|

市場調査レポート

商品コード

1665285

宇宙ロジスティクスの市場機会、成長促進要因、産業動向分析と2025~2034年予測Space Logistics Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 宇宙ロジスティクスの市場機会、成長促進要因、産業動向分析と2025~2034年予測 |

|

出版日: 2024年12月19日

発行: Global Market Insights Inc.

ページ情報: 英文 210 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

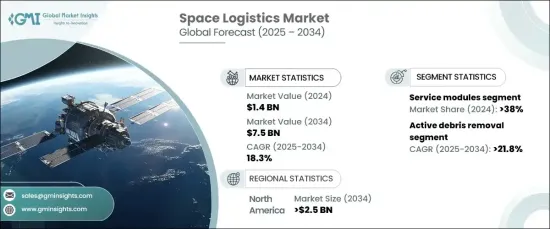

世界の宇宙ロジスティクス市場は、2024年に14億米ドルと評価され、2025~2034年のCAGRは18.3%と予測され、力強い成長を遂げます。

この成長は、衛星配備、軌道上サービス、宇宙探査プログラムに対する需要の増加が主要要因です。再使用可能な打上げ技術の革新は、通信や地球観測のための衛星コンステレーションの展開の高まりと相まって、宇宙空間における効率的な輸送と運用サポートの必要性を大幅に押し上げています。さらに、宇宙旅行や宇宙採掘などの商業ベンチャーや、月や火星を目指す政府主導の野心的なミッションの台頭が、技術の進歩を促し、新たな成長機会をもたらしています。

宇宙ロジスティクス市場は、サービスモジュール、ミッション拡大ポッド(MEP)、貨物モジュール、ロボットアームとマニピュレーター、スペースタグなど、さまざまなタイプに区分されます。2024年には、サービスモジュールが38%の市場シェアを占め、大きな成長が見込まれています。これらのモジュールは、推進、電力、通信システムなどの重要な機能を提供することで、衛星の運用を維持するために不可欠なものとなっています。衛星コンステレーションの展開が拡大する中、サービスモジュールは衛星の寿命を延ばし、軌道の持続可能性をサポートする上で重要な役割を果たしており、このセグメントでの急速な普及を後押ししています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025~2034 |

| 開始金額 | 14億米ドル |

| 予測金額 | 75億米ドル |

| CAGR | 18.3% |

同市場はまた、寿命延長、ラストマイルデリバリー、アクティブ・デブリ除去、宇宙状況認識、軌道上組立・製造などの主要セグメントを含む運用別にも区分されます。アクティブ・デブリ除去セグメントは、2034年までCAGR 21.8%という驚異的な成長が予測されています。この成長には、宇宙デブリ管理システムを強化する自律ロボット工学と人工知能(AI)技術の進歩が寄与しています。ロボットアーム、ネット、モリのような最先端のツールは、未使用の衛星やデブリを捕獲するために開発されており、AIを搭載したアルゴリズムは複雑な軌道環境でのナビゲーションと運用精度を向上させています。

北米の宇宙ロジスティクス市場は、2034年までに25億米ドルに達すると予測されています。特に米国市場は、衛星配備の需要増と宇宙インフラの進歩により大きな成長を遂げています。再使用可能な打上げロケットの採用は、運用コストの削減と打上げ頻度の増加に重要な役割を果たし、宇宙ロジスティクスの運用をより効率的で費用対効果の高いものにしています。

目次

第1章 調査手法と調査範囲

- 市場範囲と定義

- 基本推定と計算

- 予測計算

- データソース

- 1次データ

- 二次資料

- 有料情報源

- 公的情報源

第2章 エグゼクティブサマリー

第3章 産業洞察

- エコシステム分析

- バリューチェーンに影響を与える要因

- 利益率分析

- 変革

- 将来の展望

- メーカー

- 流通業者

- サプライヤーの状況

- 利益率分析

- 主要ニュース

- 規制状況

- 影響要因

- 促進要因

- 衛星打ち上げ需要の増加

- 宇宙輸送とインフラの進歩

- 再使用可能な打上げシステムと宇宙船の増加

- 宇宙での複雑なペイロード展開に対する需要の高まり

- 衛星フリート展開・管理のためのサービスとしての宇宙と柔軟なモデルへのシフト

- 産業の潜在的リスク・課題

- 宇宙事業の高コスト

- 宇宙交通管理とデブリ緩和

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 競合のポジショニングマトリックス

- 戦略展望マトリックス

第5章 市場推定・予測:タイプ別、2021~2034年

- 主要動向

- ミッション拡大ポッド(MEP)

- 貨物モジュール

- サービスモジュール

- ロボットアームとマニピュレーター

- スペースタグ

第6章 市場推定・予測:オペレーション別、2021~2034年

- 主要動向

- ラストマイルデリバリー

- 宇宙状況認識

- 寿命延長

- アクティブ・デブリ除去

- 軌道上組立・製造

第7章 市場推定・予測:軌道別、2021~2034年

- 主要動向

- 地球近傍軌道

- 地球低軌道

- 静止軌道

第8章 市場推定・予測:最終用途別、2021~2034年

- 主要動向

- 商業

- 政府・防衛

第9章 市場推定・予測:地域別、2021~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- ラテンアメリカ

- ブラジル

- メキシコ

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第10章 企業プロファイル

- Arianespace

- Astroscale

- Atomos Space

- Blue Origin

- ClearSpace

- D-Orbit

- Exolaunch

- Japan Aerospace Exploration Agency

- Lockheed Martin

- Maxar Technologies

- Northrop Grumman

- Rocket Lab

- SpaceX

- Thales Alenia Space

The Global Space Logistics Market, valued at USD 1.4 billion in 2024, is set to experience robust growth with a projected compound annual growth rate (CAGR) of 18.3% from 2025 to 2034. This growth is largely driven by the increasing demand for satellite deployment, in-orbit servicing, and space exploration programs. Innovations in reusable launch technologies, coupled with the rising deployment of satellite constellations for communication and Earth observation, have significantly boosted the need for efficient transportation and operational support in space. Furthermore, the rise of commercial ventures, such as space tourism and mining, along with ambitious government-led missions to the Moon and Mars, are catalyzing technological advancements and opening up new growth opportunities.

The space logistics market is segmented into various types, including service modules, Mission Extension Pods (MEPs), cargo modules, robotic arms and manipulators, and space tugs. In 2024, the service modules segment held a substantial 38% market share and is expected to see significant growth. These modules have become essential for maintaining satellite operations by providing critical functions such as propulsion, power, and communication systems. As the deployment of satellite constellations expands, service modules are playing a key role in extending satellite lifespans and supporting orbital sustainability, driving their rapid adoption across the sector.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.4 billion |

| Forecast Value | $7.5 billion |

| CAGR | 18.3% |

The market is also segmented by operation, with key areas including life extension, last-mile delivery, active debris removal, space situational awareness, and on-orbit assembly and manufacturing. The active debris removal segment is forecasted to grow at an impressive CAGR of 21.8% through 2034. This growth is fueled by advancements in autonomous robotics and artificial intelligence (AI) technologies, which enhance space debris management systems. Cutting-edge tools such as robotic arms, nets, and harpoons are being developed to capture unused satellites and debris, while AI-powered algorithms improve navigation and operational precision in complex orbital environments.

North America space logistics market is projected to reach USD 2.5 billion by 2034. The U.S. market, in particular, is experiencing significant growth due to the increasing demand for satellite deployment and advancements in space infrastructure. The adoption of reusable launch vehicles has played a critical role in reducing operational costs and increasing launch frequencies, making space logistics operations more efficient and cost-effective.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Key news & initiatives

- 3.5 Regulatory landscape

- 3.6 Impact forces

- 3.6.1 Growth drivers

- 3.6.1.1 Increased satellite launch demand

- 3.6.1.2 Advancements in space transportation and infrastructure

- 3.6.1.3 Growing reusable launch systems and spacecraft

- 3.6.1.4 Rising demand for complex payload deployment in space

- 3.6.1.5 Shift toward space as a service and flexible models for deploying and managing satellite fleets

- 3.6.2 Industry pitfalls & challenges

- 3.6.2.1 High costs of space operations

- 3.6.2.2 Space traffic management and debris mitigation

- 3.6.1 Growth drivers

- 3.7 Growth potential analysis

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Type, 2021-2034 (USD Million)

- 5.1 Key trends

- 5.2 Mission extension pods (MEPs)

- 5.3 Cargo modules

- 5.4 Service modules

- 5.5 Robotic arms and manipulators

- 5.6 Space tugs

Chapter 6 Market Estimates & Forecast, By Operation, 2021-2034 (USD Million)

- 6.1 Key trends

- 6.2 Last mile delivery

- 6.3 Space situational awareness

- 6.4 Life-extension

- 6.5 Active debris removal

- 6.6 On-orbit assembly and manufacturing

Chapter 7 Market Estimates & Forecast, By Orbit, 2021-2034 (USD Million)

- 7.1 Key trends

- 7.2 Near earth orbit

- 7.3 Lower earth orbit

- 7.4 Geostationary orbit

Chapter 8 Market Estimates & Forecast, By End Use, 2021-2034 (USD Million)

- 8.1 Key trends

- 8.2 Commercial

- 8.3 Government and defense

Chapter 9 Market Estimates & Forecast, By Region, 2021-2034 (USD Million)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 Australia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Arianespace

- 10.2 Astroscale

- 10.3 Atomos Space

- 10.4 Blue Origin

- 10.5 ClearSpace

- 10.6 D-Orbit

- 10.7 Exolaunch

- 10.8 Japan Aerospace Exploration Agency

- 10.9 Lockheed Martin

- 10.10 Maxar Technologies

- 10.11 Northrop Grumman

- 10.12 Rocket Lab

- 10.13 SpaceX

- 10.14 Thales Alenia Space