商用航空機用エンジン:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)

Commercial Aircraft Engines - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 90 Pages

- 納期

- 2~3営業日

- 商品コード

- 1690733

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

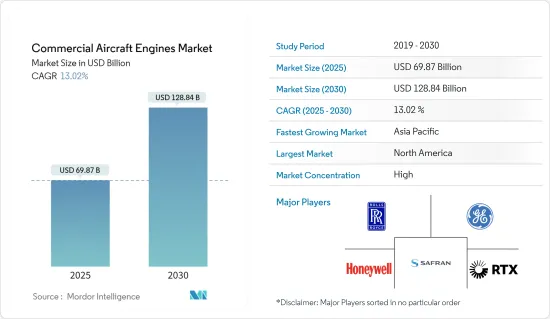

商用航空機用エンジンの市場規模は2025年に698億7,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは13.02%で、2030年には1,288億4,000万米ドルに達すると予測されます。

世界の航空旅客輸送量の増加が新型商用航空機の需要増につながり、商用航空機エンジン市場の成長を牽引しています。アジア太平洋および中東・アフリカの各都市における新しい中型・小型空港の開発は、新しい路線に就航するための新しい航空機の需要を促進し、それによって商用航空機エンジン市場の関連成長を牽引しています。

技術革新は、この市場の成長を大きく後押ししています。新型モデルの開発により、軽量化、ノイズフットプリントの低減、排出ガスの低減、高推力化、メンテナンス作業の軽減などが実現されています。しかし、先進エンジンの研究開発サイクルが不安定なため、世界の経済格差の影響を受けやすく、市場は景気変動に悩まされています。将来的には、軽量化、省スペース化、高出力化など、バッテリー技術の開発によって完全電動化が達成されるまで、ハイブリッド推進エンジンが開発・採用されることになると思われます。

商用航空機用エンジン市場動向

予測期間中、ワイドボディ航空機セグメントが最も高いCAGRで成長すると予測される

ツインアイル航空機と呼ばれるワイドボディ航空機は、7席以上の座席を横並びにして2つの乗客通路を確保できる幅の胴体を持つ旅客機です。一般的な胴体の直径は5~6m(16~20フィート)です。ボーイングB777X型機やエアバスA350型機は、世界各地で就航しているワイドボディ機の一例です。

航空会社はワイドボディ機を貨物輸送に使用しています。こうした航空機の高い需要は2023年まで続くと予想されました。開発メーカーはこの需要に応えるため、先進的なエンジンを開発しました。例えば、2023年2月、タタ・サンズ傘下のエア・インディアは、GEエアロスペースと、40基のGEnx-1Bエンジンと20基のGE9Xエンジンの調達契約と、複数年にわたるTrueChoiceエンジン・サービス契約を締結しました。この契約は、同航空会社がボーイングB777X型機10機とボーイングB787型機20機を確定発注したことと協調して締結されました。

エミレーツ航空は2023年11月、ボーイングB777X型機に搭載する202基のGE9X型エンジンの発注を発表しました。この発注には、長期サービス契約も含まれています。これにより、エミレーツ航空はGE9Xエンジンを合計460基発注したことになります。2022年5月、オーストラリアの航空会社カンタス航空は、ロールスロイス・トレントXWB-97を搭載したA350-1000型機12機の契約にコミットすることを発表しました。この航空機は、ロンドンやニューヨークとオーストラリア東海岸の都市シドニーやメルボルンを直行便で結ぶ、世界最長の商業直行便の運航を目指す同航空会社の目標をサポートするものです。これは、同業航空会社との航空機エンジン調達パートナーシップにつながります。焦点は、大陸間移動に最適なワイドボディ機です。航空機エンジンメーカーによるワイドボディ航空機向けの複数のパートナーシップとイノベーションにより、このセグメントは予測期間中に大きく成長すると予想されます。

アジア太平洋地域は予測期間中に顕著な成長を示すだろう

アジア太平洋地域は予測期間中に最も高い成長を示すと予測されます。航空会社の機体拡大計画や貨物サービスの増加により、新しい旅客機や貨物機の調達が加速しており、予測期間中、航空機エンジン市場に好影響を与えると思われます。

現在、最新のC919を含め、中国で生産される商用航空機には外国製エンジンが搭載されています。しかし、同国は、高度な技術の海外供給源への依存を削減するため、国産代替エンジンの開発を試みています。中国はCJ1000の開発を進めています。CJ1000は、今後3年から5年の間に、国産のナローボディ機C919の動力源として設計されたターボファンジェットエンジンです。

2023年6月、チャイナエアラインは、増加するボーイング787ドリームライナー民間ジェット機の動力源として、ゼネラル・エレクトリック(GE)エアロスペース社から17基のGEnx-1Bエンジンと予備品を受注しました。同航空は現在、旅客機66機と貨物機21機を含む87機を運航しています。

インド民間航空局(DGCA)の報告によると、2022年、インドの総旅客数は1億500万人以上に達します。国際航空運送協会(IATA)によると、インドは今後10年間で、2030年までに中国と米国を抜いて世界第3位の航空旅客市場になると予想されています。そのため、航空会社は保有機材を拡大し、拡大する市場機会に対応するため、大規模な調達計画を進めています。2023年6月、インディゴはエアバスA320ファミリーを500機発注しました。このインディゴのオーダーブックは、A320NEO、A321NEO、A321XLRの混合機で構成されています。このような航空会社や航空機運航会社の航空機近代化計画は、予測期間中、航空機エンジン市場の商用セグメントの成長を促進すると予想されます。

商用航空機エンジン産業の概要

商用航空機エンジン市場は統合されており、ゼネラル・エレクトリック社、サフランSA、プラット・アンド・ホイットニー社(RTX社)、ロールス・ロイスPLC、ハネウェル・インターナショナル社などの大手企業が市場を独占しています。商用航空機用エンジン市場では、航空機の軽量化と低燃費化を実現する新技術を生み出すための共同開発や共同開発プログラムが行われています。世界の商用航空機エンジン・メーカーはまた、低コストの労働力が利用可能であり、航空産業が成長していることから、アジア太平洋地域などの製造エコシステムに投資しています。市場プレイヤーの主な収益創出戦略は、航空機メーカーからエンジンとエンジンMROサービスの契約と注文を獲得することです。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 市場抑制要因

- ポーターのファイブフォース分析

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- 航空機タイプ

- ナローボディ機

- ワイドボディ機

- リージョナル機

- エンジンタイプ

- ターボファン

- ターボプロップ

- 地域

- 北米

- 米国

- カナダ

- 欧州

- 英国

- フランス

- ドイツ

- ロシア

- スペイン

- その他欧州

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- その他アジア太平洋地域

- ラテンアメリカ

- メキシコ

- ブラジル

- アルゼンチン

- その他ラテンアメリカ

- 中東・アフリカ

- アラブ首長国連邦

- サウジアラビア

- その他中東とアフリカ

- 北米

第6章 競合情勢

- ベンダー市場シェア

- 企業プロファイル

- The General Electric Company

- Safran SA

- Rolls-Royce PLC

- Honeywell International Inc.

- United Engine Corporation(Rostec)

- Pratt & Whitney(RTX Corporation)

- MTU Aero Engines AG

- IHI Corporation

- CFM International

- Williams International Co. LLC

- Mitsubishi Heavy Industries Ltd

- Aviation Industry Corporation of China

- IAG Aero Group

第7章 市場機会と今後の動向

目次

The Commercial Aircraft Engines Market size is estimated at USD 69.87 billion in 2025, and is expected to reach USD 128.84 billion by 2030, at a CAGR of 13.02% during the forecast period (2025-2030).

The rise in global air passenger traffic is leading to a growth in the demand for new commercial aircraft, driving the growth of the commercial aircraft engines market. The development of new medium- and small-sized airports in cities across Asia-Pacific and Middle East and Africa is propelling the demand for new aircraft to serve the new routes, thereby driving related growth of the commercial aircraft engines market.

Technological innovations are significantly fueling the growth of the market studied. The development of new models results in weight reduction, fewer noise footprints, fewer emissions, high thrust, reduction in maintenance operations, etc. However, the market is marred by economic fluctuations as the tenuous R&D cycle of advanced engines renders the players vulnerable to global economic disparities. In the future, hybrid propulsion engines will be developed and adopted until full electrification is achieved through the development of battery technology in areas such as weight reduction, less space requirement, and high power.

Commercial Aircraft Engines Market Trends

Wide-Body Aircraft Segment is Anticipated to Grow with the Highest CAGR During the Forecast Period

A wide-body aircraft, called twin-aisle aircraft, is an airliner with a fuselage wide enough to accommodate two passenger aisles with seven or more seats abreast. The typical fuselage diameter is 5 to 6 m (16 to 20 ft). Boeing B777X and Airbus A350 are examples of wide-body aircraft in service across various world geographies.

Airlines use wide-body aircraft to ferry goods. The high demand for such aircraft was expected to continue until 2023. Manufacturers developed advanced engines to meet the demand. For instance, in February 2023, Air India, a part of Tata Sons, signed a procurement contract for 40 GEnx-1B and 20 GE9X engines and a multi-year TrueChoice engine services agreement with GE Aerospace. The deal was signed in coordination with the airline's firm order for 10 Boeing B777X and 20 Boeing B787 aircraft.

In November 2023, Emirates announced an order for 202 GE9X engines to power its upcoming fleet of Boeing B777X aircraft. The order also includes a long-term services agreement. This brings Emirates' total order for GE9X engines to 460. In May 2022, the Australian carrier Qantas announced its commitment to a deal for 12 Rolls Royce Trent XWB-97 powered A350-1000 aircraft that will support the airline's aim to operate the world's longest commercial non-stop flights, allowing passengers to fly direct between London and New York to the Australian east coast cities of Sydney and Melbourne. This leads to aircraft engine procurement partnerships with airlines in the industry. The focus is on wide-body aircraft that are ideal for intercontinental travel. With multiple partnerships and innovations by aircraft engine manufacturers for wide-body aircraft, this segment is expected to grow significantly during the forecast period.

Asia Pacific Will Showcase Remarkable Growth During the Forecast Period

Asia Pacific is projected to show the highest growth during the forecast period. Fleet expansion plans of airlines and increasing cargo services are accelerating the procurement of new passenger and cargo aircraft, which will possess a positive stance on the aircraft engine market during the forecast period.

Currently, the commercial aircraft produced in China, including the latest C919, are equipped with foreign engines. However, the country has been trying to develop a home-grown alternative as it seeks to cut its dependence on foreign sources of sophisticated technology. China is progressing with the development of CJ1000, a turbofan jet engine designed to power the homemade C919 narrow-body aircraft in the next three to five years.

In June 2023, China Airlines made an order for 17 GEnx-1B engines and spares from General Electric (GE) Aerospace to power its growing fleet of Boeing 787 Dreamliner commercial jets. The Airline currently operates a fleet of 87 aircraft, including 66 passenger jets and 21 freighters.

According to a report by the Indian Directorate General of Civil Aviation (DGCA), in 2022, India's total air passenger traffic reached more than 105 million passengers. According to the International Air Transport Association (IATA), India is expected to overtake China and the United States as the world's third-largest air passenger market in the next ten years by 2030. Hence, the airlines are undertaking massive procurement plans to expand their fleet and address the growing market opportunity. On this note, in June 2023, IndiGo ordered 500 Airbus A320 Family aircraft. This IndiGo order-book comprises a mix of A320NEO, A321NEO and A321XLR aircraft. Such fleet modernization plans of the airlines and aircraft operators are expected to drive the growth of the commercial segment of the aircraft engines market during the forecast period.

Commercial Aircraft Engines Industry Overview

The commercial aircraft engines market is consolidated, with major players, such as The General Electric Company, Safran SA, Pratt & Whitney (RTX Corporation), Rolls-Royce PLC, and Honeywell International Inc., dominating the market. The commercial aircraft engine market is witnessing collaborations and joint development programs for creating new technologies for lighter and fuel-efficient aircraft. Global commercial aircraft engine manufacturers are also investing in the manufacturing ecosystems in regions such as Asia-Pacific, owing to the availability of low-cost labor and the growing aviation industry. The main revenue generation strategy of market players is winning contracts and orders from aircraft manufacturers for engines and engine MRO services.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Buyers/Consumers

- 4.4.2 Bargaining Power of Suppliers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Aircraft Type

- 5.1.1 Narrow-body Aircraft

- 5.1.2 Wide-body Aircraft

- 5.1.3 Regional Aircraft

- 5.2 Engine Type

- 5.2.1 Turbofan

- 5.2.2 Turboprop

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.2 Europe

- 5.3.2.1 United Kingdom

- 5.3.2.2 France

- 5.3.2.3 Germany

- 5.3.2.4 Russia

- 5.3.2.5 Spain

- 5.3.2.6 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 India

- 5.3.3.3 Japan

- 5.3.3.4 South Korea

- 5.3.3.5 Rest of Asia-Pacific

- 5.3.4 Latin America

- 5.3.4.1 Mexico

- 5.3.4.2 Brazil

- 5.3.4.3 Argentina

- 5.3.4.4 Rest of Latin America

- 5.3.5 Middle East and Africa

- 5.3.5.1 United Arab Emirates

- 5.3.5.2 Saudi Arabia

- 5.3.5.3 Rest of Middle East and Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles

- 6.2.1 The General Electric Company

- 6.2.2 Safran SA

- 6.2.3 Rolls-Royce PLC

- 6.2.4 Honeywell International Inc.

- 6.2.5 United Engine Corporation (Rostec)

- 6.2.6 Pratt & Whitney (RTX Corporation)

- 6.2.7 MTU Aero Engines AG

- 6.2.8 IHI Corporation

- 6.2.9 CFM International

- 6.2.10 Williams International Co. LLC

- 6.2.11 Mitsubishi Heavy Industries Ltd

- 6.2.12 Aviation Industry Corporation of China

- 6.2.13 IAG Aero Group

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 90 Pages

- 納期

- 2~3営業日