|

市場調査レポート

商品コード

1876783

再生金属市場の機会、成長要因、業界動向分析、および2025年から2034年までの予測Recycled Metal Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 再生金属市場の機会、成長要因、業界動向分析、および2025年から2034年までの予測 |

|

出版日: 2025年11月06日

発行: Global Market Insights Inc.

ページ情報: 英文 210 Pages

納期: 2~3営業日

|

概要

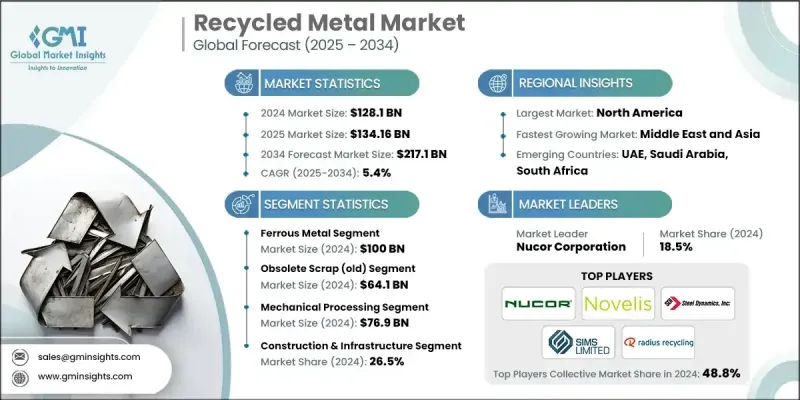

世界の再生金属市場は、2024年に1,281億米ドルと評価され、2034年までにCAGR5.4%で成長し、2,171億米ドルに達すると予測されています。

本市場は、使用済み金属の回収・加工・再利用を通じて新たな原料を創出し、新規鉱石の採掘需要を削減することに焦点を当てています。自動車、建築物、電子機器、包装材などの使用済み製品から回収される金属は、環境持続可能性、省エネルギー、温室効果ガス削減において極めて重要な役割を果たします。アルミニウム、鉄鋼、銅、亜鉛は品質を損なうことなく繰り返しリサイクル可能であり、循環型経済の主要な推進力となっています。AIによる選別、ロボット技術、センサーベースの分離、低排出炉などの技術進歩により、回収効率は大幅に向上しています。デジタル追跡やブロックチェーン技術の応用が拡大し、リサイクル金属の透明性、トレーサビリティ、真正性が確保されることで、製造業者や消費者はサプライチェーンの健全性と持続可能な調達慣行を検証できるようになっています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年度 | 2025-2034 |

| 開始時価値 | 1,281億米ドル |

| 予測金額 | 2,171億米ドル |

| CAGR | 5.4% |

機械加工セグメントは、スクラップ金属を効率的に破砕・切断し再利用可能な状態に加工するため、2024年には769億米ドルの市場規模を生み出しました。次いで熱処理セグメントが続き、高温での溶解・分離により複雑なスクラップや汚染されたスクラップから金属を回収し、工業用途に適した高純度の製品を生産する点で優れています。

建設・インフラ分野は2024年に26.5%のシェアを占め、建築・土木プロジェクトにおける鉄鋼・アルミニウムの需要拡大が牽引しました。自動車・輸送分野では電気自動車や軽量車両の普及により急成長を遂げています。産業機械、電子機器、電気設備、包装、エネルギー事業においても、回路・配線から再生可能エネルギーシステムに至るまで、コスト効率と持続可能性を両立させるため、リサイクル金属への依存度が高まっています。

米国リサイクル金属市場は、自動車および建設セクターからの需要増加により、2024年に266億米ドルに達しました。北米では、電気自動車への移行、エネルギー効率の高いインフラ、持続可能な製造手法が成長を牽引しています。カナダは循環型経済イニシアチブを支援するため、産業廃棄物や廃金属からの回収に投資しています。

世界の再生金属市場で主要な企業には、Metaloop GmbH、Redwood Materials Inc.、Kuusakoski Group、Steel Dynamics Inc.、Radius Recycling Inc.、Sims Metal Management Limited、Lohum Cleantech Pvt Ltd、Ace Green Recycling Inc.、Nucor Corporation、European Metal Recycling Limited、Asahi Holdings Inc.、Befesa S.A.バックス・エナジーズ・プライベート・リミテッド、GFGアライアンス、ヘンゼル・リサイクル社、ノベリス社、スクラップビーズ社、ソーターラ・テクノロジーズ社、トリプルMメタル社などが挙げられます。リサイクル金属市場の企業は、自らの立場を強化するため、処理能力の拡大、高度な選別・製錬技術への投資、効率向上のための自動化導入など、複数の戦略を採用しております。また、サプライチェーン能力の強化と原材料源の確保を目的として、戦略的提携や合弁事業の形成も進めております。多くのプレイヤーは、環境意識の高い顧客にアピールするため、デジタル化、ブロックチェーンベースのトレーサビリティ、持続可能性認証に注力しております。

よくあるご質問

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- 各段階における付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- 拡大する産業活動および建設活動

- リサイクルプロセスにおける技術的進歩

- 自動車および電子機器分野からの需要増加

- 促進要因

- 業界の潜在的リスク&課題

- 変動するスクラップ金属価格

- 効率的な収集・分別システムの不足

- 市場機会

- デジタル技術と自動化の統合

- グリーン産業における二次原料の需要増加

- 製品革新と再生金属ベースの製造

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- ポーター分析

- PESTEL分析

- 技術とイノベーションの動向

- 現在の技術動向

- 新興技術

- 価格動向

- 地域別

- 金属タイプ別

- 将来の市場動向

- 技術とイノベーションの動向

- 現在の技術動向

- 新興技術

- 特許状況

- 貿易統計(HSコード)(注:貿易統計は主要国のみ提供されます)

- 主要輸入国

- 主要輸出国

- 持続可能性と環境的側面

- 持続可能な取り組み

- 廃棄物削減戦略

- 生産におけるエネルギー効率

- 環境に配慮した取り組み

- カーボンフットプリントへの配慮

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 地域別

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ地域

- 地域別

- 企業マトリクス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併・買収

- 提携・協業

- 新製品の発売

- 事業拡大計画

第5章 市場推計・予測:金属の種類別、2021-2034

- 主要動向

- 鉄金属

- 鉄スクラップ

- 鉄スクラップ

- 鋳鉄

- 非鉄金属

- アルミニウム

- 一次アルミニウムスクラップ

- 二次アルミ合金

- 銅

- 銅線・ケーブル

- 銅管・パイプ

- 鉛

- バッテリー用鉛

- 鉛板

- 貴金属

- 金回収

- 銀の回収

- 白金族金属

- 特殊金属

- チタン

- ニッケル

- レアアース元素

- アルミニウム

第6章 市場推計・予測:スクラップ源別、2021-2034

- 主要動向

- 産業スクラップ(即時スクラップ)

- 製造廃棄物フロー

- 加工施設の製品別

- 陳腐化したスクラップ(オールドスクラップ)

- 使用済み自動車

- 解体された建物・インフラ

- 電子廃棄物(E-waste)

- 家電製品・消費財

- 家庭スクラップ(新規スクラップ)

- 製鉄所返却品

- 鋳造返却品

第7章 市場推計・予測:処理方法別、2021-2034

- 主要動向

- 機械的処理

- シュレッディング及びサイズ縮小

- 磁気分離

- 密度分離

- 熱処理

- 電気アーク炉(EAF)

- 誘導炉

- 火法処理

- 化学処理

- 湿式冶金抽出

- 電気精錬

- 溶媒抽出

- 高度な選別技術

- AI搭載光学選別

- センサーベースの分離

- レーザー誘起破壊分光法(LIBS)

第8章 市場推計・予測:最終用途産業別、2021-2034

- 主要動向

- 建設・インフラ

- 構造用鋼材の応用分野

- 補強材

- 政府インフラプロジェクト

- 自動車・輸送機器

- ボディ・フレーム部品

- エンジン・駆動系部品

- 電気自動車部品

- 製造・産業機械

- 重機

- 産業用工具・部品

- 電気・電子機器

- 配線・導体

- 電子部品

- 電池応用

- 包装・容器

- 食品・飲料包装

- 産業用包装

- エネルギー・公益事業

- 発電設備

- 再生可能エネルギーインフラ

- 送電・配電システム

- 航空宇宙・防衛

- 航空機部品

- 防衛用途

- 消費財・家電製品

- 化学・プロセス産業

- 船舶・造船

- その他

第9章 市場推計・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- その他欧州地域

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- その他アジア太平洋地域

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- その他ラテンアメリカ地域

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

- その他中東・アフリカ地域

第10章 企業プロファイル

- Ace Green Recycling Inc.

- Asahi Holdings Inc.

- Batx Energies Private Limited

- Befesa S.A.

- ヨーロピアン・メタル・リサイクリング株式会社

- GFG Alliance

- Hensel Recycling GmbH

- Kuusakoski Group

- Lohum Cleantech Pvt Ltd

- Metaloop GmbH

- Nucor Corporation

- Novelis Inc

- Redwood Materials Inc.

- ScrapBees GmbH

- Radius Recycling Inc.

- Sims Metal Management Limited

- Sortera Technologies Inc

- Steel Dynamics Inc.

- Triple M Metal LP