|

市場調査レポート

商品コード

1665183

降圧剤市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測Antihypertensive Drugs Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 降圧剤市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2024年12月13日

発行: Global Market Insights Inc.

ページ情報: 英文 140 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

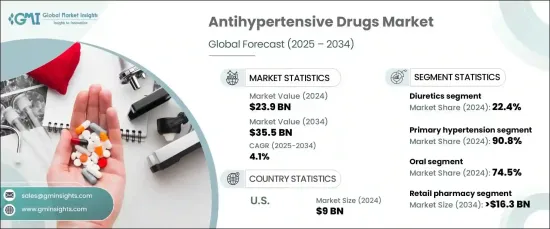

降圧剤の世界市場は、2024年に239億米ドルと評価され、2025年から2034年にかけてCAGR4.1%で拡大する見通しです。

この成長は、世界の高血圧の有病率の増加によるところが大きいです。高血圧は無症状であり、深刻な健康リスクがあるため、しばしば「サイレント・キラー」と呼ばれます。

人口の高齢化や、食生活の乱れ、ストレス、運動不足といった生活習慣の悪化が進むにつれて、高血圧率は上昇を続け、効果的な治療法への需要が高まっています。薬剤製剤の絶え間ない進歩は、遠隔モニタリングや個別化された投薬計画のようなデジタルヘルス技術の統合と相まって、治療風景を再構築しています。さらに、心臓病や脳卒中など、管理されていない高血圧に関連する合併症に対する意識の高まりが、早期診断と積極的な治療の導入を促し、降圧剤の持続的な需要を確保しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 239億米ドル |

| 予測金額 | 355億米ドル |

| CAGR | 4.1% |

市場は治療タイプ別に利尿薬、ACE阻害薬、アンジオテンシン受容体拮抗薬、ベータ遮断薬、カルシウム拮抗薬、レニン阻害薬、アルファ遮断薬、血管拡張薬、その他の治療に分類されます。2024年には、血圧を下げる効果が認められているサイアザイド系利尿薬が広く使用されているため、利尿薬部門が22.4%と最大のシェアを占めました。このセグメントにはループ利尿薬やカリウム温存利尿薬も含まれ、多様な治療ニーズに対応しています。もう一つの主要カテゴリーであるベータ遮断薬は、さらにベータ1選択性と内因性交感神経刺激性に区分され、個々の患者のニーズに基づいた個別化ソリューションを提供しています。

薬剤の種類別に見ると、市場は一次性高血圧治療薬と二次性高血圧治療薬に分かれます。一次性高血圧治療は、この疾患の世界の有病率の高さを反映し、2024年の市場シェアで90.8%を占めています。一次性高血圧は、ライフスタイルや遺伝的要因に関連することが多く、効果的で長期的な治療オプションの必要性が高まっています。

米国は降圧剤市場における支配的な地位を維持しており、2024年には90億米ドルの売上を計上します。このリーダーシップは、高血圧罹患率の高さ、強固なヘルスケアインフラ、研究開発への多額の投資に起因しています。革新的な治療法に対する規制当局の承認により、患者は最先端の薬剤を利用できるようになり、市場の成長をさらに促進しています。また、早期診断キャンペーンや先進的な治療プロトコルに注力することで、国全体での普及率も加速しています。

目次

第1章 調査手法と調査範囲

- 市場スコープと定義

- 調査デザイン

- 調査アプローチ

- データ収集方法

- 基本推定と計算

- 基準年の算出

- 市場推計の主要動向

- 予測モデル

- 1次調査と検証

- 一次情報

- データマイニングソース

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- 業界への影響要因

- 促進要因

- 高血圧有病率の増加

- 高血圧治療薬開発と製剤の進歩

- 高血圧のリスクに対する意識の高まり

- 治療戦略におけるデジタルヘルスソリューションの統合

- 業界の潜在的リスク&課題

- 降圧治療中の服薬アドヒアランスの低下

- 厳しい規制の存在

- 促進要因

- 成長可能性分析

- 規制状況

- 技術的展望

- 特許分析

- ギャップ分析

- 将来の市場動向

- ポーターの分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 主要市場プレーヤーの競合分析

- 競合のポジショニングマトリックス

- 戦略展望

第5章 市場推計・予測:治療法別、2021年~2034年

- 主要動向

- 利尿薬

- サイアザイド系利尿薬

- ループ利尿薬

- カリウム温存利尿薬

- ACE阻害薬

- アンジオテンシン受容体拮抗薬

- ベータ遮断薬

- ベータ1選択的

- 内因性交感神経刺激薬

- カルシウム拮抗薬

- レニン阻害薬

- アルファ遮断薬

- 血管拡張薬

- その他の治療薬

第6章 市場推計・予測:薬剤タイプ別、2021年~2034年

- 主要動向

- 一次性高血圧

- 二次性高血圧

第7章 市場推計・予測:投与経路別、2021年~2034年

- 主要動向

- 経口剤

- 注射剤

- その他の投与経路

第8章 市場推計・予測:流通チャネル別、2021年~2034年

- 主要動向

- 小売薬局

- 病院薬局

- オンライン薬局

第9章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第10章 企業プロファイル

- AbbVie

- AstraZeneca

- Bayer AG

- Boehringer Ingelheim International GmbH

- Daiichi Sankyo Company

- Johnson &Johnson Services

- Lupin

- Merck &Co

- Noden Pharma DAC

- Novartis AG

- Pfizer

- Sanofi

- Sun Pharmaceutical Industries

- Takeda Pharmaceutical

- Torrent Pharmaceuticals

The Global Antihypertensive Drugs Market, valued at USD 23.9 billion in 2024, is set to expand at a compound annual growth rate (CAGR) of 4.1% from 2025 to 2034. This growth is largely driven by the increasing prevalence of hypertension worldwide, a condition often referred to as the "silent killer" due to its asymptomatic nature and severe health risks.

As populations age and lifestyle factors such as poor diet, stress, and lack of exercise persist, hypertension rates continue to rise, fueling the demand for effective treatments. Continuous advancements in drug formulations, coupled with the integration of digital health technologies like remote monitoring and personalized medication plans, are reshaping treatment landscapes. Furthermore, heightened awareness of the complications associated with unmanaged hypertension, such as heart disease and stroke, is encouraging early diagnosis and proactive treatment adoption, ensuring a sustained demand for antihypertensive drugs.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $23.9 Billion |

| Forecast Value | $35.5 Billion |

| CAGR | 4.1% |

The market is categorized by therapy type into diuretics, ACE inhibitors, angiotensin receptor blockers, beta blockers, calcium channel blockers, renin inhibitors, alpha-blockers, vasodilators, and other treatments. In 2024, the diuretics segment commanded the largest share at 22.4%, thanks to the widespread use of thiazide diuretics, which are recognized for their effectiveness in reducing blood pressure. This segment also includes loop and potassium-sparing diuretics, catering to diverse treatment requirements. Beta blockers, another key category, are further segmented into beta-1 selective and intrinsic sympathomimetic variants, offering personalized solutions based on individual patient needs.

By drug type, the market divides into treatments for primary and secondary hypertension. Primary hypertension treatments dominated with a commanding 90.8% market share in 2024, reflecting the high global prevalence of this condition. Primary hypertension, often linked to lifestyle and genetic factors, underscores the growing need for effective, long-term treatment options.

The United States remains a dominant player in the antihypertensive drugs market, generating USD 9 billion in revenue in 2024. This leadership is attributed to the high incidence of hypertension, coupled with robust healthcare infrastructure and significant investment in research and development. Regulatory approvals for innovative therapies are enabling patients to access cutting-edge medications, further driving market growth. The focus on early diagnosis campaigns and advanced treatment protocols is also accelerating adoption rates across the country.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates & calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing prevalence of hypertension

- 3.2.1.2 Advances in hypertensive drug development and formulations

- 3.2.1.3 Growing awareness about the risks of hypertension

- 3.2.1.4 Integration of digital health solutions in treatment strategies

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 Poor medication adherence during antihypertensive treatments

- 3.2.2.2 Presence of stringent regulations

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Technological landscape

- 3.6 Patent analysis

- 3.7 Gap analysis

- 3.8 Future market trends

- 3.9 Porter’s analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy outlook

Chapter 5 Market Estimates and Forecast, By Therapy, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Diuretics

- 5.2.1 Thiazide diuretics

- 5.2.2 Loop diuretics

- 5.2.3 Potassium-sparing diuretics

- 5.3 ACE inhibitors

- 5.4 Angiotensin receptor blockers

- 5.5 Beta blockers

- 5.5.1 Beta-1 selective

- 5.5.2 Intrinsic sympathomimetic

- 5.6 Calcium channel blockers

- 5.7 Renin inhibitors

- 5.8 Alpha-blockers

- 5.9 Vasodilators

- 5.10 Other therapies

Chapter 6 Market Estimates and Forecast, By Drug Type, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Primary hypertension

- 6.3 Secondary hypertension

Chapter 7 Market Estimates and Forecast, By Route of Administration, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Oral

- 7.3 Injectables

- 7.4 Other routes of administration

Chapter 8 Market Estimates and Forecast, By Distribution Channel, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Retail pharmacy

- 8.3 Hospital pharmacy

- 8.4 Online pharmacy

Chapter 9 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 AbbVie

- 10.2 AstraZeneca

- 10.3 Bayer AG

- 10.4 Boehringer Ingelheim International GmbH

- 10.5 Daiichi Sankyo Company

- 10.6 Johnson & Johnson Services

- 10.7 Lupin

- 10.8 Merck & Co

- 10.9 Noden Pharma DAC

- 10.10 Novartis AG

- 10.11 Pfizer

- 10.12 Sanofi

- 10.13 Sun Pharmaceutical Industries

- 10.14 Takeda Pharmaceutical

- 10.15 Torrent Pharmaceuticals