|

市場調査レポート

商品コード

1665287

宇宙ラストワンマイルデリバリー市場の市場機会、成長促進要因、産業動向分析、2025年~2034年予測Space Last-Mile Delivery Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 宇宙ラストワンマイルデリバリー市場の市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2024年12月19日

発行: Global Market Insights Inc.

ページ情報: 英文 220 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

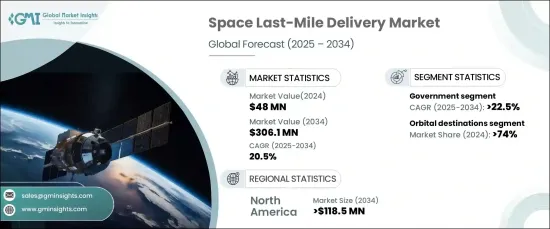

世界の宇宙ラストマイルデリバリー市場は、2024年には4,800万米ドルと評価され、2025~2034年のCAGRは20.5%と予測され、目覚ましい成長を遂げます。

この成長の原動力となっているのは、最先端の軌道上ロジスティクスソリューションと精密な衛星配備に対する需要の高まりです。軌道上輸送機と先進推進システムの革新は、より効率的なペイロードの配置と再配置を可能にし、衛星ネットワーク、宇宙探査、商業運用をこれまで以上に効果的にします。宇宙の商業化が進み、再利用可能な技術が進歩したことで、こうしたサービスはより費用対効果が高くなり、より幅広い産業が利用できるようになっています。

宇宙ラストマイルデリバリー市場は、主に軌道上の目的地と惑星または地表の目的地の2つのカテゴリーに分けられます。軌道目的地セグメントは、2024年には74%の圧倒的な市場シェアを占めており、今後数年間は力強い成長が見込まれます。世界のブロードバンドカバレッジ、地球観測、通信サービスのための衛星コンステレーションの展開拡大が、軌道デリバリーソリューションの需要を大幅に押し上げています。各組織は、衛星の性能を最適化するために正確な軌道配置を達成することに重点を置いており、宇宙ミッションの進化するニーズを満たすために、ラストマイルデリバリーシステムや軌道変換技術への依存を高めています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025~2034 |

| 開始金額 | 4,800万米ドル |

| 予測金額 | 3億610万米ドル |

| CAGR | 20.5% |

エンドユーザーの観点から、市場は商業部門と政府部門に区分されます。2034年のCAGRは22.5%と予測され、政府部門が最も高い成長が見込まれています。世界各国の政府は、モニタリング、通信、ミサイル探知に重要な防衛衛星を配備するため、ラストマイルデリバリーインフラへの投資を強化しています。正確な軌道測位の必要性から、軌道上輸送機や軌道上サービス機能への関心が高まっており、その結果、国家安全保障が強化され、衛星ネットワークの効率が最適化されます。

北米は宇宙ラストマイルデリバリー市場をリードし、2034年までに1億1,850万米ドルに達すると予想されています。米国は、宇宙探査と商業化における技術的専門知識によって、この成長の最前線にいます。地球観測と通信のための衛星コンステレーションの配備が加速しているため、先進的軌道上ロジスティクスシステムの需要がさらに高まっています。各社は、ミッションの柔軟性を高め、コストを削減し、宇宙運用をより効率的で手頃なものにする、再利用可能な輸送機や自律的輸送技術の開発に注力しています。

目次

第1章 調査手法と調査範囲

- 市場範囲と定義

- 基本推定と計算

- 予測計算

- データソース

- 1次データ

- 二次資料

- 有料情報源

- 公的情報源

第2章 エグゼクティブサマリー

第3章 産業洞察

- エコシステム分析

- バリューチェーンに影響を与える要因

- 利益率分析

- 変革

- 将来の展望

- メーカー

- 流通業者

- サプライヤーの状況

- 利益率分析

- 主要ニュース

- 規制状況

- 影響要因

- 促進要因

- 衛星配備数の増加

- 商業宇宙ベンチャーの台頭と宇宙開発への民間セクターの関与の拡大

- ライドシェアリングと二次ペイロード打ち上げの増加

- 持続可能性とスペースデブリの軽減への関心の高まり

- 政府投資と宇宙開発計画の増加

- 産業の潜在的リスク・課題

- 高い開発・運用コスト

- 技術的限界と信頼性

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 競合のポジショニングマトリックス

- 戦略的展望マトリックス

第5章 市場推定・予測:仕向地別、2021~2034年

- 主要動向

- 軌道目的地

- 低軌道(LEO)

- 中軌道(MEO)

- 静止軌道(GEO)

- 地球高周回軌道(GEO以遠)

- 惑星/地表の目的地

- 月面

- 火星表面

- 小惑星表面

第6章 市場推定・予測:2021~2034年、ペイロード別

- 主要動向

- 科学機器

- インフラコンポーネント

- 宇宙ステーションモジュール

- 衛星部品

- 消耗品

- 推進剤・燃料

- その他

第7章 市場推定・予測:デリバリー技術別、2021~2034年

- 主要動向

- 自律システム

- 有人デリバリー

- ハイブリッドシステム

第8章 市場推定・予測:最終用途別、2021~2034年

- 主要動向

- 商業

- 政府

第9章 市場推定・予測:地域別、2021~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- ラテンアメリカ

- ブラジル

- メキシコ

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第10章 企業プロファイル

- AAC Clyde Space

- Aliena

- Astro Digital

- D-Orbit

- Exotrail

- Impulse Space

- Momentus Space

- Orbit Fab

- Rocket Lab

- SEOPS(Space Exploration and Orbital Solutions)

- Spaceflight Industries

- SpaceLink

- TransAstra

The Global Space Last-Mile Delivery Market was valued at USD 48 million in 2024 and is set to experience impressive growth, with a projected compound annual growth rate (CAGR) of 20.5% from 2025 to 2034. This growth is being driven by an increasing demand for cutting-edge in-orbit logistics solutions and precise satellite deployment. Innovations in orbital transfer vehicles and advanced propulsion systems enable more efficient payload placement and repositioning, making satellite networks, space exploration, and commercial operations more effective than ever. With the growing commercialization of space and advancements in reusable technologies, these services are becoming more cost-effective and accessible to a broader range of industries.

The space last-mile delivery market is primarily divided into two categories: orbital targets and planetary or surface destinations. The orbital destinations segment held a dominant 74% market share in 2024 and is expected to see robust growth in the coming years. The expanding deployment of satellite constellations for global broadband coverage, Earth observation, and communication services is significantly boosting the demand for orbital delivery solutions. Organizations are placing greater emphasis on achieving precise orbital placement to optimize satellite performance, driving increased reliance on last-mile delivery systems and orbital transfer technologies to meet the evolving needs of space missions.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $48 million |

| Forecast Value | $306.1 million |

| CAGR | 20.5% |

In terms of end users, the market is segmented into commercial and government sectors. The government segment is expected to experience the highest growth, with a projected CAGR of 22.5% through 2034. Governments worldwide are ramping up investments in last-mile delivery infrastructure to deploy critical defense satellites for surveillance, communications, and missile detection. The need for exact orbital positioning is fueling greater interest in orbital transfer vehicles and in-orbit servicing capabilities, which in turn enhances national security and optimizes satellite network efficiency.

North America is anticipated to lead the space last-mile delivery market, reaching USD 118.5 million by 2034. The United States is at the forefront of this growth, driven by its technological expertise in space exploration and commercialization. The escalating deployment of satellite constellations for Earth observation and communication is further intensifying the demand for advanced in-orbit logistics systems. Companies are focusing on developing reusable transfer vehicles and autonomous delivery technologies, which enhance mission flexibility and reduce costs, making space operations more efficient and affordable.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Key news & initiatives

- 3.5 Regulatory landscape

- 3.6 Impact forces

- 3.6.1 Growth drivers

- 3.6.1.1 Growing number of satellite deployment

- 3.6.1.2 Rise of commercial space ventures and the growing private sector involvement in space exploration

- 3.6.1.3 Increasing ride-sharing and secondary payload launches

- 3.6.1.4 Growing focus on sustainability and mitigating space debris

- 3.6.1.5 Increasing governmental investments and space programs

- 3.6.2 Industry pitfalls & challenges

- 3.6.2.1 High development and operational costs

- 3.6.2.2 Technological limitations and reliability

- 3.6.1 Growth drivers

- 3.7 Growth potential analysis

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Destination, 2021-2034 (USD Million)

- 5.1 Key trends

- 5.2 Orbital destinations

- 5.2.1 Low earth orbit (LEO)

- 5.2.2 Medium earth orbit (MEO)

- 5.2.3 Geostationary orbit (GEO)

- 5.2.4 High earth orbit (Beyond GEO)

- 5.3 Planetary/surface destinations

- 5.3.1 Lunar surface

- 5.3.2 Martian surface

- 5.3.3 Asteroids surface

Chapter 6 Market Estimates & Forecast, By Delivery Payload, 2021-2034 (USD Million)

- 6.1 Key trends

- 6.2 Scientific equipment

- 6.3 Infrastructure components

- 6.3.1 Space station modules

- 6.3.2 Satellite components

- 6.4 Consumables

- 6.5 Propellants/fuel

- 6.6 Others

Chapter 7 Market Estimates & Forecast, By Delivery Technology, 2021-2034 (USD Million)

- 7.1 Key trends

- 7.2 Autonomous systems

- 7.3 Manned delivery

- 7.4 Hybrid systems

Chapter 8 Market Estimates & Forecast, By End Use, 2021-2034 (USD Million)

- 8.1 Key trends

- 8.2 Commercial

- 8.3 Government

Chapter 9 Market Estimates & Forecast, By Region, 2021-2034 (USD Million)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 Australia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 AAC Clyde Space

- 10.2 Aliena

- 10.3 Astro Digital

- 10.4 D-Orbit

- 10.5 Exotrail

- 10.6 Impulse Space

- 10.7 Momentus Space

- 10.8 Orbit Fab

- 10.9 Rocket Lab

- 10.10 SEOPS (Space Exploration and Orbital Solutions)

- 10.11 Spaceflight Industries

- 10.12 SpaceLink

- 10.13 TransAstra