|

市場調査レポート

商品コード

1665342

モジュール式包装機器の市場機会、成長促進要因、産業動向分析、2025年~2034年予測Modular Packaging Equipment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| モジュール式包装機器の市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2024年12月23日

発行: Global Market Insights Inc.

ページ情報: 英文 220 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

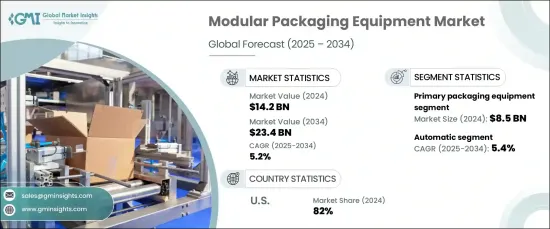

モジュール式包装機器の世界市場は2024年に142億米ドルに達し、2025~2034年にかけてCAGR 5.2%で力強い成長が見込まれています。

この拡大の主要原動力は、eコマースや消費者直接販売(DTC)ビジネスモデルへのシフトが進んでいることです。オンラインプラットフォームを採用する企業が増えるにつれ、柔軟で拡大性のある包装ソリューションに対するニーズが急増しています。モジュール式包装システムはこの需要に応え、さまざまな製品サイズ、個別包装のニーズ、最適化された出荷形態など、今日のめまぐるしいビジネス環境に欠かせない適応性の高いソリューションを提供するようになっています。

市場は一次包装機器と二次包装機器タイプに分けられます。一次包装機器セグメントは2024年に85億米ドルを生み出し、2034年までCAGR 5.3%で成長すると予測されています。革新的でカスタマイズ型包装ソリューションに対する需要の高まりが、このセグメントの成長を後押ししています。メーカー各社は、多様な製品形態や進化し続ける消費者の嗜好に対応するため、軟質な一次包装システムの採用を増やしています。これらのシステムは、強化された効率性、適応性、市場のダイナミックな需要に対応する能力を記載しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025~2034年 |

| 開始金額 | 142億米ドル |

| 予測金額 | 234億米ドル |

| CAGR | 5.2% |

自動化の観点から、市場は手動、半自動、自動システムに区分されます。自動包装機器セグメントは2024年に市場シェアの45%を占め、予測期間を通じてCAGR 5.4%で成長すると予測されています。医薬品、飲食品、民生用電子機器製品など大量生産を行う産業では、自動モジュールシステムの採用が急速に進んでいます。これらのシステムは、効率的な製造に必要な精度と一貫性を維持しながら、迅速な処理を可能にし、手作業の必要性を減らし、大規模なオペレーションをサポートします。

米国のモジュール式包装機器市場は、2024年には82%の圧倒的シェアを占めています。この地域ではeコマースの急速な拡大により、幅広い製品タイプと多様な出荷要件に対応できる汎用性の高い包装システムへのニーズがさらに高まっています。より速く、より安全で、費用対効果の高い包装ソリューションに対する消費者の要求の高まりが、モジュール式包装システムの成長を後押ししています。これらのシステムは生産プロセスを合理化するだけでなく、材料使用量を最適化し、産業全体で持続可能で効率的な包装プラクティスを促進しています。

目次

第1章 調査手法と調査範囲

- 市場範囲と定義

- 基本推定と計算

- 予測計算

- データソース

- 一次データ

- 二次データ

- 有料情報源

- 公的情報源

第2章 エグゼクティブサマリー

第3章 産業洞察

- エコシステム分析

- バリューチェーンに影響を与える要因。

- 利益率分析

- 変革

- 将来の展望

- メーカー

- 流通業者

- サプライヤーの状況

- 利益率分析

- 主要ニュース&イニシアチブ

- 規制状況

- 影響要因

- 促進要因

- 成長するeコマース産業

- 飲食品産業の成長

- 産業の潜在的リスク・課題

- 市場の飽和と激しい競合

- 持続可能性への懸念

- 促進要因

- 技術概要

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 競合のポジショニングマトリックス

- 戦略展望マトリックス

第5章 市場推定・予測:タイプ別、2021~2034年

- 主要動向

- 一次包装機器

- 充填機

- シール機

- ラベル貼り機

- コーディング&マーキング機器

- 二次包装機器

- カートニングマシン

- ケースパッキングシステム

- シュリンク包装機

- パレタイジング機器

第6章 市場推定・予測:自動化レベル別、2021~2034年

- 主要動向

- 手動システム

- 半自動システム

- 自動システム

第7章 市場推定・予測:最終用途別、2021~2034年

- 主要動向

- 飲食品

- 医薬品

- 化粧品・パーソナルケア

- 化学・農薬

- エレクトロニクス

- その他(自動車など)

第8章 市場推定・予測:流通チャネル別、2021~2034年

- 主要動向

- 直接

- 間接

第9章 市場推定・予測:地域別、2021~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- ラテンアメリカ

- ブラジル

- メキシコ

- 中東・アフリカ

- アラブ首長国連邦

- サウジアラビア

- 南アフリカ

第10章 企業プロファイル

- Bosch Packaging Technology

- Coesia

- Combi Packaging Systems

- IMA Group

- Krones

- Marchesini Group

- Marel

- Multivac

- NJM Packaging

- Packaging Automation

- ProMach

- Rockwell Automation

- Sidel Group

- Tetra Pak

- Unipak Machinery

The Global Modular Packaging Equipment Market reached USD 14.2 billion in 2024 and is expected to experience robust growth at a CAGR of 5.2% from 2025 to 2034. A major driver behind this expansion is the increasing shift toward e-commerce and direct-to-consumer (DTC) business models. As more businesses embrace online platforms, the need for flexible, scalable packaging solutions has surged. Modular packaging systems are stepping up to meet this demand, providing adaptable solutions for varying product sizes, personalized packaging needs, and optimized shipping configurations, which are crucial in today's fast-paced business environment.

The market is divided into primary and secondary packaging equipment types. The primary packaging equipment segment generated USD 8.5 billion in 2024 and is anticipated to grow at a CAGR of 5.3% through 2034. The rising demand for innovative and customized packaging solutions is fueling the growth of this segment. Manufacturers are increasingly adopting flexible primary packaging systems to accommodate diverse product formats and ever-evolving consumer preferences. These systems offer enhanced efficiency, adaptability, and the ability to meet the dynamic demands of the market.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $14.2 Billion |

| Forecast Value | $23.4 Billion |

| CAGR | 5.2% |

In terms of automation, the market is segmented into manual, semi-automatic, and automatic systems. The automatic packaging equipment segment accounted for 45% of the market share in 2024 and is projected to grow at a CAGR of 5.4% throughout the forecast period. Industries with high-volume production, such as pharmaceuticals, food and beverages, and consumer electronics, are rapidly adopting automated modular systems. These systems enable faster processing, reduce the need for manual intervention, and support large-scale operations, all while maintaining the precision and consistency required for efficient manufacturing.

The U.S. modular packaging equipment market held a dominant share of 82% in 2024. The rapid expansion of e-commerce in the region has further amplified the need for versatile packaging systems that can handle a wide range of product types and diverse shipping requirements. Increasing consumer demands for faster, more secure, and cost-effective packaging solutions have propelled the growth of modular packaging systems. These systems not only streamline production processes but also optimize material usage, promoting sustainable and efficient packaging practices across industries.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations.

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain.

- 3.1.2 Profit margin analysis.

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Supplier landscape

- 3.3 Profit margin analysis.

- 3.4 Key news & initiatives

- 3.5 Regulatory landscape

- 3.6 Impact forces

- 3.6.1 Growth drivers

- 3.6.1.1 Growing e-commerce industry

- 3.6.1.2 Growing food and beverage industry

- 3.6.2 Industry pitfalls & challenges

- 3.6.2.1 Market saturation and intense competition

- 3.6.2.2 Sustainability concerns

- 3.6.1 Growth drivers

- 3.7 Technological overview

- 3.8 Growth potential analysis

- 3.9 Porter’s analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Type, 2021-2034 (USD Million) (Thousand Units)

- 5.1 Key trends

- 5.2 Primary packaging equipment

- 5.2.1 Filling machines

- 5.2.2 Sealing machines

- 5.2.3 Labeling machines

- 5.2.4 Coding and marking equipment

- 5.3 Secondary packaging equipment

- 5.3.1 Cartoning machines

- 5.3.2 Case packing systems

- 5.3.3 Shrink wrapping machines

- 5.3.4 Palletizing equipment

Chapter 6 Market Estimates & Forecast, By Automation Level, 2021-2034 (USD Million) (Thousand Units)

- 6.1 Key trends

- 6.2 Manual modular equipment

- 6.3 Semi-automatic systems

- 6.4 Automatic systems

Chapter 7 Market Estimates & Forecast, By End Use, 2021-2034 (USD Million) (Thousand Units)

- 7.1 Key trends

- 7.2 Food and beverage

- 7.3 Pharmaceuticals

- 7.4 Cosmetics and personal care

- 7.5 Chemical and agrochemical

- 7.6 Electronics

- 7.7 Others (automotive, etc.)

Chapter 8 Market Estimates & Forecast, By Distribution Channel, 2021-2034 (USD Million) (Thousand Units)

- 8.1 Key trends

- 8.2 Direct

- 8.3 Indirect

Chapter 9 Market Estimates & Forecast, By Region, 2021-2034 (USD Million) (Thousand Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 Australia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 Saudi Arabia

- 9.6.3 South Africa

Chapter 10 Company Profiles

- 10.1 Bosch Packaging Technology

- 10.2 Coesia

- 10.3 Combi Packaging Systems

- 10.4 IMA Group

- 10.5 Krones

- 10.6 Marchesini Group

- 10.7 Marel

- 10.8 Multivac

- 10.9 NJM Packaging

- 10.10 Packaging Automation

- 10.11 ProMach

- 10.12 Rockwell Automation

- 10.13 Sidel Group

- 10.14 Tetra Pak

- 10.15 Unipak Machinery