|

市場調査レポート

商品コード

1665279

ヘマトクリット検査装置の市場機会、成長促進要因、産業動向分析、2025年~2034年予測Hematocrit Test Devices Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| ヘマトクリット検査装置の市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2024年12月19日

発行: Global Market Insights Inc.

ページ情報: 英文 140 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

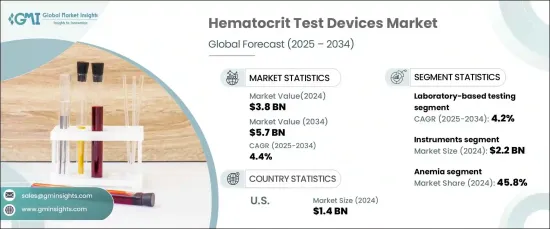

ヘマトクリット検査装置の世界市場は、2024年に38億米ドルと評価され、2025~2034年にかけてCAGR 4.4%で拡大すると予測されています。

この堅調な成長の背景には、血液疾患の有病率の上昇、高齢化人口の増加、ポイントオブケア検査技術の継続的な進歩があります。正確で効率的な診断ツールに対する需要の高まりにより、ヘマトクリット検査装置は医療提供における重要なコンポーネントとして位置づけられています。

市場は機器、試薬、消耗品に区分され、ヘマトクリット検査アナライザとメーターを含む機器カテゴリーが主導権を握っています。2024年には、このセグメントは22億米ドルの最も高い売上を生み出しました。これらの機器は、血球濃度の定期的なモニタリングに不可欠であり、医療と診断の両方の場面でその必要性が強調されています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025~2034 |

| 開始金額 | 38億米ドル |

| 予測金額 | 57億米ドル |

| CAGR | 4.4% |

さらに、市場はラボベースの検査とポイントオブケア(POC)検査を含む検査タイプ別に分類されます。ラボベースの検査が支配的なセグメントとして浮上し、2024年の売上高は25億米ドルを占めました。2025~2034年のCAGRは4.2%と予測され、高精度で信頼性の高い結果を提供できることから、このセグメントは繁栄を続けています。ラボベースのヘマトクリット値検査装置は、貧血、多血症、脱水などのさまざまな症状の診断に不可欠であり、医療診断に欠かせないツールとなっています。

米国は依然として重要な市場参入企業であり、ヘマトクリット検査装置は2024年に14億米ドルの売上を上げます。このセグメントは2025~2034年にかけてCAGR 3.9%で成長すると予測されています。米国人口における貧血、鎌状赤血球症、多血症などの血液疾患の有病率の増加が、信頼性の高いヘマトクリット検査装置に対する需要を煽っています。これらの機器の採用は臨床と在宅医療にまたがり、患者のモニタリングとケアにおいて極めて重要な役割を担っています。

目次

第1章 調査手法と調査範囲

第2章 エグゼクティブサマリー

第3章 産業洞察

- エコシステム分析

- 産業への影響要因

- 促進要因

- 血液疾患の有病率の増加

- ポイントオブケア検査に対する需要の高まり

- 血液学検査における技術の進歩

- 産業の潜在的リスク・課題

- 高度ヘマトクリット測定装置の高コスト

- 促進要因

- 成長可能性分析

- 規制状況

- 技術

- ポーター分析

- PESTEL分析

- ギャップ分析

- 今後の市場動向

- バリューチェーン分析

第4章 競合情勢

- イントロダクション

- 企業マトリックス分析

- 企業シェア分析

- 主要市場参入企業の競合分析

- 競合のポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推定・予測:製品別、2021~2034年

- 主要動向

- 機器

- ヘマトクリット測定アナライザ

- ヘマトクリット測定メーター

- 試薬・消耗品

第6章 市場推定・予測:モダリティ別、2021~2034年

- 主要動向

- ラボベースの検査

- ポイントオブケア(POC)検査

第7章 市場推定・予測:用途別、2021~2034年

- 主要動向

- 貧血

- 先天性心疾患

- 真性多血症

- その他

第8章 市場推定・予測:最終用途別、2021~2034年

- 主要動向

- 病院

- 診断ラボ

- 外来手術センター

- その他

第9章 市場推定・予測:地域別、2021~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第10章 企業プロファイル

- MENARINI Group

- Abbott

- BIO-RAD

- Boule

- Danaher

- Diatron

- EKF Diagnostics

- Roche

- HORIBA Medical

- Mindray

- NIHON KOHDEN

- Nova Biomedical

- SENSA CORE

- SIEMENS Healthineers

- Sysmex

The Global Hematocrit Test Devices Market was valued at USD 3.8 billion in 2024 and is projected to expand at a CAGR of 4.4% from 2025 to 2034. This robust growth is driven by a rising prevalence of blood disorders, a growing aging population, and continuous advancements in point-of-care testing technologies. The increasing demand for precise and efficient diagnostic tools positions hematocrit test devices as a critical component in healthcare delivery.

The market is segmented into instruments, reagents, and consumables, with the instruments category-comprising hematocrit test analyzers and meters-leading the charge. In 2024, this segment generated the highest revenue of USD 2.2 billion. These devices are indispensable for the regular monitoring of blood cell concentrations, underscoring their necessity in both medical and diagnostic settings.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $3.8 Billion |

| Forecast Value | $5.7 Billion |

| CAGR | 4.4% |

Additionally, the market is categorized by testing type, including laboratory-based testing and point-of-care (POC) testing. Laboratory-based testing emerged as the dominant segment, accounting for USD 2.5 billion in revenue in 2024. With a projected CAGR of 4.2% from 2025 to 2034, this segment continues to thrive due to its ability to deliver highly precise and reliable results. Laboratory-based hematocrit testing devices are crucial for diagnosing a range of conditions, such as anemia, polycythemia, and dehydration, making them an essential tool in healthcare diagnostics.

The U.S. remains a significant market player, with hematocrit test devices generating USD 1.4 billion in revenue in 2024. This segment is forecasted to grow at a CAGR of 3.9% between 2025 and 2034. The increasing prevalence of blood disorders, such as anemia, sickle cell disease, and polycythemia, within the U.S. population fuels the demand for reliable hematocrit testing equipment. The adoption of these devices spans clinical and home healthcare settings, ensuring their pivotal role in patient monitoring and care.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence of blood disorders

- 3.2.1.2 Growing demand for point-of-care testing

- 3.2.1.3 Technological advancements in hematology testing

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of advanced hematocrit devices

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Technology landscape

- 3.6 Porter’s analysis

- 3.7 PESTEL analysis

- 3.8 Gap analysis

- 3.9 Future market trends

- 3.10 Value chain analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Product, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Instruments

- 5.2.1 Hematocrit test analyzer

- 5.2.2 Hematocrit test meter

- 5.3 Reagents and consumables

Chapter 6 Market Estimates and Forecast, By Modality, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Laboratory-based testing

- 6.3 Point-of-care (POC) testing

Chapter 7 Market Estimates and Forecast, By Application, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Anemia

- 7.3 Congenital heart diseases

- 7.4 Polycythemia vera

- 7.5 Other applications

Chapter 8 Market Estimates and Forecast, By End Use, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Hospitals

- 8.3 Diagnostic laboratories

- 8.4 Ambulatory surgical centers

- 8.5 Other end users

Chapter 9 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 MENARINI Group

- 10.2 Abbott

- 10.3 BIO-RAD

- 10.4 Boule

- 10.5 Danaher

- 10.6 Diatron

- 10.7 EKF Diagnostics

- 10.8 Roche

- 10.9 HORIBA Medical

- 10.10 Mindray

- 10.11 NIHON KOHDEN

- 10.12 Nova Biomedical

- 10.13 SENSA CORE

- 10.14 SIEMENS Healthineers

- 10.15 Sysmex