|

市場調査レポート

商品コード

1859016

整形外科用デバイスの市場機会と促進要因、産業動向分析、2025年~2034年予測Orthopedic Devices Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 整形外科用デバイスの市場機会と促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年10月09日

発行: Global Market Insights Inc.

ページ情報: 英文 160 Pages

納期: 2~3営業日

|

概要

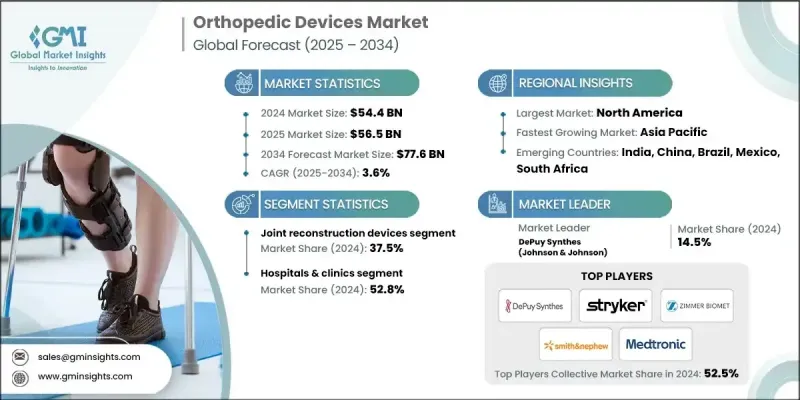

世界の整形外科用デバイス市場は、2024年に544億米ドルと評価され、CAGR 3.6%で成長し、2034年には776億米ドルに達すると予測されています。

成長の原動力は、筋骨格系疾患の世界的な負担増、高齢化、整形外科技術の絶え間ない革新です。整形外科用デバイスは、運動能力の向上、痛みの軽減、患者の生活の質の向上に不可欠なものとなっています。この業界は、関節インプラント、脊椎システム、外傷装置、手術精度や術後ケアを向上させるデジタルツールなどの先進的なソリューションを提供することで、ヘルスケアプロバイダー、ライフサイエンス企業、デジタルヘルスプラットフォームをサポートしています。早期介入に対する意識の高まり、ヘルスケアへの支出の増加、低侵襲技術の出現が需要をさらに高めています。先進国市場でも新興市場でも、これらの医療機器は早期回復、個別化治療、臨床効率の改善によって整形外科医療の形を変えつつあります。また、事故率の上昇、スポーツ関連の怪我、ダウンタイムを短縮する技術的に高度な処置に対する患者の嗜好も需要を支えています。病院や手術センターがデジタル手術システムやロボット手術システムを導入するにつれて、整形外科用デバイスの役割は多様な医療現場で拡大し続けています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 市場規模 | 544億米ドル |

| 予測金額 | 776億米ドル |

| CAGR | 3.6% |

関節再建器具セグメントは2024年に37.5%のシェアを占めました。退行性関節疾患の診断の増加と、特に高齢者における人工股関節置換術および人工膝関節置換術の件数の増加が、この分野を押し上げる主な要因です。これらの機器は、関節の機能性を回復させ慢性的な不快感を和らげるために外科的介入を必要とする、可動性を損なう状態の管理に不可欠です。

脊椎器具分野は2024年に117億米ドルを生み出し、2034年まで安定したCAGR 2.8%で成長すると予測されています。この分野の市場拡大には、高齢化や座りっぱなしの生活スタイルに起因する脊椎疾患の罹患者数の増加が大きく寄与しています。侵襲性の低い外科手術が好まれるようになり、高度な脊椎技術の需要が高まっています。動きを保持するインプラント、生体吸収性コンポーネント、画像誘導システムなどの最近の技術革新により、治療成績が向上し、術後合併症の減少に役立っているため、脊椎手術はより身近で効果的なものとなっています。

北米整形外科用デバイス2024年の市場シェアは55.6%。同地域の強力なヘルスケア・インフラと新しい医療技術への多額の投資が、整形外科ソリューションの幅広い採用を支えています。人口の高齢化と関節炎、肥満、関節関連疾患の多発が、引き続き高い需要を牽引しています。同地域では早期診断・早期介入が好まれ、スポーツ関連外傷の発生率も増加しているため、整形外科用インプラントや器具の臨床現場での使用がさらに加速しています。

整形外科用デバイスの世界市場に参入している主な業界企業には、Enovis、ATEC、MicroPort Scientific、DePuy Synthes(J&J)、Stryker、Waldemar、Zimmer Biomet、Arthrex、TriMed、ConforMIS、Integra、CONMED、Globus Medical、aap Implantate、B. Braun、Smith &Nephew、Medtronic、Medactaなどがあります。整形外科用デバイスの世界市場における主要企業は、技術革新、グローバル展開、戦略的買収を通じて存在感を高めることに注力しています。継続的な研究開発投資により、次世代インプラント、ロボット支援システム、患者専用デバイスを開発しています。パートナーシップや現地生産を通じて新興市場に進出することで、増大する需要や規制上のニーズを満たすことができます。各社はまた、臨床転帰を向上させるため、AIを活用した手術計画ツールや遠隔患者モニタリングなどのデジタル技術にも投資しています。

よくあるご質問

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 業界への影響要因

- 促進要因

- 高齢者人口の増加

- 整形外科疾患の増加

- 技術的進歩

- 先進国における整形外科手術率の上昇

- 業界の潜在的リスク&課題

- 過剰なコスト整形外科用デバイス

- 厳しいFDA規制と生体適合性の問題

- 市場機会

- 低侵襲整形外科手術の採用増加

- 新興国におけるヘルスケア・インフラの拡大

- 促進要因

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ・中東・アフリカ

- テクノロジー・情勢

- 現在の技術動向

- ポータブル家庭用整形外科用デバイス

- デジタルヘルス遠隔モニタリング

- 患者に優しい振動システム

- 新興技術

- AI呼吸器予測分析

- ウェアラブル・コネクテッド整形外科用デバイス

- スマート適応療法機器

- 現在の技術動向

- ギャップ分析

- ポーター分析

- PESTEL分析

- 今後の市場動向

- IoTシステムの統合

- 個別化整形外科ソリューション

- ロボット支援機器アプリケーション

第4章 競合情勢

- イントロダクション

- 企業マトリックス分析

- 企業の市場シェア分析

- グローバル

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ・中東・アフリカ

- 競合ポジショニングマトリックス

- 主要市場企業の競合分析

- 主な発展

- 合併・買収

- パートナーシップ&コラボレーション

- 新しいサービスタイプの立ち上げ

- 拡張計画

第5章 市場推計・予測:製品別、2021-2034

- 主要動向

- 関節再建器具

- 人工膝関節置換術

- 人工股関節置換術

- 人工肩関節置換術

- 人工足関節置換術

- その他の関節再建器具

- 脊椎器具

- 外傷固定装置

- 生物工学

- 関節鏡視下手術機器

- その他の製品

第6章 市場推計・予測:最終用途別、2021-2034

- 主要動向

- 病院・診療所

- 外来手術センター

- その他のエンドユース

第7章 市場推計・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋地域

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第8章 企業プロファイル

- aap Implantate

- Arthrex

- ATEC

- B. Braun

- ConforMIS

- CONMED

- DePuy Synthes(J&J)

- Enovis

- Globus Medical

- Integra

- Medacta

- Medtronic

- MicroPort Scientific

- Smith &Nephew

- Stryker

- TriMed

- Waldemar

- Zimmer Biomet