|

市場調査レポート

商品コード

1871321

導電性ポリマー市場の機会、成長要因、業界動向分析、および2025年から2034年までの予測Conductive Polymers Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 導電性ポリマー市場の機会、成長要因、業界動向分析、および2025年から2034年までの予測 |

|

出版日: 2025年10月30日

発行: Global Market Insights Inc.

ページ情報: 英文 190 Pages

納期: 2~3営業日

|

概要

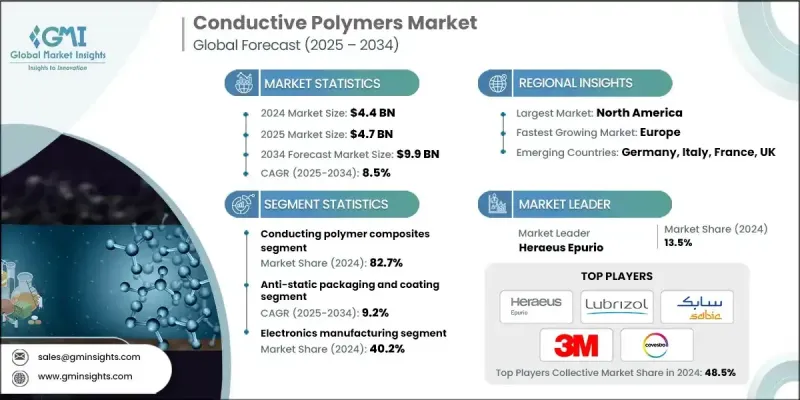

世界の導電性ポリマー市場は、2024年に44億米ドルと評価され、2034年までにCAGR8.5%で成長し、99億米ドルに達すると予測されています。

この市場の急成長は、電気伝導性と軽量・柔軟性を兼ね備えた先進材料を求める複数産業における需要の高まりに牽引されています。導電性ポリマーは、革新と持続可能性を追求する産業にとって最も汎用性の高いソリューションの一つとして台頭しています。機械的柔軟性と効率的な導電性を同時に提供できる特性により、自動車、医療、消費財分野での応用において不可欠な存在となっています。環境意識の高まりと、リサイクル可能で無毒な材料への選好の増加が、その採用をさらに加速させています。市場は、センサー、エネルギー貯蔵、スマートテキスタイルなどの次世代用途における可能性を探求する企業と共に進化を続けております。持続可能な素材への広範な移行と、エレクトロニクスおよびグリーン製造の急速な進歩が相まって、今後10年間にわたり導電性ポリマーの需要を牽引し続けると予想されます。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測期間 | 2025-2034 |

| 開始時価値 | 44億米ドル |

| 予測金額 | 99億米ドル |

| CAGR | 8.5% |

医療分野では、生体適合性と適応性から、導電性ポリマーがバイオエレクトロニクス、センサー、医療機器においてますます活用されています。自動車製造における役割の拡大は、軽量でありながら耐久性に優れる特性によるもので、これにより燃費効率の向上と排出ガスの削減が図られています。これらの材料は、持続可能性に焦点を当てた産業で支持を集めており、地球環境目標に沿うとともに、柔軟で効率的かつリサイクル可能な部品の製造を可能にします。

2024年時点で、固有導電性ポリマー分野は17.3%のシェアを占めており、技術的な成熟度の向上と産業用途の拡大が顕著です。これらのポリマーは、先端電子機器、電磁波干渉(EMI)シールド、帯電防止コーティングなどの分野で広く活用されています。継続的な技術革新と研究開発により、導電性、安定性、耐久性が向上しており、従来の導電性材料に代わる優れた選択肢としての地位をさらに強化しています。

2024年における帯電防止包装・コーティング分野のシェアは27.8%を占め、CAGR 9.2%で成長しています。様々な産業分野における電子部品の統合が進む中、効果的な静電気対策ソリューションの必要性が高まっています。導電性ポリマーはコスト効率に優れ軽量な選択肢を提供するため、世界中のメーカーから選ばれています。同様に、コンデンサへの導電性ポリマーの採用も、優れた電気伝導性、化学的安定性、信頼性により急速に拡大しています。民生用・産業用を問わず、コンパクトで高性能な電子機器への需要増加が、この分野の革新を継続的に促進しています。

北米の導電性ポリマー市場は2024年に43.3%のシェアを占め、2034年までCAGR 8.6%で成長が見込まれます。同地域の成長は、技術進歩、強固な産業基盤、医療・自動車・航空宇宙・電子機器分野における導電性材料の広範な利用によって牽引されています。軽量で柔軟性があり、持続可能な材料への注目が高まっており、特に米国とカナダでは、スマートデバイスや環境に優しい製造技術における革新が進んでいることから、需要が加速しています。

世界の導電性ポリマー市場の主要企業には、デュポン・デ・ネムール、SABIC、RTPカンパニー、ウェストレイク・プラスチックス、ルブリゾール・コーポレーション、ヘンケルAG、ヘレウス・エプリオ、3M、セラニーズ・コーポレーション、ケメット・コーポレーション、アグファ・ゲバート、コベストロAG、ケナー・マテリアル&システム、プレミックスOy、アビエント・コーポレーションなどが挙げられます。導電性ポリマー市場の主要企業は、イノベーション、パートナーシップ、生産能力の拡大を通じて市場での存在感を高めるための戦略的施策を実施しております。多くの企業が、導電性ポリマーの電気的性能、加工性、環境適合性を向上させるため、研究開発に多額の投資を行っております。電子機器、自動車、医療機器メーカーとの協業により、先進的な用途向けにカスタマイズされた材料の共同開発が可能となっております。また、主要なグローバル市場における需要拡大に対応するため、生産施設の拡張や地域別流通ネットワークの構築も進めております。持続可能性は依然として重要な焦点であり、環境に配慮した規制に適合するため、リサイクル可能なバイオベースの導電性材料の開発が進められております。

よくあるご質問

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- 各段階における付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク&課題

- 市場機会

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- ポーター分析

- PESTEL分析

- 価格動向

- 地域別

- 製品カテゴリー別

- 将来の市場動向

- 技術とイノベーションの情勢

- 現在の技術動向

- 新興技術

- 特許情勢

- 貿易統計(HSコード)(注:貿易統計は主要国のみ提供されます)

- 主要輸入国

- 主要輸出国

- 持続可能性と環境面

- 持続可能な取り組み

- 廃棄物削減戦略

- 生産におけるエネルギー効率

- 環境に配慮した取り組み

- カーボンフットプリントへの配慮

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 地域別

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ地域

- 地域別

- 企業マトリクス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併・買収

- 提携・協業

- 新製品の発売

- 拡大計画

第5章 市場推計・予測:伝導メカニズム別、2021-2034

- 主要動向

- 導電性ポリマー複合材料

- ABS

- ポリカーボネート

- PVC

- PP

- ナイロン

- その他

- 固有導電性ポリマー

- ポリアニリン(PANI)

- ポリピロール(PPy)

- ポリフェニレンビニレン(PPV)

- PEDOT

- その他

第6章 市場推計・予測:用途別、2021-2034

- 主要動向

- 静電気防止包装・コーティング

- コンデンサ

- アクチュエータ及びセンサー

- 電池

- 太陽電池

- エレクトロルミネッセンス

- プリント基板

- その他

第7章 市場推計・予測:最終用途別、2021-2034

- 主要動向

- 電子機器製造

- ヘルスケア・ライフサイエンス

- 自動車・航空宇宙

- 化学・材料

- エネルギー・公益事業

- その他

第8章 市場推計・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- その他欧州地域

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- その他アジア太平洋地域

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- その他ラテンアメリカ地域

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

- その他中東・アフリカ地域

第9章 企業プロファイル

- 3M

- Agfa Gevaert

- Avient Corporation

- Celanese Corporation

- Covestro AG

- DuPont de Nemours

- Henkel Ag

- Heraeus Epurio

- KEMET Corporation

- Kenner Material &System

- Premix Oy

- RTP Company

- SABIC

- The Lubrizol Corporation

- Westlake Plastics