|

市場調査レポート

商品コード

2038424

自動運転ソフトウェア市場の機会、成長要因、業界動向分析、および2026年~2035年の予測Autonomous Driving Software Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

カスタマイズ可能

|

|||||||

| 自動運転ソフトウェア市場の機会、成長要因、業界動向分析、および2026年~2035年の予測 |

|

出版日: 2026年04月27日

発行: Global Market Insights Inc.

ページ情報: 英文 180 Pages

納期: 2~3営業日

|

概要

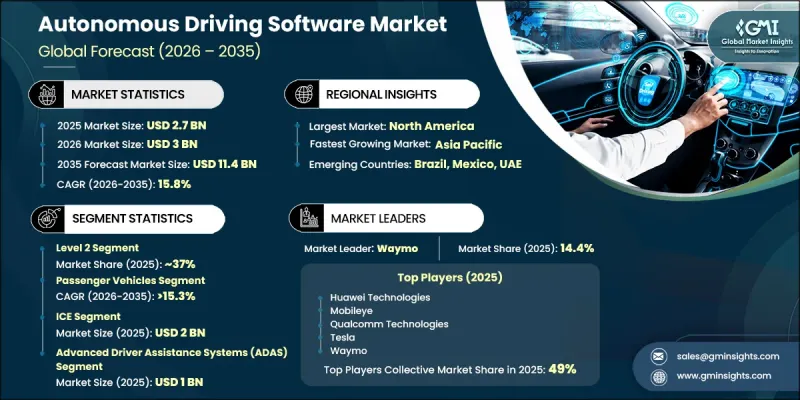

世界の自動運転ソフトウェア市場は、2025年に27億米ドルと評価され、CAGR 15.8%で成長し、2035年までに114億米ドルに達すると予測されています。

自動車のインテリジェンスが、より高度な自動化やソフトウェア定義の車両エコシステムへと急速に進化する中、市場は力強い勢いを見せています。ADAS(先進運転支援システム)の統合が進むことで車両アーキテクチャが再構築される一方、AIを活用した知覚・意思決定プラットフォームは、次世代モビリティソリューションの中核となりつつあります。また、多様な運転条件下において、より安全で効率的な運転体験を支えるリアルタイムデータ処理機能への需要も高まっています。乗用車、商用車、ロボタクシーネットワーク、モビリティサービスプラットフォームにおけるコネクテッドカー技術の導入拡大が、ソフトウェアの採用をさらに加速させています。自動車メーカーや技術開発企業は、自動運転機能と安全性を向上させるため、センサーフュージョンシステム、予測制御アルゴリズム、および高性能コンピューティングプラットフォームへの投資を拡大しています。人工知能、機械学習モデル、エッジコンピューティング機能の継続的な改善により、イノベーションのサイクルが加速しています。同時に、ソフトウェア定義型車両のフレームワークが従来の自動車設計手法を変革しており、自動運転ソフトウェアは将来のモビリティエコシステムを実現する重要な要素となっています。

| 市場範囲 | |

|---|---|

| 開始年 | 2025年 |

| 予測期間 | 2026年~2035年 |

| 開始時の市場規模 | 27億米ドル |

| 予測額 | 114億米ドル |

| CAGR | % |

自動運転ソフトウェア市場は、自動車メーカーに対し、交通安全の向上、事故率の低減、そしてより高度な運転支援機能の提供を求める圧力が高まっていることで、さらに牽引されています。AIを活用した知覚技術やリアルタイムナビゲーション技術の進歩により、基本的な支援システムから完全に統合された自動運転ソフトウェアアーキテクチャへの移行が加速しています。最新のプラットフォームは、一元化された車両インテリジェンス、意思決定の向上、および無線アップデートによる継続的なパフォーマンス最適化を可能にします。これらの機能により、人間の介入への依存度が低減されると同時に、車両のライフサイクル全体にわたる運用上の安全性とシステムの信頼性が向上します。

レベル2セグメントは2025年に37%のシェアを占め、2026年から2035年にかけてCAGR15.5%で成長すると予測されています。このセグメントは、高度な運転支援技術を搭載した市販車への広範な導入により、引き続き主導的な地位を維持しています。このセグメントは、適応型運転支援、車線位置制御、自動ブレーキシステム、渋滞支援機能、および部分的な自動高速道路ナビゲーションなどの機能をサポートしています。その強固な市場地位は、主流の車両カテゴリーにおける大規模な導入に加え、AI駆動の知覚システム、センサー統合、およびリアルタイム処理能力の継続的な改善によってさらに強化されています。ソフトウェアプラットフォームと自動化機能の継続的な改良により、世界の自動車市場全体での採用がさらに促進されています。

乗用車セグメントは2025年に75.6%のシェアで市場を独占しており、2026年から2035年にかけてCAGR15.3%超で成長すると予想されています。この優位性は、コンパクトカー、SUV、電気自動車(EV)を含む現代の乗用車プラットフォーム全体への自動運転ソフトウェアの統合が進んでいることに支えられています。安全性の向上、運転の利便性向上、およびコネクテッドモビリティ機能に対する消費者の需要の高まりが、インテリジェントドライビングシステムの導入を加速させています。知覚、ナビゲーション、運転支援のためのスケーラブルなソフトウェアソリューションの利用可能性が高まっていることが、大衆車および高級車の両カテゴリーにおける広範な導入をさらに後押ししています。このセグメントは、自動運転ソフトウェアエコシステムの主要な成長エンジンであり続けています。

米国の自動運転ソフトウェア市場は83%のシェアを占め、2025年には8億5,930万米ドルの市場規模に達しました。同国の主導的地位は、強固な自動車製造基盤、先進的なデジタルインフラ、そしてコネクテッドカーおよび自動運転技術の急速な普及によって支えられています。人工知能、センサーフュージョンプラットフォーム、自動運転モビリティシステムへの多額の投資が、ソフトウェアのイノベーションを加速させています。乗用車、電動モビリティプラットフォーム、商用車フリート事業への導入拡大が、市場の成長をさらに後押ししています。クラウドベースの車両コネクティビティとリアルタイム分析の継続的な進歩もまた、自動運転ソフトウェア開発における世界のハブとしての同国の地位を強化しています。

よくあるご質問

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- コスト構造

- 各段階における付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- AI、機械学習、およびセンサーフュージョン技術の急速な進歩

- 車両の安全性およびADAS統合に対する需要の高まり

- 電気自動車およびソフトウェア定義車両の普及拡大

- ロボタクシー、自動運転トラック、およびフリート自動化の拡大

- 業界の潜在的リスク&課題

- 高い開発および検証コスト

- 規制の不確実性と法的コンプライアンス上の課題

- 市場機会

- ロボタクシーおよび自動運転モビリティサービスの成長

- 自律走行商用車両および物流の拡大

- AIを活用したフリート管理および予知保全

- 都市型自動運転モビリティとスマートシティとの統合

- 促進要因

- 成長可能性分析

- 規制情勢

- 北米

- 米国- 自動運転ソフトウェアおよび安全基準遵守に関する連邦および州レベルの規制枠組み

- カナダ- 自動運転車向けソフトウェアテストおよびデータガバナンスに関する国家ガイドライン

- 欧州

- 英国- 自動運転車(AV)およびAI安全法に基づく自動運転ソフトウェアに対する規制監督

- ドイツ-EU枠組みに基づく自動運転システムの型式認定および安全規制

- フランス- 自動運転ソフトウェアの試験運用およびデータ保護コンプライアンスに関する法的枠組み

- アジア太平洋地域

- インド- 自動運転ソフトウェアおよび道路安全政策に関する規制状況の動向

- 中国- 自動運転ソフトウェアのテストおよびサイバーセキュリティコンプライアンスに関する政府主導の規制

- 日本- 自動運転ソフトウェアの導入に関する国家政策および機能安全基準

- ラテンアメリカ

- ブラジル- 自動運転ソフトウェアおよび車両自動化基準に関する新たな規制

- 中東・アフリカ

- UAE-自動運転ソフトウェアおよびAI統合に関するスマートモビリティ規制

- 北米

- 技術およびイノベーションの動向

- 現在の技術動向

- 新興技術

- 価格分析(1次調査に基づく)

- 過去の価格動向分析

- プレーヤータイプ別の価格戦略

- ポーター分析

- PESTEL分析

- 特許分析(1次調査に基づく)

- AIおよび生成AIが市場に与える影響

- AIによる既存ビジネスモデルの変革

- セグメント別のGenAIの使用事例と導入ロードマップ

- リスク、制約、および規制上の考慮事項

- サステナビリティおよび環境面

- 持続可能な取り組み

- 廃棄物削減戦略

- 生産におけるエネルギー効率

- 環境に配慮した取り組み

- カーボンフットプリントに関する考慮事項

- 予測の前提条件およびシナリオ分析(1次調査に基づく)

- ベースケース-CAGRを牽引する主要なマクロ経済および業界変数

- 楽観的シナリオ- マクロ経済および業界における追い風

- 悲観シナリオ- マクロ経済の減速または業界の逆風

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

- 主な発展

- 合併・買収

- パートナーシップおよび提携

- 新製品の発売

- 事業拡大計画と資金調達

- 企業のティア別ベンチマーク

- ティア分類基準および選定基準

- 売上高、地域、イノベーション別のティア位置付けマトリックス

第5章 市場推計・予測:自動化レベル別、2022-2035

- レベル1

- レベル2

- レベル3

- レベル4

- レベル5

第6章 市場推計・予測:車種別、2022-2035

- 乗用車

- ハッチバック

- セダン

- SUV

- 商用車

- 小型商用車(LCV)

- 中型商用車(MCV)

- 大型商用車(HCV)

第7章 市場推計・予測:推進方式別、2022-2035

- 内燃機関

- 電気自動車

第8章 市場推計・予測:ソフトウェア別、2022-2035

- 知覚・計画ソフトウェア

- 運転支援ソフトウェア

- 車内センシングソフトウェア

- 監視・モニタリングソフトウェア

第9章 市場推計・予測:用途別、2022-2035

- ADAS(先進運転支援システム)

- 自動駐車

- 高速道路自動運転

- 都市部での自動運転

- フリート自動化

第10章 市場推計・予測:地域別、2022-2035

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ベルギー

- オランダ

- スウェーデン

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- シンガポール

- 韓国

- ベトナム

- インドネシア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ(MEA)

- アラブ首長国連邦

- 南アフリカ

- サウジアラビア

第11章 企業プロファイル

- Global Player

- Aptiv

- Aurora Innovation

- Continental

- Huawei Technologies

- Mobileye

- NVIDIA

- Qualcomm Technologies

- Tesla

- Waymo

- Zoox

- Regional Player

- AImotive

- AutoX

- Bosch

- Denso

- Luminar Technologies

- Magna International

- Nuro

- Pony.ai

- Tier IV

- Valeo