ディスプレイ材料市場の市場機会、成長促進要因、産業動向分析、2025~2034年予測

Display Material Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 210 Pages

- 納期

- 2~3営業日

- 商品コード

- 1665212

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

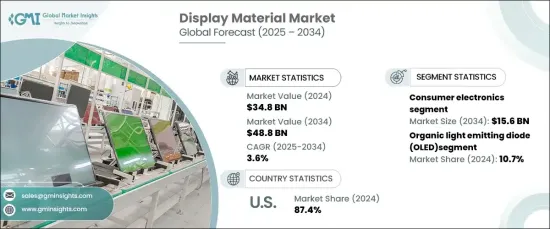

世界のディスプレイ材料市場は、2024年に348億米ドルと評価され、2025~2034年にかけて3.6%のCAGRで堅調に拡大すると予想されています。

この成長の原動力となっているのは、スマートフォン、タブレット端末、ウェアラブル端末などの先進的民生用電子機器製品に対する需要の高まりであり、消費者は、強化されたビジュアル品質、鮮やかな色彩、優れたエネルギー効率を備えたデバイスを求めるようになっています。

ディスプレイ材料における技術革新は産業に革命をもたらし、メーカー各社は省エネ需要にも対応した高品質の視覚体験を実現できるようになっています。また、軟質ディスプレイや折りたたみ式ディスプレイの人気が高まっていることも、特にプレミアムデバイスの需要を牽引しています。この動向は、ディスプレイ技術の絶え間ない進化によってさらに加速され、消費者が省エネを推進しながら先進的視覚機能を備えた製品に簡単にアクセスできるようになっています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025~2034 |

| 開始金額 | 348億米ドル |

| 予測金額 | 488億米ドル |

| CAGR | 3.6% |

ディスプレイ材料市場は主に技術別に区分され、マイクロLEDディスプレイ、有機発光ダイオード(OLED)、液晶ディスプレイ(LCD)、量子ドットディスプレイ、電子ペーパーディスプレイ(EPD)などが含まれます。OLED技術は、2024年には10.7%という大きなシェアを占めます。この技術は、より深い黒、鮮やかな色、より速い応答時間を実現する自己発光ピクセルで認知されています。OLEDの薄型で柔軟な設計は、スマートフォン、テレビ、新興の拡張現実(AR)と仮想現実(VR)アプリケーションのハイエンドディスプレイにとって理想的な選択肢であり、最先端機器に最適な技術としての地位を確固たるものにしています。

用途別では、ディスプレイ材料市場は、民生用電子機器、自動車、医療、小売、産業、企業など複数の産業にまたがっています。民生用電子機器セグメントは2034年までに156億米ドルに達すると予測され、引き続き市場最大の収益源となっています。この拡大は、ノートパソコン、ゲーム用モニター、スマートウェアラブルなどの製品で、高解像度でエネルギー効率の高いディスプレイを好む消費者が増えていることに起因しています。ディスプレイは今や不可欠な部品であり、現代の民生用電子機器製品の機能性と美的魅力の両方を高めています。

米国のディスプレイ材料市場は、急速な技術進歩、高い消費支出、革新的なデバイスの迅速な導入が原動力となり、2024年には87.4%の圧倒的シェアを占めます。AR、VR、車載ディスプレイ、医療画像システムにおけるディスプレイ技術の統合が進んでいることが、同地域の市場需要をさらに押し上げています。さらに、大手メーカーによる研究開発への多額の投資は、米国がディスプレイ材料革新の世界的リーダーとしての地位を強化するのに役立っています。

目次

第1章 調査手法と調査範囲

- 市場範囲と定義

- 基本推定と計算

- 予測計算

- データソース

- 1次データ

- 二次資料

- 有料情報源

- 公的情報源

第2章 エグゼクティブサマリー

第3章 産業洞察

- エコシステム分析

- バリューチェーンに影響を与える要因

- 利益率分析

- 変革

- 将来の展望

- メーカー

- 流通業者

- サプライヤーの状況

- 利益率分析

- 主要ニュース

- 規制状況

- 影響要因

- 促進要因

- 先端コンシューマー・エレクトロニクスの需要急増

- 自動車用ディスプレイセグメントの成長

- ディスプレイ技術の急速な進歩

- 高解像度ディスプレイの普及拡大

- 産業の潜在的リスク・課題

- 高い生産コストと設備投資の必要性

- サプライチェーンの混乱と資源依存

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 競合のポジショニングマトリックス

- 戦略展望マトリックス

第5章 市場推定・予測:材料別、2021~2034年

- 主要動向

- 偏光板

- ガラス基板

- カラーフィルター

- 液晶(LC)

- バックライトユニット(BLU)

- 接着剤

- インジウム・スズ酸化物(ITO)

- その他

第6章 市場推定・予測:用途別、2021~2034年

- 主要動向

- 民生用電子機器

- 自動車

- 医療

- 小売

- 産業・企業

- その他

第7章 市場推定・予測:技術別、2021~2034年

- 主要動向

- 液晶ディスプレイ(LCD)

- 有機発光ダイオード(OLED)

- 量子ドットディスプレイ

- マイクロLEDディスプレイ

- 電子ペーパーディスプレイ(EPD)

第8章 市場推定・予測:地域別、2021~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- ラテンアメリカ

- ブラジル

- メキシコ

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第9章 企業プロファイル

- 3M Company

- AGC Inc.(Asahi Glass Co., Ltd.)

- AU Optronics Corporation

- BOE Technology Group Co., Ltd.

- Corning Incorporated

- DIC Corporation

- DowDuPont Inc.

- Hitachi Chemical Co., Ltd.

- Idemitsu Kosan Co., Ltd.

- Innolux Corporation

- Japan Display Inc.

- JNC Corporation

- Kyulux, Inc.

- LG Chem, Ltd.

- Lumileds Holding B.V.

- Merck KGaA

- Nanoco Technologies Limited

- Nitto Denko Corporation

- Samsung Display Co., Ltd.

- Sumitomo Chemical Co., Ltd.

- Toray Industries, Inc.

- Universal Display Corporation

目次

The Global Display Material Market was valued at USD 34.8 billion in 2024 and is expected to expand at a robust CAGR of 3.6% from 2025 to 2034. This growth is fueled by the rising demand for advanced consumer electronics, such as smartphones, tablets, and wearables, as consumers increasingly seek devices with enhanced visual quality, vibrant colors, and superior energy efficiency.

Technological innovations in display materials are revolutionizing the industry, enabling manufacturers to create high-quality visual experiences that also meet energy-saving demands. The growing popularity of flexible and foldable displays is also driving market demand, especially in premium devices. This trend is further accelerated by the continuous evolution of display technologies, making it easier for consumers to access products with advanced visual capabilities while promoting energy conservation.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $34.8 Billion |

| Forecast Value | $48.8 Billion |

| CAGR | 3.6% |

The display material market is primarily segmented by technology, including micro-LED display, organic light-emitting diode (OLED), liquid crystal display (LCD), quantum dot display, and e-paper display (EPD). OLED technology dominated in 2024, accounting for a significant share of 10.7%. This technology is recognized for its self-emissive pixels, which deliver deeper blacks, vibrant colors, and faster response times. OLED's thin, flexible design makes it an ideal choice for high-end displays in smartphones, televisions, and emerging augmented reality (AR) and virtual reality (VR) applications, solidifying its position as the go-to technology for cutting-edge devices.

In terms of application, the display material market spans several industries, including consumer electronics, automotive, healthcare, retail, industrial and enterprise sectors, among others. The consumer electronics segment is projected to reach USD 15.6 billion by 2034, continuing to be the largest source of revenue in the market. This expansion is attributed to the increasing consumer preference for high-resolution, energy-efficient displays in products such as laptops, gaming monitors, and smart wearables. Displays are now an essential component, enhancing both the functionality and aesthetic appeal of modern consumer electronics.

The U.S. display material market held a dominant share of 87.4% in 2024, driven by rapid technological advancements, high consumer spending, and the swift adoption of innovative devices. The growing integration of display technologies in AR, VR, automotive displays, and healthcare imaging systems further fuels market demand in the region. Furthermore, substantial investments in research and development by leading manufacturers help reinforce the U.S.'s position as a global leader in display material innovation.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Key news & initiatives

- 3.5 Regulatory landscape

- 3.6 Impact forces

- 3.6.1 Growth drivers

- 3.6.1.1 Surging demand for advanced consumer electronics

- 3.6.1.2 Growth of the automotive display sector

- 3.6.1.3 Rapid advancements in display technologies

- 3.6.1.4 Increasing penetration of high-resolution displays

- 3.6.2 Industry pitfalls & challenges

- 3.6.2.1 High production costs and capital investment requirements

- 3.6.2.2 Supply chain disruptions and resource dependence

- 3.6.1 Growth drivers

- 3.7 Growth potential analysis

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Material, 2021-2034 (USD Billion)

- 5.1 Key trends

- 5.2 Polarizers

- 5.3 Glass substrates

- 5.4 Color filters

- 5.5 Liquid crystals (LC)

- 5.6 Backlighting units (BLU)

- 5.7 Adhesives

- 5.8 Indium tin oxide (ITO)

- 5.9 Others

Chapter 6 Market Estimates & Forecast, By Application, 2021-2034 (USD Billion)

- 6.1 Key trends

- 6.2 Consumer electronics

- 6.3 Automotive

- 6.4 Healthcare

- 6.5 Retail

- 6.6 Industrial and enterprise

- 6.7 Others

Chapter 7 Market Estimates & Forecast, By Technology, 2021-2034 (USD Billion)

- 7.1 Key trends

- 7.2 Liquid crystal display (LCD)

- 7.3 Organic light emitting diode (OLED)

- 7.4 Quantum dot display

- 7.5 Micro LED display

- 7.6 E-paper display (EPD)

Chapter 8 Market Estimates & Forecast, By Region, 2021-2034 (USD Billion)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 UK

- 8.3.2 Germany

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Russia

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 South Korea

- 8.4.5 Australia

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.6 MEA

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 3M Company

- 9.2 AGC Inc. (Asahi Glass Co., Ltd.)

- 9.3 AU Optronics Corporation

- 9.4 BOE Technology Group Co., Ltd.

- 9.5 Corning Incorporated

- 9.6 DIC Corporation

- 9.7 DowDuPont Inc.

- 9.8 Hitachi Chemical Co., Ltd.

- 9.9 Idemitsu Kosan Co., Ltd.

- 9.10 Innolux Corporation

- 9.11 Japan Display Inc.

- 9.12 JNC Corporation

- 9.13 Kyulux, Inc.

- 9.14 LG Chem, Ltd.

- 9.15 Lumileds Holding B.V.

- 9.16 Merck KGaA

- 9.17 Nanoco Technologies Limited

- 9.18 Nitto Denko Corporation

- 9.19 Samsung Display Co., Ltd.

- 9.20 Sumitomo Chemical Co., Ltd.

- 9.21 Toray Industries, Inc.

- 9.22 Universal Display Corporation

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 210 Pages

- 納期

- 2~3営業日