimates & Forecast, By Distribution Channel, 2021 - 2034 ($Bn, Units)

- 10.1 Key trends

- 10.2 Direct sales

- 10.3 Retail

- 10.4 Online platforms

Chapter 11 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 UK

- 11.3.2 Germany

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.3.6 Russia

- 11.3.7 Nordics

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.4.6 Southeast Asia

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 MEA

- 11.6.1 UAE

- 11.6.2 South Africa

- 11.6.3 Saudi Arabia

Chapter 12 Company Profiles

- 12.1 AGCO

- 12.2 Bogballe

- 12.3 Bredal

- 12.4 Claas

- 12.5 CNH Industrial

- 12.6 Dalton

- 12.7 Fertilizer Equipment Specialists

- 12.8 IRIS Spreaders

- 12.9 John Deere

- 12.10 Kasco Manufacturing

- 12.11 Kubota

- 12.12 Kuhn

- 12.13 Kverneland

- 12.14 Mahindra & Mahindra

- 12.15 Maschio Gaspardo

- 12.16 Monosem

- 12.17 Rauch Landmaschinenfabrik

- 12.18 Sulky Burel

- 12.19 Techint

- 12.20 Vicon

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 175 Pages

- 納期

- 2~3営業日