|

市場調査レポート

商品コード

1644901

ドイツのラストマイル配送:市場シェア分析、産業動向と統計、成長予測(2025年~2030年)Germany Last Mile Delivery - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| ドイツのラストマイル配送:市場シェア分析、産業動向と統計、成長予測(2025年~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 150 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

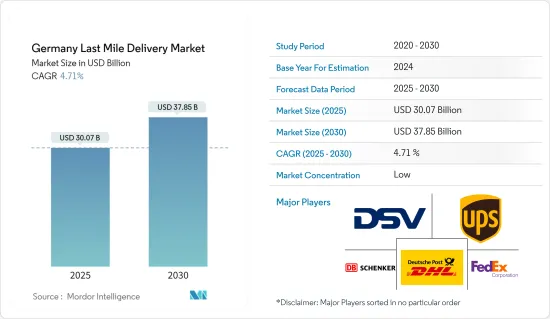

ドイツのラストマイル配送の市場規模は2025年に300億7,000万米ドルと推定され、予測期間中(2025~2030年)のCAGRは4.71%で、2030年には378億5,000万米ドルに達すると予測されます。

マイル配送市場は、eコマース分野の開拓や世界化による取引活動の活発化、配送車両の技術革新、迅速な荷物配送のニーズなど、いくつかの要因によって牽引されています。

しかし、貧弱なインフラ、高い物流コスト、メーカーや小売業者による物流サービスの管理不足、不正確な郵便住所システムなどが市場の成長を阻害します。ドイツで社会活動や不要不急の商業活動を制限する指令が施行されて以来、鉄道や道路による貨物輸送は約20%減少しました。

オンライン小売業者の大半もCOVID-19の影響を受けました。ドイツポストによると、通常、1日平均520万個の小包が配達されています。ドイツポストによると、封鎖期間中、毎日800万個以上の小包や配達物が輸送されたといいます。コロナウイルス危機により、国内の保管スペースの需要が高まっているが、これは予想外ではないです。

ドイツでは、世界のほぼすべての国と同様、eコマースがかつてない成長を遂げています。eコマースの成長と並行して、小包ロッカーや小包集積所といった全国的な宅配オプションの人気が高まっています。例えば、ドイツポストは現在約8,500台の自動小包機を運用しており、2023年までに1万2,500台まで増やす計画です。

例えば、2023年6月には、即日配達サービスを提供するDODOがドイツ市場に事業を拡大し、即日配達、ラストマイル配送の長期的な実現可能性が強化されました。DODOは長年にわたり、さまざまな業界のプレイヤーをサポートする包括的なソフトウェアとデリバリーのエコシステムを開発してきました。このエコシステムは、企業のIT構造に直接統合できる同社のホワイトラベル・ソリューションによってさらにサポートされています。DODOは現在、2500人以上の宅配業者と1,000台以上の車両を雇用しています。

ドイツのラストマイル配送市場動向

eコマースの成長が市場を牽引

ドイツのeコマース・プラットフォーム市場は、主に同地域のインターネット普及率の高さと、スマートデバイスの利用拡大が牽引しています。都市化の進展に伴い、多くの伝統的企業が顧客数と市場シェアを拡大し、諸経費を削減し、製品の売上を伸ばすためにeコマース・プラットフォームを利用するようになっています。

ドイツでは、大半のオンライン・ストアが支払い方法としてペイパルかクレジットカードを受け入れています。また、銀行振込に対応しているウェブサイトも多いです。また、ほとんどのサイトでは、請求書/今すぐ買って後払いでの支払いが可能であり、オンラインの顧客は14日以内であれば、理由を問わず、あるいはまったく理由をつけずに注文をキャンセルし、商品やサービスを返品することができます。eコマース企業が提供するメリットは非常に多く、この地域のeコマース産業は今後数年間で拡大し続けると思われます。

ドイツのeコマース売上で最も多いのはファッション(24.1%)で、次いで食品・パーソナルケア(22.2%)、家具・家電(20.2%)、電子機器・メディア(17.4%)、玩具・趣味・DIY(16.0%)となっています。

交通インフラへの政府投資がラストマイル配送を支える

ラストマイル配送は、交通網を改善し、混雑を緩和し、物流効率を向上させるインフラに投資することで改善できます。道路、橋、港湾が整備されれば、より迅速かつ効率的に商品を輸送できるようになり、結果として配送時間が短縮されます。スマート交通管理システム(TMS)や配送専用レーンは、混雑を緩和し、タイムリーな配送を実現するのに役立ちます。リアルタイムのモニタリングをサポートするデジタル・インフラは、ルートを最適化し、配送チームと顧客とのコミュニケーションを向上させる。

ドイツ連邦政府は2022年、2021年と比べて数百万ユーロ増の交通インフラ支出を割り当てる予定です。輸送インフラ支出の最大の増加は、連邦鉄道に110億ユーロ(120億1,000万米ドル)が割り当てられた2021年に発生し、これは2016年に割り当てられた額の2倍以上です。2022年には連邦高速道路に120億ユーロ以上、水路に170億ユーロ(180億1,000万米ドル)が割り当てられます。

B247の拡張は北部テューリンゲン州最大のインフラプロジェクトとなった。このプロジェクトは、22.2kmの道路区間に2~4車線を新設するもので、2つの新しいバイパス、2つの橋と5つの鉄道橋を含む31の構造物、8つのジャンクション、約6kmの州道と連邦道の追加などが含まれます。工事は2025年半ばまでに、ドイツのVINCIグループの子会社(Eurovia、VINCI Construction Terrassement、Via Structure)がチューリンゲン州の企業と現地で提携して完成させる。

ドイツのラストマイル配送業界の概要

ドイツのラストマイル配送市場は、国際的なプレーヤーと国内プレーヤーが混在しているため、競争が激しいです。ドイツのラストマイル配送市場の大手企業には、DSV(ディレクトール・フォン・シュヴェリン)、UPS(ユナイテッド・パーセル・サービス)(UPS)、DBシュヴェリン(ドイツポストDHL)、フェデックス(FedEx)などがあります。この分野の企業は、ドローン、電子車両、輸送管理システム(TMS)、人工知能(AI)などの新技術の統合による成長に注力しています。ドイツのロジスティクス企業は、人件費が上昇し、労働力の確保が難しくなっているため、苦戦を強いられています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 現在の市場シナリオ

- 技術動向

- eコマース業界に関する洞察

- トラック輸送業界に関する洞察

- 倉庫・配送センターに関する洞察

- 冷蔵ラストマイル配送への洞察

- 返品物流への洞察

- COVID-19の市場への影響

第5章 市場力学

- 市場促進要因

- 電子商取引の増加

- 都市化の進展

- 市場抑制要因/課題

- 荷物の盗難や破損のリスク

- コスト効率

- 市場機会

- eコマースの統合

- 業界の魅力- ポーターのファイブフォース分析

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第6章 市場セグメンテーション

- サービス別

- B2B(Business-to-Business)

- B2C(Business-to-Consumer)

- C2C(Customer-to-Customer)

第7章 競合情勢

- 市場集中度の概要

- 企業プロファイル

- DSV

- UPS

- DB Schenker

- Deutsche Post DHL

- FedEx

- DPD Group

- General Logistics Systems

- Rhenes Logistics

- JJX Logistics

- CEVA Logistics

- SpeedLink Transport*

第8章 市場機会と今後の動向

第9章 付録

The Germany Last Mile Delivery Market size is estimated at USD 30.07 billion in 2025, and is expected to reach USD 37.85 billion by 2030, at a CAGR of 4.71% during the forecast period (2025-2030).

The mile delivery market is driven by several factors, including the development of the e-commerce sector and the rise in trading activities due to globalization, technological innovations in delivery vehicles, and the need for fast package delivery.

However, poor infrastructure, high logistics costs, a lack of control over logistics services by manufacturers and retailers, and an inaccurate postal address system will impede the market growth. Since the implementation of the directive to restrict social activities and non-essential commercial activities in Germany, freight transport by rail and road has decreased by approximately 20%.

The majority of online retailers were also affected by COVID-19. According to Deutsche Post, a daily average of 5.2 million parcels are usually delivered. Deutsche Post reported that during the lockdowns, more than 8 million packages and deliveries were transported daily. The coronavirus crisis has led to an increase in the demand for storage space in the country, which is not unexpected.

Germany has seen unprecedented growth in e-commerce, as has almost every country in the world. In parallel with the growth of e-commerce, nationwide out-of-the-home delivery options such as parcel lockers and parcel collection stations have become increasingly popular. Deutsche Post, for example, currently operates about 8500 automated parcel machines, with plans to increase that to 12,500 machines by 2023.

For instance, in June 2023, DODO, the same-day delivery service provider, expanded its operations into the German market, reinforcing the long-term viability of same-day, last-mile delivery. DODO has developed a comprehensive software and delivery ecosystem over the years to support players across a variety of industries. This ecosystem is further supported by the company's white-label solution, which allows direct integration into the company's IT structure. DODO currently employs more than 2500 couriers and 1,000 vehicles.

Germany Last Mile Delivery Market Trends

Growth in E-commerce is Driving the Market

The e-commerce platform market in Germany is mainly driven by the high internet penetration in the region and the growing use of smart devices. With increasing urbanization, many traditional businesses are turning to e-commerce platforms to increase the number of customers and market share, reduce overhead expenses, and increase the sales of their products.

In Germany, the majority of online stores accept PayPal or credit cards as the payment method. Many websites also accept bank transfers. Most websites accept invoices/buy now and pay later, and online customers can cancel their orders within 14 days and return their goods or services for any reason or no reason at all. There are so many benefits offered by e-commerce companies that the e-commerce industry in the region will continue to expand over the next few years.

Fashion makes up the biggest chunk of German e-commerce revenue (24.1%), followed by food and personal care (22.2%), furniture and appliances (20.2%), electronics and media (17.4%), and toys, and hobby and DIY (16.0%).

Government Investment in Transport Infrastructure Supports Last Mile Delivery

Last-mile delivery can be improved by investing in infrastructure that improves transportation networks, reduces congestion, and improves logistical efficiency. Roads, bridges, and ports that are upgraded will allow goods to be transported more quickly and efficiently, resulting in shorter delivery times. Smart traffic management systems (TMS) and dedicated delivery lanes can help reduce congestion and ensure timely deliveries. The digital infrastructure that supports real-time monitoring optimizes routes and improves communication between the delivery team and customers, which can also improve last-mile delivery.

Germany's federal government plans to allocate several million euros more in transport infrastructure spending in 2022 compared to 2021. The largest increase in transport infrastructure spending occurred in 2021 when EUR 11 billion (USD 12.01 billion) was allocated to federal railways, which was more than double the amount allocated in 2016. Over EUR 12 billion will be allocated to federal highways in 2022, and EUR 17 billion (USD 18.01 billion) will be allocated to waterways.

The expansion of the B247 became the largest infrastructure project in Northern Thuringia. The project consists of building two to four new lanes on a 22.2 km road section, including two new bypasses, 31 structures, including two bridges and five railway bridges, eight junctions, and around 6 km of additional state and federal roads. The works will be completed by mid-2025 by subsidiaries of the VINCI Group in Germany (Eurovia, VINCI Construction Terrassement, and Via Structure) in local partnership with Thuringian companies.

Germany Last Mile Delivery Industry Overview

Germany's Last Mile Delivery market is highly competitive as it is made up of a mix of international and domestic players. Some of Germany's leading players in the last-mile delivery market are DSV (Direktor von Schwerin), UPS (United Parcel Service) (UPS), DB Schwerin (Deutsche Post DHL), and FedEx (FedEx). Companies in the sector are focusing on growth through the integration of new technologies such as drones, e-vehicles, transport management systems (TMS), and artificial intelligence (AI). Germany's logistics players are struggling as labor costs are on the rise and labor availability is decreasing.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definitions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Current Market Scenario

- 4.2 Technological Trends

- 4.3 Insights into E-Commerce Industry

- 4.4 Insights into Trucking Industry

- 4.5 Insights into Warehousing and Distribution Centers

- 4.6 Insights into Refrigerated Last Mile Delivery

- 4.7 Insights into Return Logistics

- 4.8 Impact of COVID-19 on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Rise In eCommerce

- 5.1.2 Rise In Urbanization

- 5.2 Market Restraints/Challenges

- 5.2.1 The Risk of Package Theft or Damage

- 5.2.2 Cost Efficiency

- 5.3 Market Opportunities

- 5.3.1 E- commerce Integration

- 5.4 Industry Attractiveness - Porter's Five Forces Analysis

- 5.4.1 Bargaining Power of Buyers/Consumers

- 5.4.2 Bargaining Power of Suppliers

- 5.4.3 Threat of New Entrants

- 5.4.4 Threat of Substitute Products

- 5.4.5 Intensity of Competitive Rivalry

6 MARKET SEGMENTATION

- 6.1 By Service

- 6.1.1 B2B (Business-to-Business)

- 6.1.2 B2C (Business-to-Consumer)

- 6.1.3 C2C (Customer-to-Customer)

7 COMPETITIVE LANDSCAPE

- 7.1 Market Concentration Overview

- 7.2 Company Profiles

- 7.2.1 DSV

- 7.2.2 UPS

- 7.2.3 DB Schenker

- 7.2.4 Deutsche Post DHL

- 7.2.5 FedEx

- 7.2.6 DPD Group

- 7.2.7 General Logistics Systems

- 7.2.8 Rhenes Logistics

- 7.2.9 JJX Logistics

- 7.2.10 CEVA Logistics

- 7.2.11 SpeedLink Transport*