|

市場調査レポート

商品コード

1773247

歯科予防用品の市場機会、成長促進要因、産業動向分析、2025年~2034年予測Dental Preventive Supplies Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 歯科予防用品の市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年06月19日

発行: Global Market Insights Inc.

ページ情報: 英文 135 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

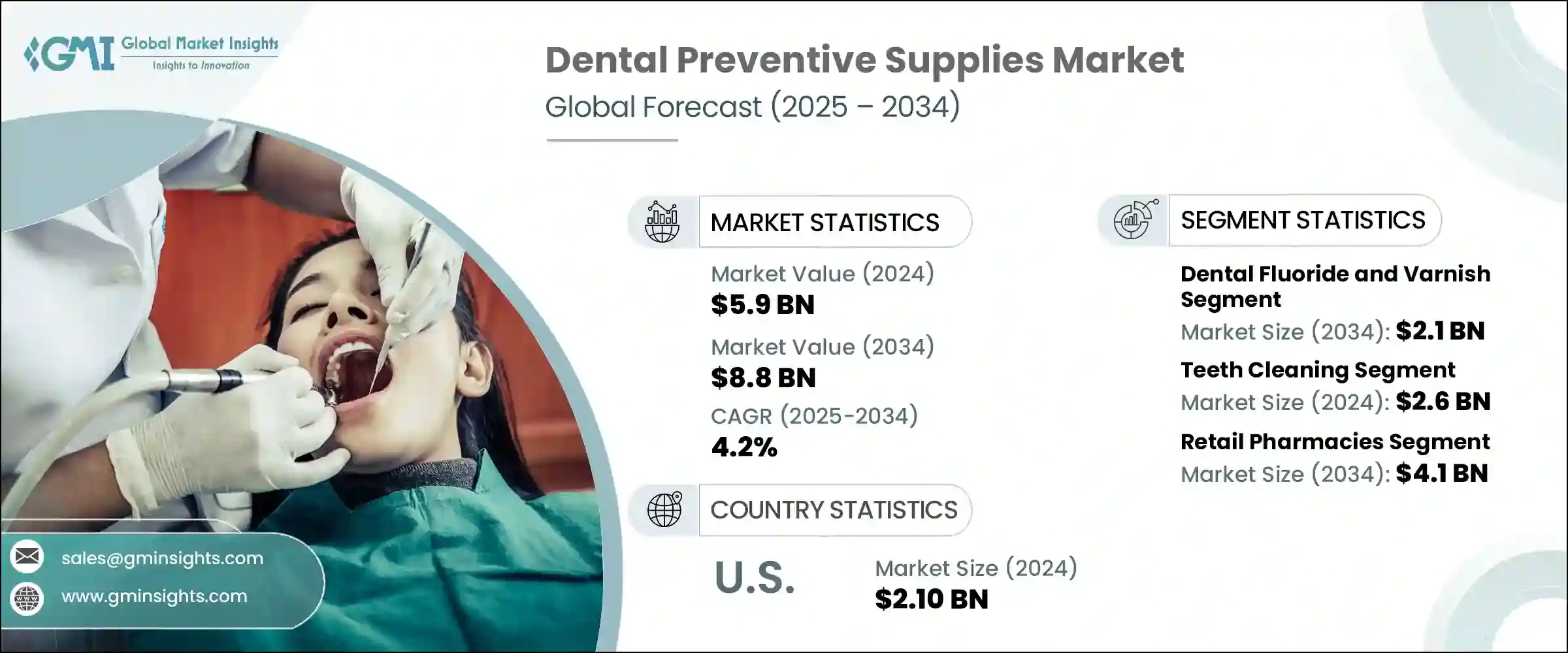

世界の歯科予防用品市場は、2024年に59億米ドルと評価され、CAGR 4.2%で成長し、2034年には88億米ドルに達すると推定されています。

この成長には、歯科疾患の罹患率の上昇、口腔衛生に対する国民の意識の高まり、歯科予防製品における継続的な技術革新が寄与しています。予防の重要性を認識する人が増えるにつれ、歯磨き粉、フロス、洗口液などの製品が広く採用されるようになっています。口腔衛生を推進する政府や健康団体による取り組み、特に学校でのプログラムや一般向けの啓発キャンペーンは、予防用品の使用をさらに促しています。歯科予防用具の進歩は、専門家と消費者の両方が口腔ケアに取り組む方法に革命をもたらし、毎日の習慣をより効果的で個々のニーズに合ったものにしています。

歯科予防用品には、虫歯や歯肉の炎症などの口腔疾患のリスクを軽減するためにデザインされた幅広い製品が含まれています。これらの用品は、歯科医師と口腔内の健康を最適に保ちたいと願う個人の両方に役立っています。技術の進歩は市場拡大において重要な役割を果たしており、革新的な製品は使いやすさ、正確さ、利便性を高めています。例えば、センサー、人工知能、Bluetooth接続を備えたスマート歯ブラシは、ユーザーがブラッシング習慣をモニターし、リアルタイムのフィードバックを通じて技術を改善することを可能にし、口腔ケアをよりパーソナライズされた体験に変えます。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025年~2034年 |

| 開始金額 | 59億米ドル |

| 予測金額 | 88億米ドル |

| CAGR | 4.2% |

歯科用フッ化物・ワニス分野は、歯科疾患、特に小児と高齢者のう蝕と虫歯の世界の発生率の増加が主な要因となって、2034年までに21億米ドルに成長すると予測されます。砂糖の多量摂取、タバコの消費、口腔衛生習慣の悪さなどの要因が、これらの歯科疾患の有病率上昇に大きく寄与しています。そのため、歯を保護し、虫歯を減らすのに役立つフッ素治療やワニスのような予防手段の需要が高まっています。

2024年、歯のクリーニングサービス分野は26億米ドルを生み出しました。この成長は、虫歯や歯肉炎などの歯科疾患を予防することの重要性に対する一般市民の意識の高まりによるところが大きいです。このセグメントはさらに、口腔の健康問題をより多く経験する傾向にある世界の高齢化人口の拡大によって支えられています。その結果、専門家による定期的な歯のクリーニングサービスの需要が高まり、口腔の健康維持とさらなる合併症の予防に役立っています。

米国の歯科予防用品2024年の市場規模は21億米ドルでした。この強力な市場地位は、予防ケアを専門とする多くの高度な訓練を受けた歯科専門家によって支えられています。また、歯科医療技術や教育の継続的な進歩も市場の成長を支えています。これらの要因から、米国は世界の歯科予防用品業界において重要な企業となっており、継続的な技術革新と専門知識が需要と製品開発に拍車をかけています。

歯科予防用品市場で事業を展開する主要企業には、コルゲート・パルモリーブ・カンパニー、3Mカンパニー、ジョンソン・エンド・ジョンソン、ザ・プロクター・アンド・ギャンブル・カンパニー、デンツプライ・シロナ・インク、ハレオン、Ivoclar Vivadent、Henry Schein, Inc.、Sunstar Suisse S.A.、Kerr Corporation、Hu-Friedy Mfg. Co., LLC.、Ultradent Products Inc.、Church &Dwight Co.、Young Innovations, Inc.などがあります。歯科予防用品分野の主要企業は、市場での地位を強化するため、継続的なイノベーション、製品ポートフォリオの拡大、戦略的パートナーシップに注力しています。

研究開発への投資により、企業は進化する消費者の嗜好に対応したスマート歯科機器や天然成分ベースの製品など、先進的なソリューションを導入することができます。市場リーダーはまた、口腔衛生への意識が急速に高まっている新興市場に参入し、地理的な拡大を重視しています。歯科専門家、教育機関、政府の保健プログラムとのコラボレーションは、製品の採用とブランドの信頼性を高めるのに役立ちます。さらに、企業はデジタル・マーケティングやeコマース・プラットフォームを活用して、より多くの消費者に直接リーチしています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 業界への影響要因

- 促進要因

- 口腔衛生意識の高まり

- 歯科疾患の罹患率の増加

- 歯科予防用品における技術の進歩

- 業界の潜在的リスク&課題

- 歯科治療に伴う高額な費用

- 歯科医療へのアクセスにおける経済的障壁

- 促進要因

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋

- 日本

- 中国

- インド

- 技術的情勢

- 現在の技術動向

- 新興技術

- 将来の市場動向

- 価格分析

- バリューチェーン分析

- 消費者行動分析

- 口腔衛生習慣の動向の変化

- デジタルメディアが予防歯科ケアに与える影響

- 自然食品やオーガニック製品に対する消費者の嗜好

- ギャップ分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:製品タイプ別、2021年~2034年

- 主要動向

- 歯科用フッ化物とワニス

- 歯のホワイトニングと知覚過敏治療薬

- 予防用ペーストおよび粉末

- シーラント

- デンタルフロス

- マウスジェル

- その他の製品タイプ

第6章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- 歯のクリーニング

- 歯のホワイトニング

- 歯のコーティング

第7章 市場推計・予測:流通チャネル別、2021年~2034年

- 主要動向

- 小売薬局

- ドラッグストア

- eコマース

第8章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第9章 企業プロファイル

- 3M Company

- Church &Dwight Co.

- Colgate-Palmolive Company

- Dentsply Sirona

- GC International

- Haleon

- Henry Schein

- Hu-Friedy Mfg.

- Ivoclar Vivadent

- Johnson &Johnson

- Kerr Corporation

- Sunstar Suisse

- The Procter &Gamble Company

- Ultradent Products

- Young Innovations

The Global Dental Preventive Supplies Market was valued at USD 5.9 billion in 2024 and is estimated to grow at a CAGR of 4.2% to reach USD 8.8 billion by 2034. This growth is fueled by the rising incidence of dental conditions, increasing public awareness about oral health, and continuous technological innovations in dental preventive products. As more people recognize the importance of prevention, products like toothpaste, floss, and mouthwash are seeing broader adoption. Efforts by governments and health organizations promoting oral hygiene, especially through school programs and public awareness campaigns, are further encouraging the use of preventive supplies. Advancements in dental preventive tools are revolutionizing how both professionals and consumers approach oral care, making daily routines more effective and tailored to individual needs.

Dental preventive supplies encompass a wide array of products designed to reduce the risk of oral diseases such as tooth decay and gum inflammation. These supplies serve both dental practitioners and individuals who want to maintain optimal oral health. Technological progress plays a key role in market expansion, with innovative products enhancing usability, accuracy, and convenience. For instance, smart toothbrushes equipped with sensors, artificial intelligence, and Bluetooth connectivity allow users to monitor brushing habits and improve techniques through real-time feedback, transforming oral care into a more personalized experience.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $5.9 Billion |

| Forecast Value | $8.8 Billion |

| CAGR | 4.2% |

The dental fluoride and varnish segment is projected to grow to USD 2.1 billion by 2034, driven largely by the increasing global incidence of dental issues, especially dental caries and tooth decay among children and older adults. Factors such as high sugar intake, tobacco consumption, and poor oral hygiene habits significantly contribute to the rising prevalence of these dental diseases. This, in turn, fuels the demand for preventive measures like fluoride treatments and varnishes, which help protect teeth and reduce decay.

In 2024, the teeth cleaning services segment generated USD 2.6 billion. This growth is largely due to greater public awareness about the importance of preventing dental conditions such as cavities and gingivitis. The segment is further supported by the expanding aging population worldwide, which tends to experience more oral health problems. As a result, the demand for routine professional teeth cleaning services has increased, helping maintain oral health and prevent further complications.

U.S. Dental Preventive Supplies Market was valued at USD 2.10 billion in 2024. This strong market position is supported by many highly trained dental professionals specializing in preventive care. Additionally, continuous advancements in dental technologies and education across the country help sustain market growth. These factors make the U.S. a vital player in the global dental preventive supplies industry, with ongoing innovation and expertise fueling demand and product development.

Major players operating in the Dental Preventive Supplies Market include Colgate-Palmolive Company, 3M Company, Johnson & Johnson, The Procter & Gamble Company, Dentsply Sirona Inc., Haleon, Ivoclar Vivadent, Henry Schein, Inc., Sunstar Suisse S.A., Kerr Corporation, Hu-Friedy Mfg. Co., LLC., Ultradent Products Inc., Church & Dwight Co., and Young Innovations, Inc. Leading companies in the dental preventive supplies sector focus on continuous innovation, expanding product portfolios, and strategic partnerships to strengthen their market position.

Investment in R&D allows firms to introduce advanced solutions like smart dental devices and natural ingredient-based products that meet evolving consumer preferences. Market leaders also emphasize geographic expansion by entering emerging markets where oral health awareness is growing rapidly. Collaborations with dental professionals, educational institutions, and government health programs help boost product adoption and brand credibility. Additionally, companies leverage digital marketing and e-commerce platforms to reach a wider audience directly.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product type

- 2.2.3 Application

- 2.2.4 Distribution channel

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing oral health awareness

- 3.2.1.2 Increasing prevalence of dental disorders

- 3.2.1.3 Technological advancements in dental preventive supplies

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost associated with dental procedures

- 3.2.2.2 Economic barriers to dental care access

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.3.1 Japan

- 3.4.3.2 China

- 3.4.3.3 India

- 3.5 Technological landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Future market trends

- 3.7 Pricing analysis

- 3.8 Value chain analysis

- 3.9 Consumer behaviour analysis

- 3.9.1 Shifting trends in oral hygiene practices

- 3.9.2 Influence of digital media on preventive dental care

- 3.9.3 Consumer preferences for natural and organic products

- 3.10 Gap analysis

- 3.11 Porter's analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Dental fluorides and varnish

- 5.3 Tooth whitening and desensitizers

- 5.4 Prophylactic pastes and powders

- 5.5 Sealants

- 5.6 Dental floss

- 5.7 Mouth gels

- 5.8 Other product types

Chapter 6 Market Estimates and Forecast, By Application, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Teeth cleaning

- 6.3 Teeth whitening

- 6.4 Teeth coating

Chapter 7 Market Estimates and Forecast, By Distribution Channel, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Retail pharmacies

- 7.3 Drug stores

- 7.4 E-commerce

Chapter 8 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 3M Company

- 9.2 Church & Dwight Co.

- 9.3 Colgate-Palmolive Company

- 9.4 Dentsply Sirona

- 9.5 GC International

- 9.6 Haleon

- 9.7 Henry Schein

- 9.8 Hu-Friedy Mfg.

- 9.9 Ivoclar Vivadent

- 9.10 Johnson & Johnson

- 9.11 Kerr Corporation

- 9.12 Sunstar Suisse

- 9.13 The Procter & Gamble Company

- 9.14 Ultradent Products

- 9.15 Young Innovations