眼科用ルーペの市場機会、成長促進要因、産業動向分析、2025年~2034年予測

Ophthalmic Loupes Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 150 Pages

- 納期

- 2~3営業日

- 商品コード

- 1665261

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

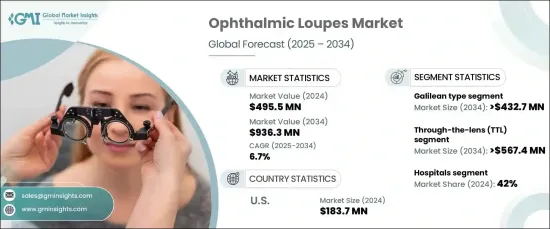

世界の眼科用ルーペ市場は、2024年には4億9,550万米ドルとなり、2025~2034年にかけてCAGR 6.7%という驚異的な成長が予測されています。

この力強い成長の原動力は、眼科手術における精密ツールに対する需要の高まりです。眼科手術がますます複雑になるにつれて、医療専門家は手術の精度を高め、リスクを減らすために眼科ルーペのような高精度の器具に目を向けています。

低侵襲手術への嗜好の高まりも、眼科用ルーペの採用に大きく貢献しています。このような手術では、卓越した鮮明さと精度が要求されますが、最新のルーペは先進的拡大技術によってこれを実現しています。LED照明、軽量材料、人間工学に基づいたデザインなどの技術革新は、快適性と使いやすさをさらに向上させ、医療従事者にとって不可欠なツールとしての地位を確固たるものにしています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025~2034 |

| 開始金額 | 4億9,550万米ドル |

| 予測金額 | 9億3,630万米ドル |

| CAGR | 6.7% |

製品タイプ別では、ガリレオタイプ、プリズムタイプ、プレートタイプルーペがあります。このうち、ガリレオタイプはCAGR 6.8%で顕著な成長を遂げ、2034年には4億3,270万米ドルに達すると予測されています。ガリレオタイプルーペは、手頃な価格、使いやすさ、軽量設計が魅力で、日常的な眼科検査や手術に最適です。ガリレオタイプルーペは、2枚または3枚のレンズを備えたシンプルな光学構造が特徴で、長時間の使用でも快適な使い心地を確保しながら、鮮明な倍率を実現します。

同市場はまた、スルー・ザ・レンズ(TTL)やフリップアップなど、デザインタイプによっても分類されます。TTLルーペはCAGR 6.4%で安定した成長を遂げ、2034年には5億6,740万米ドルに達すると予測されています。特注設計で有名なTTLルーペは、個々のニーズに合わせた比類のない光学的透明度を記載しています。人間工学に基づいた機能により、長時間の手術でも負担が少なく、効率と満足度の両方が向上します。特に低侵襲性眼科手術における精密機器への需要の高まりが、TTLセグメントの拡大を推進しています。

米国の眼科用ルーペ市場は、2024年に1億8,370万米ドルを占め、2025~2034年にかけてCAGR 6.2%で成長すると予測されています。この成長を促進する要因としては、白内障、緑内障、糖尿病網膜症、黄斑変性症などの眼科疾患の有病率の増加が挙げられます。これらの疾患は正確な診断と外科的介入を必要とするため、眼科用ルーペのような専門的ツールの需要が高まっています。さらに、人口の高齢化、糖尿病や慢性疾患の罹患率の増加が、米国における先進的眼科ソリューションの必要性をさらに際立たせています。

目次

第1章 調査手法と調査範囲

第2章 エグゼクティブサマリー

第3章 産業洞察

- エコシステム分析

- 産業への影響要因

- 促進要因

- 眼科疾患の有病率の増加

- 眼科手術件数の増加

- ルーペの技術的進歩

- 低侵襲手術への需要の高まり

- 人間工学に基づいたカスタマイズ可能なデザインへのシフト

- 産業の潜在的リスク・課題

- 先進的ルーペの高コスト

- カスタマイズとフィット感の課題

- 促進要因

- 成長可能性分析

- 規制状況

- 技術

- ギャップ分析

- ポーター分析

- PESTEL分析

- 今後の市場動向

- バリューチェーン分析

第4章 競合情勢

- イントロダクション

- 企業マトリックス分析

- 企業シェア分析

- 主要市場参入企業の競合分析

- 競合のポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推定・予測:製品タイプ別、2021~2034年

- 主要動向

- ガリレオタイプ

- プリズムタイプ

- プレートタイプ

第6章 市場推定・予測:デザインタイプ別、2021~2034年

- 主要動向

- スルー・ザ・レンズ(TTL)

- フリップアップ

第7章 市場推定・予測:最終用途別、2021~2034年

- 主要動向

- 病院

- 眼科クリニック

- 外来手術センター(ASC)

- その他

第8章 市場推定・予測:地域別、2021~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第9章 企業プロファイル

- DentLight

- Designs for Vision

- ErgonoptiX

- Heine Optotechnik

- Keeler

- Lumadent

- NEITZ

- Ocutech

- Orascoptic

- Q-Optics

- Rudolf Riester

- SHEERVISION

- SurgiTel

- Univet

- ZEISS

目次

The Global Ophthalmic Loupes Market was valued at USD 495.5 million in 2024 and is forecasted to grow at an impressive CAGR of 6.7% from 2025 to 2034. This robust growth is fueled by the rising demand for precision tools in ophthalmic surgeries. As eye care procedures become increasingly intricate, healthcare professionals are turning to high-precision instruments like ophthalmic loupes to enhance surgical accuracy and reduce risks.

The growing preference for minimally invasive surgeries has also significantly contributed to the adoption of ophthalmic loupes. These procedures demand exceptional clarity and precision, which modern loupes provide through advanced magnification technologies. Innovations such as LED lighting, lightweight materials, and ergonomic designs have further enhanced comfort and usability, solidifying their position as essential tools for medical professionals.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $495.5 Million |

| Forecast Value | $ 936.3 Million |

| CAGR | 6.7% |

By product type, the market includes galilean, prismatic, and plate loupes. Among these, the galilean type is expected to witness remarkable growth at a CAGR of 6.8%, generating USD 432.7 million by 2034. Its widespread appeal lies in its affordability, ease of use, and lightweight design, making it an excellent choice for routine ophthalmic tests and surgeries. Featuring a straightforward optical structure with two or three lenses, galilean loupes provide clear magnification while ensuring user comfort during prolonged use.

The market is also categorized by design type, including through-the-lens (TTL) and flip-up designs. TTL loupes are projected to experience steady growth at a CAGR of 6.4%, reaching USD 567.4 million by 2034. Renowned for their custom-built design, TTL loupes offer unparalleled optical clarity tailored to individual needs. Their ergonomic features minimize strain during extended procedures, enhancing both efficiency and user satisfaction. The rising demand for precision tools, particularly in minimally invasive eye surgeries, continues to propel the expansion of the TTL segment.

The U.S. ophthalmic loupes market accounted for USD 183.7 million in 2024 and is anticipated to grow at a CAGR of 6.2% between 2025 and 2034. Factors driving this growth include the increasing prevalence of ophthalmic conditions such as cataracts, glaucoma, diabetic retinopathy, and macular degeneration. These conditions require precise diagnostic and surgical interventions, elevating the demand for specialized tools like ophthalmic loupes. Additionally, an aging population and the growing incidence of diabetes and chronic diseases further underscore the need for advanced ophthalmic solutions in the U.S.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence of ophthalmic disorders

- 3.2.1.2 Rising number of ophthalmic surgeries

- 3.2.1.3 Technological advancements in loupes

- 3.2.1.4 Growing demand for minimally invasive procedures

- 3.2.1.5 Shift toward ergonomic and customizable designs

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of advanced loupes

- 3.2.2.2 Challenges in customization and fit

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Technology landscape

- 3.6 Gap analysis

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

- 3.9 Future market trends

- 3.10 Value chain analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Galilean type

- 5.3 Prismatic type

- 5.4 Plate loupe type

Chapter 6 Market Estimates and Forecast, By Design Type, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Through-the-lens (TTL)

- 6.3 Flip up

Chapter 7 Market Estimates and Forecast, By End Use, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 Ophthalmic clinics

- 7.4 Ambulatory surgical centers (ASCs)

- 7.5 Other end users

Chapter 8 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 DentLight

- 9.2 Designs for Vision

- 9.3 ErgonoptiX

- 9.4 Heine Optotechnik

- 9.5 Keeler

- 9.6 Lumadent

- 9.7 NEITZ

- 9.8 Ocutech

- 9.9 Orascoptic

- 9.10 Q-Optics

- 9.11 Rudolf Riester

- 9.12 SHEERVISION

- 9.13 SurgiTel

- 9.14 Univet

- 9.15 ZEISS

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 150 Pages

- 納期

- 2~3営業日