超音波メスの市場機会、成長促進要因、産業動向分析、2025年~2034年予測

Ultrasonic Scalpel Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 135 Pages

- 納期

- 2~3営業日

- 商品コード

- 1664820

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

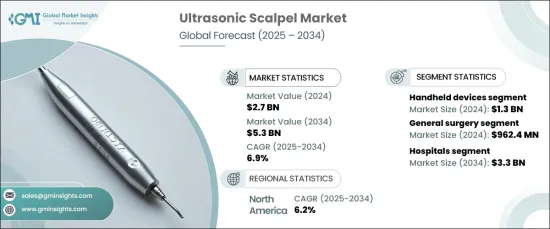

世界の超音波メス市場は、2024年に27億米ドルとなり、2025年から2034年にかけて6.9%のCAGRで堅調に拡大すると予測されています。

この顕著な成長は、外来患者処置の需要増加、婦人科および心臓血管外科手術量の増加、ロボット支援手術手技の採用拡大によって後押しされています。

この市場拡大の主な促進要因は、現代ヘルスケアにおけるゴールドスタンダードとなりつつある低侵襲手術(MIS)への世界のシフトです。腹腔鏡手術を含むこれらの手術は、回復時間の短縮、リスクの最小化、患者の転帰の改善といった大きな利点を提供します。超音波メスは、これらの手術に不可欠な道具として登場し、最適な結果を得るために不可欠な、組織の切断と凝固に比類のない精度を提供しています。さらに、外来手術センターの急増により、超音波メスのようなコンパクトで効率的なツールへの需要が高まっています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025年~2034年 |

| 開始金額 | 27億米ドル |

| 予測金額 | 53億米ドル |

| CAGR | 6.9% |

市場は、ハンドヘルドデバイス、ジェネレーター、アクセサリーを含む製品タイプ別に区分されます。なかでもハンドヘルド超音波メスが最も高い収益を上げ、2024年には13億米ドルに達します。これらの器具は、特に低侵襲手術中の狭いスペースでの精密さと制御性から外科医に非常に支持されています。人間工学に基づいたデザインと高性能により、現代の外科手術には欠かせないものとなっています。MISが世界的に普及し続けるにつれて、これらの高度なツールに対する需要は着実に増加すると予想されます。

用途別では、一般外科、整形外科、眼科外科、泌尿器科外科、婦人科外科などのカテゴリーにまたがっています。一般外科が最大の市場シェアを占め、2024年には9億6,240万米ドルの売上を計上しました。このセグメントには、超音波メスが正確性と有効性を確保する上で重要な役割を果たす重要な手術が幅広く含まれており、手術結果を成功に導く上で不可欠なものとなっています。

地域別では、北米が超音波メス市場を独占し、2024年には12億米ドルに達し、予測期間中のCAGRは6.2%と予測されました。同地域の成長を牽引しているのは、慢性的な健康状態の蔓延と高齢化であり、これらが外科的介入の需要を増幅しています。加齢に関連した健康問題に対処するための高度な手術器具に対するニーズの高まりは、北米を主要な成長貢献国として位置づけ、市場拡大を後押しし続けています。

超音波メス市場は、技術の進歩と低侵襲手術への選好の高まりが需要を牽引し、大幅な成長が見込まれています。この動向は、精密性、効率性、患者予後の向上を提供し、現代の外科手術の未来を形作る超音波メスの重要な役割を強調しています。

目次

第1章 調査手法と調査範囲

第2章 エグゼクティブサマリー

第3章 業界洞察

- 産業エコシステム分析

- 業界への影響要因

- 成長促進要因

- 慢性疾患の増加

- 低侵襲手術に対する需要の高まり

- 製品の技術的進歩の高まり

- 業界の潜在的リスク・課題

- 機器の高コストと代替技術の利用可能性

- 成長促進要因

- 成長可能性分析

- 規制状況

- 技術動向

- 今後の市場動向

- バリューチェーン分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業マトリックス分析

- 企業シェア分析

- 主要市場プレーヤーの競合分析

- 競合のポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:製品別、2021年~2034年

- 主要動向

- ハンドヘルド機器

- ジェネレーター

- アクセサリ

第6章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- 一般外科

- 婦人科外科

- 整形外科

- 泌尿器外科

- 眼科手術

- その他の用途

第7章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 病院

- 外来手術センター

- 専門クリニック

- その他のエンドユーザー

第8章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第9章 企業プロファイル

- Anhui Wanyi Science and Technology

- Apollo Technosystems

- Axon Medical Solutions

- Bioventus

- BOWA Medical UK

- Hangzhou Rex Medical Instrument

- HENAN TRADING

- Johnson and Johnson

- Miconvey

- Olympus

- Reach Surgical

- SI Surgical

- Stryker

- Surgnova

- Wuhan BBT Mini-Invasive Medical Tech

目次

The Global Ultrasonic Scalpel Market was valued at USD 2.7 billion in 2024 and is projected to expand at a robust CAGR of 6.9% from 2025 to 2034. This remarkable growth is fueled by rising demand for outpatient procedures, an increasing volume of gynecological and cardiovascular surgeries, and the growing adoption of robotic-assisted surgical techniques.

A key driver of this market expansion is the global shift toward minimally invasive surgeries (MIS), which are becoming the gold standard in modern healthcare. These procedures, including laparoscopic surgeries, offer significant advantages such as reduced recovery times, minimal risks, and improved patient outcomes. Ultrasonic scalpels have emerged as indispensable tools for these surgeries, offering unparalleled precision in tissue cutting and coagulation, essential for achieving optimal results. Moreover, the surge in outpatient surgical centers has amplified the demand for compact and efficient tools like ultrasonic scalpels, which are tailored for high-volume environments requiring quick turnarounds.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.7 Billion |

| Forecast Value | $5.3 Billion |

| CAGR | 6.9% |

The market is segmented by product type, including handheld devices, generators, and accessories. Among these, handheld ultrasonic scalpels generated the highest revenue, reaching USD 1.3 billion in 2024. These devices are highly favored by surgeons for their precision and control, especially in confined spaces during minimally invasive surgeries. Their ergonomic design and high-performance capabilities make them vital for modern surgical practices. As MIS continues to gain traction globally, the demand for these advanced tools is expected to rise steadily.

In terms of application, the market spans categories such as general surgery, orthopedic surgery, ophthalmic surgery, urological surgery, gynecological surgery, and others. General surgery accounted for the largest market share, generating USD 962.4 million in revenue in 2024. This segment encompasses a wide range of essential procedures where ultrasonic scalpels play a critical role in ensuring precision and effectiveness, making them indispensable in achieving successful surgical outcomes.

Regionally, North America dominated the ultrasonic scalpel market, reaching USD 1.2 billion in 2024, with a projected CAGR of 6.2% during the forecast period. The region's growth is driven by the increasing prevalence of chronic health conditions and an aging population, which together amplify the demand for surgical interventions. The rising need for advanced surgical tools to address age-related health issues continues to bolster market expansion, positioning North America as a key growth contributor.

The ultrasonic scalpel market is poised for substantial growth as technological advancements and the rising preference for minimally invasive procedures drive demand. This trend underscores the critical role of ultrasonic scalpels in shaping the future of modern surgical practices, offering precision, efficiency, and enhanced patient outcomes.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence of chronic diseases

- 3.2.1.2 Rise in demand for minimally invasive surgeries

- 3.2.1.3 Growing technological advancements in products

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High costs of devices and availability of alternative technologies

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Technology landscape

- 3.6 Future market trends

- 3.7 Value chain analysis

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Product, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Handheld devices

- 5.3 Generators

- 5.4 Accessories

Chapter 6 Market Estimates and Forecast, By Application, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 General surgery

- 6.3 Gynecological surgery

- 6.4 Orthopedic surgery

- 6.5 Urological surgery

- 6.6 Ophthalmic surgery

- 6.7 Other applications

Chapter 7 Market Estimates and Forecast, By End Use, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 Ambulatory surgery centers

- 7.4 Specialty clinics

- 7.5 Other end users

Chapter 8 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Anhui Wanyi Science and Technology

- 9.2 Apollo Technosystems

- 9.3 Axon Medical Solutions

- 9.4 Bioventus

- 9.5 BOWA Medical UK

- 9.6 Hangzhou Rex Medical Instrument

- 9.7 HENAN TRADING

- 9.8 Johnson and Johnson

- 9.9 Miconvey

- 9.10 Olympus

- 9.11 Reach Surgical

- 9.12 SI Surgical

- 9.13 Stryker

- 9.14 Surgnova

- 9.15 Wuhan BBT Mini-Invasive Medical Tech

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 135 Pages

- 納期

- 2~3営業日