|

市場調査レポート

商品コード

1665335

自動車用熱電発電機の市場機会、成長促進要因、産業動向分析、2025~2034年予測Automotive Thermoelectric Generator Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 自動車用熱電発電機の市場機会、成長促進要因、産業動向分析、2025~2034年予測 |

|

出版日: 2024年12月23日

発行: Global Market Insights Inc.

ページ情報: 英文 240 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

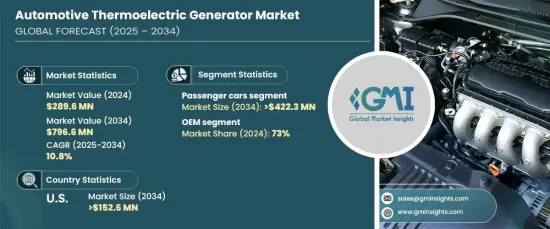

自動車用熱電発電機の世界市場は、2024年には2億8,960万米ドルとなり、2025~2034年のCAGRは10.8%と予測され、力強い成長を遂げる見込みです。

この成長の原動力は、燃料コストの上昇と、自動車の排出ガス削減を目的とした政府規制の厳格化です。その結果、燃料効率を高め、環境への影響を最小限に抑える技術に対する需要が急増しています。

この市場拡大の大きな要因は、電気自動車やハイブリッド車の人気が高まっていることです。これらの先進自動車は、バッテリー性能と走行距離を最適化するエネルギー管理システムに依存しています。排気システムからの廃熱を使用可能な電気に変換するATEGは、この最適化において極めて重要な役割を果たしています。補助システムに電力を供給し、バッテリー充電をサポートすることで、これらの発電機は最新の自動車のエネルギー効率向上に貢献しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025~2034年 |

| 開始金額 | 2億8,960万米ドル |

| 予測金額 | 7億9,660万米ドル |

| CAGR | 10.8% |

車種別では、乗用車、商用車、ハイブリッド車・電気自動車に区分されます。乗用車は2024年に市場をリードし、市場シェアの57%を占めています。このセグメントは、乗用車の大量生産と低燃費技術への需要の高まりに後押しされ、2034年までに4億2,230万米ドルを生み出すと予測されています。乗用車にATEGが広く採用されることで、エネルギー回収システムの技術革新と統合に大きな機会が生まれ、このセグメントの継続的成長が確実なものとなります。

市場はさらに、流通チャネルに基づいて相手先商標製品メーカー(OEM)とアフターマーケットに分類されます。2024年には、OEMが73%のシェアを占め、この傾向は予測期間を通じて続くと予想されます。OEMは、製造プロセスでATEGをシームレスに自動車に組み込み、互換性と最適化された性能を確保することに優れています。自動車メーカーからの大量注文に対応することで、OEMはこれらの技術の採用を加速させながらコスト効率を達成しています。さらに、OEMの技術的専門知識により、特定の車両アーキテクチャに合わせたシステム設計が可能になり、全体的な効率と信頼性が向上します。

米国では、自動車用熱電発電機市場は2024年に86%のシェアを獲得し、2034年には1億5,260万米ドルに達すると予測されています。企業平均燃費(CAFE)基準を含む厳しい燃料効率と排出規制が、この需要の主要促進要因となっています。米国市場はまた、先進的な省燃費システムを搭載するようになっているプレミアム車や高級車に対する高い需要からも恩恵を受けています。さらに、研究開発への多額の投資と大手ATEGメーカーの存在が技術革新を促進し、市場の成長軌道を支えています。

報告書の内容

第1章 調査手法と調査範囲

- 調査デザイン

- 調査アプローチ

- データ収集方法

- 基本推定と計算

- 基準年の算出

- 市場推定の主要動向

- 予測モデル

- 一次調査と検証

- 一次情報

- データマイニングソース

- 市場定義

第2章 エグゼクティブサマリー

第3章 産業洞察

- エコシステム分析

- 技術プロバイダー

- 部品サプライヤー

- メーカー

- OEMメーカー

- サプライヤーの状況

- 利益率分析

- 技術革新の状況

- 主要ニュース&イニシアチブ

- 規制状況

- 影響要因

- 促進要因

- 燃料効率に対する需要の高まり

- 厳しい排ガス規制

- 電気自動車とハイブリッド車の採用拡大

- 熱電材料の技術進歩

- 産業の潜在的リスク・課題

- 技術の初期コストが高い

- 消費者の認知度の低さ

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 競合のポジショニングマトリックス

- 戦略展望マトリックス

第5章 市場推定・予測:材料別、2021~2034年

- 主要動向

- テルル化ビスマス

- テルル化鉛

- シリコンゲルマニウム

- その他

第6章 市場推定・予測:車両別、2021~2034年

- 主要動向

- 乗用車

- 商用車

- ハイブリッド車・電気自動車

第7章 市場推定・予測:技術別、2021~2034年

- 主要動向

- 廃熱回収

- 発電

- バッテリー管理

第8章 市場推定・予測:流通チャネル別、2021~2034年

- 主要動向

- OEM

- アフターマーケット

第9章 市場推定・予測:地域別、2021~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- スペイン

- イタリア

- ロシア

- 北欧

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- ニュージーランド

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- アラブ首長国連邦

- 南アフリカ

- サウジアラビア

第10章 企業プロファイル

- Alphabet Energy

- European Thermodynamics

- Faurecia

- Ferrotec Holdings Corporation

- Gentherm Incorporated

- Hi-Z Technology, Inc.

- II-VI Marlow

- KELK Ltd.

- Komatsu Ltd.

- Laird Thermal Systems

- SANGO Co., Ltd.

- Tenneco Inc.

- Thermonamic Electronics(Jiangxi)Corp., Ltd.

- Valeo

- Yamaha Motor Co., Ltd.

The Global Automotive Thermoelectric Generator Market, valued at USD 289.6 million in 2024, is set to experience robust growth, projected at a CAGR of 10.8% from 2025 to 2034. This growth is driven by the rising costs of fuel and increasingly stringent government regulations aimed at reducing vehicle emissions. As a result, the demand for technologies that enhance fuel efficiency and minimize environmental impact is surging.

A significant driver of this market expansion is the growing popularity of electric and hybrid vehicles. These advanced vehicles rely on energy management systems to optimize battery performance and driving range. ATEGs, which convert waste heat from exhaust systems into usable electricity, play a pivotal role in this optimization. By powering auxiliary systems and supporting battery charging, these generators contribute to enhanced energy efficiency in modern vehicles.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $289.6 Million |

| Forecast Value | $796.6 Million |

| CAGR | 10.8% |

In terms of vehicle type, the market is segmented into passenger cars, commercial vehicles, and hybrid and electric vehicles. Passenger cars led the market in 2024, commanding 57% of the market share. This segment is forecasted to generate USD 422.3 million by 2034, fueled by the mass production of passenger vehicles and the increasing demand for fuel-efficient technologies. The widespread adoption of ATEGs in passenger cars creates substantial opportunities for innovation and integration of energy recovery systems, ensuring continuous growth in this segment.

The market is further categorized based on sales channels into original equipment manufacturers (OEMs) and aftermarket. In 2024, OEMs dominated with a 73% share, a trend expected to persist throughout the forecast period. OEMs excel in seamlessly incorporating ATEGs into vehicles during the manufacturing process, ensuring compatibility and optimized performance. By fulfilling bulk orders for automakers, OEMs achieve cost efficiencies while accelerating the adoption of these technologies. Additionally, their technical expertise enables them to design systems tailored to specific vehicle architectures, enhancing overall efficiency and reliability.

In the United States, the automotive thermoelectric generator market held an impressive 86% share in 2024 and is projected to reach USD 152.6 million by 2034. Stringent fuel efficiency and emissions regulations, including the Corporate Average Fuel Economy (CAFE) standards, are key drivers of this demand. The U.S. market also benefits from a high demand for premium and luxury vehicles, which increasingly incorporate advanced fuel-saving systems. Furthermore, significant investments in research and development, coupled with the presence of leading ATEG manufacturers, foster innovation and support the market's growth trajectory.

Report Content

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Technology providers

- 3.1.2 Component suppliers

- 3.1.3 Manufacturers

- 3.1.4 OEMs

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Technology & innovation landscape

- 3.5 Key news & initiatives

- 3.6 Regulatory landscape

- 3.7 Impact forces

- 3.7.1 Growth drivers

- 3.7.1.1 Increasing demand for fuel efficiency

- 3.7.1.2 Stringent emission regulations

- 3.7.1.3 Growing adoption of electric and hybrid vehicles

- 3.7.1.4 Technological advancements in thermoelectric materials

- 3.7.2 Industry pitfalls & challenges

- 3.7.2.1 High initial cost of technology

- 3.7.2.2 Limited awareness among consumers

- 3.7.1 Growth drivers

- 3.8 Growth potential analysis

- 3.9 Porter’s analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Material, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 Bismuth telluride

- 5.3 Lead telluride

- 5.4 Silicon germanium

- 5.5 Others

Chapter 6 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 Passenger cars

- 6.3 Commercial vehicles

- 6.4 Hybrid and electric vehicles

Chapter 7 Market Estimates & Forecast, By Technology, 2021 - 2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 Waste heat recovery

- 7.3 Power generation

- 7.4 Battery management

Chapter 8 Market Estimates & Forecast, By Sales Channel, 2021 - 2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 OEM

- 8.3 Aftermarket

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Russia

- 9.3.7 Nordics

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 ANZ

- 9.4.6 Southeast Asia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 South Africa

- 9.6.3 Saudi Arabia

Chapter 10 Company Profiles

- 10.1 Alphabet Energy

- 10.2 European Thermodynamics

- 10.3 Faurecia

- 10.4 Ferrotec Holdings Corporation

- 10.5 Gentherm Incorporated

- 10.6 Hi-Z Technology, Inc.

- 10.7 II-VI Marlow

- 10.8 KELK Ltd.

- 10.9 Komatsu Ltd.

- 10.10 Laird Thermal Systems

- 10.11 SANGO Co., Ltd.

- 10.12 Tenneco Inc.

- 10.13 Thermonamic Electronics (Jiangxi) Corp., Ltd.

- 10.14 Valeo

- 10.15 Yamaha Motor Co., Ltd.