|

市場調査レポート

商品コード

1801897

芝生・庭用機器の市場機会と促進要因、産業動向分析、2025~2034年の予測Lawn and Garden Equipment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 芝生・庭用機器の市場機会と促進要因、産業動向分析、2025~2034年の予測 |

|

出版日: 2025年08月07日

発行: Global Market Insights Inc.

ページ情報: 英文 170 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

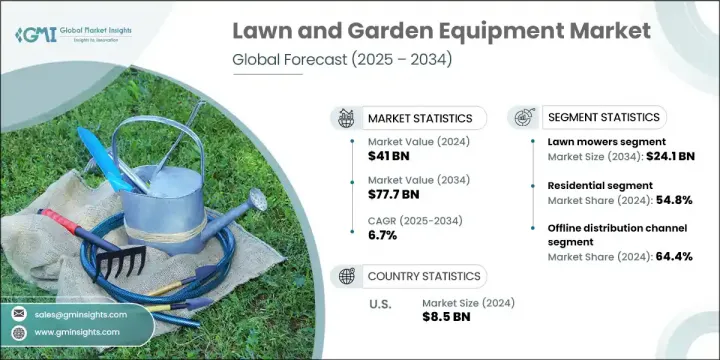

芝生・庭用機器の世界市場規模は、2024年に410億米ドルとなり、CAGR 6.7%で成長し、2034年には777億米ドルに達すると予測されています。

可処分所得の増加と中流階級の人口拡大が、住宅改修と屋外の美観に対する消費者の関心を高めています。住宅所有者はますます自分好みの屋外空間を優先するようになっており、造園用具、スマートガーデニングシステム、効率的な庭の手入れ用機器に対する需要は着実に高まっています。新しい住宅開発、特に郊外や半都市部では、芝生や庭を不可欠な生活空間として扱うことが奨励されています。

この動向は、オンラインアクセスの利便性向上、より容易な資金調達方法、環境にやさしくテクノロジーと一体化した生活を重視する傾向の高まりに支えられ、市場の見通しを形成しています。ユーザーフレンドリーでコネクテッドな機器を好む傾向が強まる中、メーカーはロボット芝刈り機、アプリベースの灌漑システム、インテリジェントなガーデニングツールなどの自動化ソリューションに注力しています。これらの技術革新は、手作業の負担を軽減するだけでなく、ユーザーが正確な制御を実現し、緑地の全体的な機能性を高めることを可能にします。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025年~2034年 |

| 開始金額 | 410億米ドル |

| 予測金額 | 777億米ドル |

| CAGR | 6.7% |

芝刈り機は2024年に123億米ドルを生み出し、2034年には241億米ドルに達すると予測されています。これらのツールは、その機能性、使いやすさ、健康な芝生の維持における重要な役割により、最も利用されている製品カテゴリーであり続けています。一貫した芝刈りは、芝生の最適な健康状態を維持し、周囲の景観を向上させ、住宅所有者に整然とした心地よい屋外環境を提供します。小さな住宅の庭であれ、大きな緑地であれ、芝刈り機は屋外のメンテナンスルーチンに不可欠な要素です。

商業用セグメントは、2025年から2034年にかけてCAGR 7.1%で成長すると予測されています。企業や機関は、都市美化や持続可能性イニシアチブの一環として、造園やグリーンインフラへの投資を増やしています。整備された屋外環境はブランドイメージの向上に役立ち、接客業、企業、公共施設などあらゆる場面で歓迎される環境を提供します。緑地帯を取り入れた都市計画が進むにつれ、より広いスペースを管理するための効率的で費用対効果の高い芝生・庭用機器への需要が高まり続けています。

米国の芝生・庭用機器市場は2024年に85億米ドルとなり、2025年から2034年にかけてCAGR 6.9%で成長すると予測されています。米国は、特に芝生が一般的な農村部や郊外での住宅所有が普及しているため、市場をリードしています。日曜大工の文化が根強く、芝生の手入れに季節性があることも相まって、ロボット芝刈り機、乗用芝刈り機、環境に配慮したツールなど、さまざまな製品に対する需要が高いです。特に暖かい季節のアウトドアライフの人気は、庭や庭のメンテナンス機器への定期的な投資を後押ししています。

世界芝生・庭用機器市場の主要企業には、Kubota Corporation、Briggs &Stratton Corporation、Stanley Black &Decker、Fiskars Group、Honda Motor Co., Ltd、Ariens Company、STIGA S.p.A、Koki Holdings Co., Ltd、Makita Corporation、Falcon Garden Tools、The Toro Company、Husqvarna Group、Techtronic Industries Co., Ltd(TTI)、Robert Bosch GmbH、MTD Holdings Inc、Stihl Holding AG &Co.KG、Deere & Companyが挙げられます。芝生・庭用機器部門の企業は、市場での地位を強化するため、複数の戦略的優先事項に注力しています。ロボット芝刈り機やセンサー駆動の灌漑システムなど、スマートでコネクテッドな製品を開発するための研究開発に重点が置かれています。各社は、環境問題への関心の高まりに対応する電動工具やバッテリー駆動工具を導入することで、持続可能性に投資しています。住宅用と商業用の両方に合わせた製品ラインの拡大も主要な成長戦略です。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

業界幹部にとっての重要な意思決定ポイント

市場参入企業にとっての重要な成功要因

- 将来の見通しと戦略的提言

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- 業界への影響要因

- 促進要因

- 技術的進歩

- 環境に優しく持続可能な製品への関心の高まり

- 住宅改修とアウトドアレジャー活動の成長

- 業界の潜在的リスク&課題

- 燃料駆動工具の使用に関する環境懸念

- 高度な機器の高いメンテナンスコスト

- 機会

- スマートガーデニングツールの需要の高まり

- 新興市場への拡大

- 促進要因

- 成長可能性分析

- 将来の市場動向

- テクノロジーとイノベーションの情勢

- 現在の技術動向

- 新興技術

- 価格動向

- 地域別

- 製品タイプ別

- 規制情勢

- 標準とコンプライアンス要件

- 地域規制枠組み

- 認証基準

- 貿易統計(HSコード8432)

- 主要輸入国

- 主要輸出国

- ポーターの分析

- PESTEL分析

- 消費者行動分析

- 購入パターン

- 嗜好分析

- 消費者行動の地域差

- eコマースが購買決定に与える影響

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 地域別

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画

第5章 市場推計・予測:製品タイプ別、2021年~2034年

- 主要動向

- ブロワー

- チェーンソー

- カッターとシュレッダー

- トラクター

- 芝刈り機

- スプリンクラーとホース

- その他(剪定ばさみ、掘り起こし器など)

第6章 市場推計・予測:動力別、2021年~2034年

- 主要動向

- 手動

- 電動

- ガス動力

- その他(ガソリン車など)

第7章 市場推計・予測:価格別、2021年~2034年

- 主要動向

- 低価格

- 中価格

- 高価格

第8章 市場推計・予測:エンドユーザー別、2021年~2034年

- 主要動向

- 住宅用

- 商業用

- その他(公共公園、公共施設、コミュニティスペース)

第9章 市場推計・予測:流通チャネル別、2021年~2034年

- 主要動向

- オンライン

- eコマース

- 企業のウェブサイト

- オフライン

- 専門店

- ホームセンター

- その他(個人、百貨店など)

第10章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- アジア太平洋

- 中国

- 日本

- インド

- 韓国

- オーストラリア

- ラテンアメリカ

- ブラジル

- メキシコ

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- 南アフリカ

第11章 企業プロファイル

- Ariens Company

- Briggs &Stratton Corporation

- Deere &Company

- Falcon Garden Tools

- Fiskars Group

- Honda Motor Co., Ltd

- Husqvarna Group

- Koki Holdings Co., Ltd

- Kubota Corporation

- Makita Corporation

- MTD Holdings Inc

- Robert Bosch GmbH

- Stanley Black &Decker

- STIGA S.p.A

- Stihl Holding AG &Co. KG

- Techtronic Industries Co. Ltd(TTI)

- The Toro Company

The Global Lawn and Garden Equipment Market was valued at USD 41 billion in 2024 and is estimated to grow at a CAGR of 6.7% to reach USD 77.7 billion by 2034. Rising disposable incomes and the expanding middle-class population are fueling consumer interest in home improvement and outdoor aesthetics. As homeowners increasingly prioritize personalized outdoor spaces, the demand for landscaping tools, smart gardening systems, and efficient yard maintenance equipment is steadily rising. New residential developments, especially in suburban and semi-urban zones, are encouraging people to treat lawns and gardens as integral living spaces.

This trend, supported by greater online accessibility, easier financing options, and a growing emphasis on eco-friendly and tech-integrated living, is shaping the outlook of the market. With a growing preference for user-friendly and connected equipment, manufacturers are focusing on automated solutions such as robotic lawn mowers, app-based irrigation systems, and intelligent gardening tools. These innovations not only reduce manual workload but also allow users to achieve precise control and enhance the overall functionality of their green spaces.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $41 Billion |

| Forecast Value | $77.7 Billion |

| CAGR | 6.7% |

The lawn mowers generated USD 12.3 billion in 2024 and is forecast to reach USD 24.1 billion by 2034. These tools remain the most utilized product category due to their functionality, ease of use, and critical role in maintaining healthy grass. Consistent mowing supports optimal lawn health, improves curb appeal, and provides a neat and welcoming outdoor setting for homeowners. Whether for small residential yards or larger green areas, lawn mowers are an essential component in outdoor maintenance routines.

The commercial segment is anticipated to grow at a CAGR of 7.1% between 2025 and 2034. Businesses and institutions are increasingly investing in landscaping and green infrastructure as part of urban beautification and sustainability initiatives. Well-maintained outdoor environments help enhance brand image and provide welcoming surroundings across hospitality, corporate, and public settings. With growing urban planning that incorporates green zones, the demand for efficient, cost-effective lawn and garden equipment to manage larger spaces continues to rise.

United States Lawn and Garden Equipment Market was valued at USD 8.5 billion in 2024 and is expected to grow at a CAGR of 6.9% from 2025 to 2034. The U.S. leads the market due to widespread homeownership, especially in rural and suburban areas where lawns are common. A strong do-it-yourself culture, coupled with the seasonal nature of lawn care, keeps demand high for various products such as robotic mowers, riding mowers, and environmentally conscious tools. The popularity of outdoor living, particularly during warmer months, drives recurring investments in garden and yard maintenance equipment.

Leading players in the Global Lawn and Garden Equipment Market include Kubota Corporation, Briggs & Stratton Corporation, Stanley Black & Decker, Fiskars Group, Honda Motor Co., Ltd, Ariens Company, STIGA S.p.A, Koki Holdings Co., Ltd, Makita Corporation, Falcon Garden Tools, The Toro Company, Husqvarna Group, Techtronic Industries Co., Ltd (TTI), Robert Bosch GmbH, MTD Holdings Inc, Stihl Holding AG & Co. KG, and Deere & Company. Companies in the lawn and garden equipment sector are focusing on multiple strategic priorities to strengthen their market position. Emphasis is being placed on R&D to develop smart, connected products such as robotic mowers and sensor-driven irrigation systems. Firms are investing in sustainability by introducing electric and battery-powered tools that cater to growing environmental concerns. Product line expansion tailored to both residential and commercial applications is also a key growth strategy.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product type

- 2.2.3 Power type

- 2.2.4 Price

- 2.2.5 End use

- 2.2.6 Distribution channel

- 2.3 CXO perspectives: Strategic imperatives

2.3.1 Key decision points for industry executives

2.3.2. Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Technological advancements

- 3.2.1.2 Increasing interest in eco-friendly and sustainable products

- 3.2.1.3 Growth in home improvement and outdoor leisure activities

- 3.2.2 Industry pitfalls & challenges

- 3.2.1 Growth drivers

3.2.2.1 Environmental concerns regarding the use of fuel-powered tools

3.2.2.2 High maintenance cost of advanced equipment

- 3.2.3 Opportunities

- 3.2.3.1 Rising demand for smart gardening tools

- 3.2.3.2 Expansion in emerging markets

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By product type

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Trade statistics (HS code- 8432)

- 3.8.1 Major importing countries

- 3.8.2 Major exporting countries

- 3.9 Porter’s analysis

- 3.10 PESTEL analysis

- 3.11 Consumer behaviour analysis

- 3.11.1 Purchasing patterns

- 3.11.2 Preference analysis

- 3.11.3 Regional variations in consumer behaviour

- 3.11.4 Impact of e-commerce on buying decisions

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East and Africa

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 - 2034 (USD Billion) (Million Units)

- 5.1 Key trends

- 5.2 Blowers

- 5.3 Chain saws

- 5.4 Cutters & shredders

- 5.5 Tractors

- 5.6 Lawn mowers

- 5.7 Sprinkler & hoses

- 5.8 Others (pruners, diggers, etc.)

Chapter 6 Market Estimates and Forecast, By Power, 2021 - 2034 (USD Billion) (Million Units)

- 6.1 Key trends

- 6.2 Manual

- 6.3 Electric powered

- 6.4 Gas powered

- 6.5 Others (gasoline powered, etc.)

Chapter 7 Market Estimates and Forecast, By Price, 2021 - 2034 (USD Billion) (Million Units)

- 7.1 Key trends

- 7.2 Low

- 7.3 Medium

- 7.4 High

Chapter 8 Market Estimates and Forecast, By End User, 2021 - 2034 (USD Billion) (Million Units)

- 8.1 Key trends

- 8.2 Residential

- 8.3 Commercial

- 8.4 Others (public parks, institutions, and community spaces)

Chapter 9 Market Estimates & Forecast, By Distribution Channel, 2021 - 2034, (USD Billion) (Million Units)

- 9.1 Key trends

- 9.2 Online

- 9.2.1 E-commerce

- 9.2.2 Company websites

- 9.3 Offline

- 9.3.1 Specialty stores

- 9.3.2 Home Improvement stores

- 9.3.3 Others (individual, department stores, etc.)

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034, (USD Billion) (Million Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 Japan

- 10.4.3 India

- 10.4.4 South Korea

- 10.4.5 Australia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.6 MEA

- 10.6.1 Saudi Arabia

- 10.6.2 UAE

- 10.6.3 South Africa

Chapter 11 Company Profiles

- 11.1 Ariens Company

- 11.2 Briggs & Stratton Corporation

- 11.3 Deere & Company

- 11.4 Falcon Garden Tools

- 11.5 Fiskars Group

- 11.6 Honda Motor Co., Ltd

- 11.7 Husqvarna Group

- 11.8 Koki Holdings Co., Ltd

- 11.9 Kubota Corporation

- 11.10 Makita Corporation

- 11.11 MTD Holdings Inc

- 11.12 Robert Bosch GmbH

- 11.13 Stanley Black & Decker

- 11.14 STIGA S.p.A

- 11.15 Stihl Holding AG & Co. KG

- 11.16 Techtronic Industries Co. Ltd (TTI)

- 11.17 The Toro Company