|

市場調査レポート

商品コード

1913471

航空機エンジン市場の機会、成長要因、業界動向分析、および2026年から2035年までの予測Aircraft Engine Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

カスタマイズ可能

|

|||||||

| 航空機エンジン市場の機会、成長要因、業界動向分析、および2026年から2035年までの予測 |

|

出版日: 2025年12月18日

発行: Global Market Insights Inc.

ページ情報: 英文 170 Pages

納期: 2~3営業日

|

概要

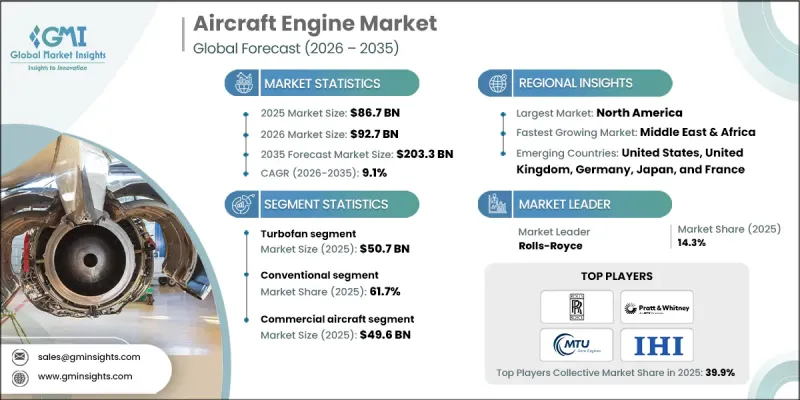

世界の航空機エンジン市場は、2025年に867億米ドルと評価され、2035年までにCAGR 9.1%で成長し、2,033億米ドルに達すると予測されています。

市場拡大の主な要因は、世界の旅客輸送量の増加、航空機の稼働率上昇、そして先進的な推進システムへの需要拡大です。航空会社は機体更新プログラムを優先しており、これが現代的なエンジンと長期メンテナンスソリューションへの需要を直接的に増加させています。同時に、次世代航空技術への投資拡大とアフターマーケット・メンテナンスサービスの持続的成長が収益基盤を強化しています。防衛航空分野のアップグレードも、政府による高性能航空機プラットフォームへの投資に伴い、市場の強さに寄与しています。効率性、信頼性、持続可能性が民間・軍用航空の両分野で中核的な優先事項となる中、世界の継続的なイノベーションと長期エンジン調達プログラムが促進され、市場全体の展望は引き続き良好です。

| 市場範囲 | |

|---|---|

| 開始年 | 2025年 |

| 予測年度 | 2026-2035 |

| 開始時価値 | 867億米ドル |

| 予測金額 | 2,033億米ドル |

| CAGR | 9.1% |

航空旅客数の増加に伴い、航空機の運航回数が増加し、エンジン使用サイクルが加速しているため、航空機エンジンの需要は引き続き上昇傾向にあります。航空会社は機材の拡充に伴い、燃費効率と運用信頼性が向上した次世代エンジンを必要としており、老朽化した航空機の更新もエンジン販売とアフターマーケット需要をさらに刺激しています。並行して、防衛機関がより高性能な航空機プラットフォームへ移行する中、軍事航空の近代化プログラムが市場成長を後押ししています。これらの近代化努力には、厳しい運用条件下でも安定した性能を発揮しつつ、効率性と耐久性を維持するエンジンが求められています。

ターボファンエンジン分野は、民間航空機群における先進推進技術の採用拡大を背景に、2025年には507億米ドルの市場規模を生み出しました。燃料消費量と排出ガスを削減するエンジンへの需要が高まることで、更新サイクルが加速し、ターボファンエンジンの開発・導入への持続的な投資を牽引しています。

従来型エンジンカテゴリーは2025年に61.7%のシェアを占めました。新型航空機設計が低燃費と環境負荷低減を実現し、運用者が費用対効果の高い方法で進化する規制基準に対応できることから、継続的な機体近代化イニシアチブが従来型推進システムへの安定した需要を支えています。

北米航空機エンジン市場は2025年に43.4%のシェアを占めました。航空輸送活動の回復基調と防衛支出の持続が、新型エンジンおよび推進システムアップグレードの需要を牽引しています。機体更新プログラムと長期的な軍事投資が、同地域の市場優位性を引き続き支えています。

よくあるご質問

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- コスト構造

- 各段階における付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- 航空需要の増加

- エンジン効率における技術的進歩

- エンジンアフターマーケット及びMROサービスの拡大

- 新興航空機技術への投資拡大

- 防衛および軍用航空機の近代化推進

- 課題と困難

- 高い研究開発(R&D)コスト

- サプライチェーン及び製造上の制約

- 機会

- ハイブリッド電気および持続可能な推進技術の成長

- エンジンアフターマーケットおよび予知保全サービスの拡大

- 促進要因

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- ポーター分析

- PESTEL分析

- 技術・イノベーション動向

- 現在の技術動向

- 新興技術

- 新興ビジネスモデル

- コンプライアンス要件

- 防衛予算分析

- 世界の防衛支出動向

- 地域別防衛予算配分

- 北米

- 欧州

- アジア太平洋地域

- 中東・アフリカ

- ラテンアメリカ

- 主要防衛近代化プログラム

- 予算予測(2026-2035)

- 業界成長への影響

- 国別防衛予算

- 分野別防衛予算配分

- 人員

- 運用・保守

- 調達

- 研究開発・試験評価

- インフラストラクチャーおよび建設

- 技術とイノベーション

- 持続可能性への取り組み

- サプライチェーンのレジリエンス

- 地政学的分析

- 労働力分析

- デジタルトランスフォーメーション

- 合併・買収および戦略的提携の動向

- リスク評価と管理

- 主要契約授与(2022-2025)

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 地域別

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- 市場集中度分析

- 地域別

- 主要企業の競合ベンチマーキング

- 製品ポートフォリオ比較

- 製品ラインの広さ

- 技術

- イノベーション

- 地域別事業展開比較

- 世界な事業展開分析

- サービスネットワークのカバー率

- 地域別市場浸透率

- 競合ポジショニングマトリックス

- リーダー企業

- 課題者

- フォロワー

- ニッチプレイヤー

- 戦略的展望マトリックス

- 製品ポートフォリオ比較

- 主な発展, 2022-2025

- 合併・買収

- 提携および協力関係

- 技術的進歩

- 拡大および投資戦略

- サステナビリティへの取り組み

- デジタルトランスフォーメーションの取り組み

- 新興/スタートアップ競合の動向

第5章 市場推計・予測:タイプ別、2022-2035

- ターボプロップ

- ターボファン

- ターボシャフト

- ピストンエンジン

第6章 市場推計・予測:コンポーネント別、2022-2035

- タービン

- コンプレッサー

- ギアボックス

- 排気システム

- 燃料システム

- その他

第7章 市場推計・予測:技術別、2022-2035

- 従来型

- ハイブリッド

第8章 市場推計・予測:用途別、2022-2035

- 民間航空機

- ナローボディ

- ワイドボディ

- リージョナルジェット

- ターボプロップ/ヘリコプター

- 軍用機

- 戦闘機

- 輸送機

- 特殊任務航空機

- 軍用ヘリコプター

- 無人航空機

第9章 市場推計・予測:地域別、2022-2035

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

第10章 企業プロファイル

- 世界の主要企業

- General Electric Company

- Rolls-Royce

- Pratt &Whitney(RTX)

- Safran Group

- 地域別主要企業

- 北米

- Engine Alliance

- Textron Inc.

- 欧州

- MTU Aero Engines AG

- ITP Aero

- アジア太平洋地域

- IHI Corporation

- Mitsubishi Heavy Industries Aero Engines, Ltd.

- 北米

- ニッチ/ディスラプター

- CFM International

- Enjet Aero