|

市場調査レポート

商品コード

1664869

自動車用スターターモーターの市場機会、成長促進要因、産業動向分析、2025年~2034年予測Automotive Starter Motor Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 自動車用スターターモーターの市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2024年12月03日

発行: Global Market Insights Inc.

ページ情報: 英文 240 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

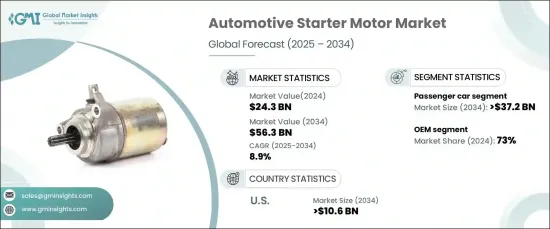

世界の自動車用スターターモーター市場は、2024年に243億米ドルとなり、2025年から2034年までのCAGRは8.9%と予測され、著しい成長が見込まれています。

この急成長の背景には、ギア減速機構や軽量設計など、スターターモーター技術の最先端の進歩があります。こうした技術革新は、効率を高めるだけでなく、エネルギー消費量を削減し、自動車性能を向上させます。

市場は乗用車と商用車に区分され、2024年の市場シェアは乗用車が67%と圧倒的です。2034年までに、このセグメントは372億米ドルの驚異的な利益を生み出すと予測されています。この成長を後押しする主な要因には、パーソナルモビリティに対する需要の高まり、急速な都市化、特に新興市場における可処分所得の増加などがあります。さらに、燃費効率を高め、厳しい排ガス基準に適合するように設計されたスタートストップシステムの進歩は、主に乗用車に組み込まれています。このような持続的な需要は、現代の自動車ソリューションにおいて高度で耐久性のあるスターターモーターが極めて重要な役割を果たしていることを裏付けています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025年~2034年 |

| 開始金額 | 243億米ドル |

| 予測金額 | 563億米ドル |

| CAGR | 8.9% |

市場はまた、相手先商標製品メーカー(OEM)とアフターマーケットに分かれており、2024年の市場シェアはOEMが73%を占めました。自動車生産に直接関与するOEMは、シームレスな統合、優れた品質、信頼性の向上を保証します。自動車メーカーは、スターターモーターを大量に調達し、最適化されたサプライチェーンを活用することでコスト効率を高めています。さらに、厳しい性能と規制ベンチマークを満たす必要性により、最先端のスターターモーターソリューションのプロバイダーとしてのOEMの優位性はさらに強固なものとなっています。

米国の自動車用スターターモーター市場は2024年に85%のシェアを占め、2034年までには106億米ドルに達すると予測されています。同国の優位性は、自動車製造エコシステムが確立していることと、スタートストップシステムのような先進技術を搭載した自動車の需要が高いことに起因しています。燃費効率を促進する規制措置により、エネルギー効率の高いスターターモーターの採用が加速しています。さらに、大手自動車メーカーや部品メーカーが存在し、強固なサプライチェーンネットワークが構築されていることも、米国市場のリーダーシップを強化しています。

目次

第1章 調査手法と調査範囲

- 調査デザイン

- 調査アプローチ

- データ収集方法

- 基本推定と計算

- 基準年の算出

- 市場推計の主要動向

- 予測モデル

- 一次調査と検証

- 一次ソース

- データマイニングソース

- 市場定義

第2章 エグゼクティブサマリー

第3章 業界洞察

- 業界エコシステム分析

- 技術プロバイダー

- 部品サプライヤー

- メーカー

- OEMメーカー

- サプライヤーの状況

- 利益率分析

- 技術革新の状況

- 主なニュースと取り組み

- 規制状況

- 影響要因

- 成長促進要因

- 自動車生産・販売の増加

- スターターモーター技術の進歩

- 電気自動車とハイブリッド車の成長

- 燃費と排ガス規制への関心の高まり

- 業界の潜在的リスク・課題

- 高い導入コスト

- 厳しい規制

- 成長促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業市場シェア分析

- 競合のポジショニングマトリックス

- 戦略展望マトリックス

第5章 市場推計・予測:スターターモーター別、2021年~2034年

- 主要動向

- 電動スターターモーター

- 空気圧スターターモーター

- 油圧スターターモーター

- その他

第6章 市場推計・予測:車両別、2021年~2034年

- 主要動向

- 乗用車

- 商用車

第7章 市場推計・予測:定格出力別、2021年~2034年

- 主要動向

- 1.5kW未満

- 1.5~2.5kW

- 2.5kW以上

第8章 市場推計・予測:販売チャネル別、2021年~2034年

- 主要動向

- OEM

- アフターマーケット

第9章 市場推計・予測:地域別、2021~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- スペイン

- イタリア

- ロシア

- 北欧

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- ニュージーランド

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- UAE

- 南アフリカ

- サウジアラビア

第10章 企業プロファイル

- BorgWarner Inc.

- Bosch

- Delco Remy

- DENSO

- Dongfeng Motor Parts and Components Group Co., Ltd.

- GDST Auto Parts

- Hella KGaA Hueck &Co.

- Hitachi Automotive Systems

- Lucas Electrical

- Magneti Marelli

- MITSUBA Corporation

- Mitsubishi Electric Corporation

- Nikko Electric Industry Co., Ltd.

- Prestolite Electric

- Remy International

- Sawafuji Electric Co., Ltd.

- TYK Automotive Electric Co., Ltd.

- Unitech Automotive Electrical Appliance Co., Ltd.

- Valeo

- WAI Global

The Global Automotive Starter Motor Market, valued at USD 24.3 billion in 2024, is poised for remarkable growth, with a projected robust CAGR of 8.9% from 2025 to 2034. This surge is fueled by cutting-edge advancements in starter motor technologies, such as gear reduction mechanisms and lightweight designs. These innovations not only enhance efficiency but also reduce energy consumption and improve vehicle performance, aligning with the automotive industry's increasing emphasis on fuel efficiency and emissions reduction.

The market is segmented into passenger cars and commercial vehicles, with passenger cars dominating at 67% of the market share in 2024. By 2034, this segment is projected to generate an impressive USD 37.2 billion. Key factors propelling this growth include rising demand for personal mobility, rapid urbanization, and higher disposable incomes, especially in emerging markets. Furthermore, advancements in start-stop systems, designed to boost fuel efficiency and comply with stringent emission standards, are predominantly integrated into passenger vehicles. This sustained demand underscores the pivotal role of advanced and durable starter motors in modern automotive solutions.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $24.3 billion |

| Forecast Value | $56.3 billion |

| CAGR | 8.9% |

The market is also divided between original equipment manufacturers (OEMs) and the aftermarket, with OEMs commanding a significant 73% market share in 2024. Their direct involvement in vehicle production ensures seamless integration, superior quality, and enhanced reliability. Automakers leverage cost efficiencies by sourcing starter motors in bulk and utilizing optimized supply chains. Additionally, the need to meet stringent performance and regulatory benchmarks further solidifies OEMs' dominance as providers of state-of-the-art starter motor solutions.

The U.S. automotive starter motor market held an 85% share in 2024 and is forecasted to reach USD 10.6 billion by 2034. The nation's dominance can be attributed to its well-established automotive manufacturing ecosystem and high demand for vehicles equipped with advanced technologies like start-stop systems. Regulatory measures promoting fuel efficiency have accelerated the adoption of energy-efficient starter motors. Furthermore, the presence of leading automakers and component manufacturers, coupled with robust supply chain networks, reinforces the U.S. market's leadership.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Technology providers

- 3.1.2 Component suppliers

- 3.1.3 Manufacturers

- 3.1.4 OEMs

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Technology & innovation landscape

- 3.5 Key news & initiatives

- 3.6 Regulatory landscape

- 3.7 Impact forces

- 3.7.1 Growth drivers

- 3.7.1.1 Rising vehicle production and sales

- 3.7.1.2 Advancements in starter motor technology

- 3.7.1.3 Growth in electric and hybrid vehicles

- 3.7.1.4 Increased focus on fuel efficiency and emissions control

- 3.7.2 Industry pitfalls & challenges

- 3.7.2.1 High implementation costs

- 3.7.2.2 Stringent regulations

- 3.7.1 Growth drivers

- 3.8 Growth potential analysis

- 3.9 Porter’s analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Starter Motor, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 Electric starter motor

- 5.3 Pneumatic starter motor

- 5.4 Hydraulic starter motor

- 5.5 Others

Chapter 6 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 Passenger car

- 6.3 Commercial vehicle

Chapter 7 Market Estimates & Forecast, By Power Rating, 2021 - 2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 Below 1.5 kW

- 7.3 1.5–2.5 kW

- 7.4 Above 2.5 kW

Chapter 8 Market Estimates & Forecast, By Sales Channel, 2021 - 2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 OEM

- 8.3 Aftermarket

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Russia

- 9.3.7 Nordics

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 ANZ

- 9.4.6 Southeast Asia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 South Africa

- 9.6.3 Saudi Arabia

Chapter 10 Company Profiles

- 10.1 BorgWarner Inc.

- 10.2 Bosch

- 10.3 Delco Remy

- 10.4 DENSO

- 10.5 Dongfeng Motor Parts and Components Group Co., Ltd.

- 10.6 GDST Auto Parts

- 10.7 Hella KGaA Hueck & Co.

- 10.8 Hitachi Automotive Systems

- 10.9 Lucas Electrical

- 10.10 Magneti Marelli

- 10.11 MITSUBA Corporation

- 10.12 Mitsubishi Electric Corporation

- 10.13 Nikko Electric Industry Co., Ltd.

- 10.14 Prestolite Electric

- 10.15 Remy International

- 10.16 Sawafuji Electric Co., Ltd.

- 10.17 TYK Automotive Electric Co., Ltd.

- 10.18 Unitech Automotive Electrical Appliance Co., Ltd.

- 10.19 Valeo

- 10.20 WAI Global