|

市場調査レポート

商品コード

2027586

ロボット市場の機会、成長要因、業界動向分析、および2026年~2035年の予測Robot Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

カスタマイズ可能

|

|||||||

| ロボット市場の機会、成長要因、業界動向分析、および2026年~2035年の予測 |

|

出版日: 2026年04月13日

発行: Global Market Insights Inc.

ページ情報: 英文 180 Pages

納期: 2~3営業日

|

概要

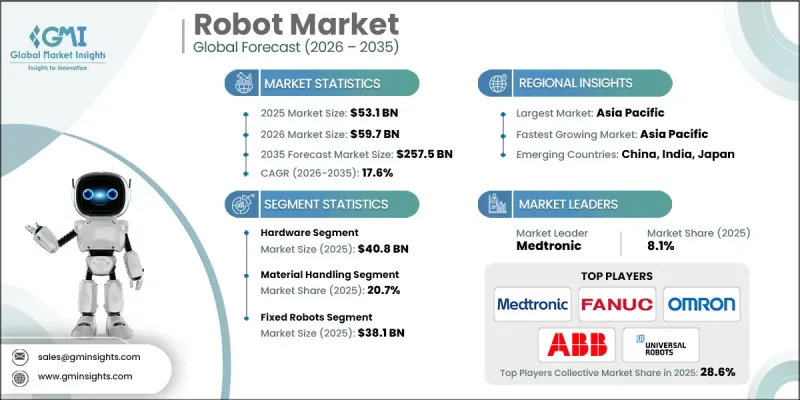

世界のロボット市場は2025年に531億米ドルと評価され、2035年までにCAGR 17.6%で成長し、2,575億米ドルに達すると推定されています。

市場の成長は、ロボット工学、人工知能、機械学習の急速な進歩によって牽引されており、これらは業界を問わず業務プロセスを変革しています。これらの技術は、より高度な自動化と精度を実現することで、サプライチェーンの運用を再構築し、顧客対応システムを強化しています。現代のロボットシステムは、高度なセンシング機能、インテリジェントな動作計画、および強化された適応性を備えて設計されており、複雑なタスクを高精度で実行することが可能です。企業は、高まる業務需要への対応、効率の向上、処理時間の短縮を図るため、ロボットソリューションの導入をますます進めています。より迅速かつ正確な注文処理へのニーズの高まりは、物流や業務ワークフローへのロボット技術の統合をさらに加速させています。さらに、従業員の生産性や業務の拡張性に対する圧力が高まる中、反復的で肉体的に過酷な作業を処理できる自動化ソリューションの導入が企業に促されています。各業界が効率性とパフォーマンスの最適化に注力し続ける中、ロボットシステムの導入は世界市場全体で大幅に拡大すると予想されます。

| 市場の範囲 | |

|---|---|

| 開始年 | 2025年 |

| 予測期間 | 2026年~2035年 |

| 開始時の市場規模 | 531億米ドル |

| 予測額 | 2,575億米ドル |

| CAGR | 17.6% |

ハードウェア分野は2025年に408億米ドルの市場規模を記録しました。この分野の成長は、協働ロボットの普及拡大と、ロボットの中核となるコンポーネントの継続的な改良によって支えられています。高度なコントローラー、アクチュエーター、エンドエフェクターにより、幅広い用途において、より精密かつ効率的なロボット操作が可能になっています。センサーは、機械が周囲の環境を検知し、自律的に動作することを可能にすることで、ロボットの機能向上に極めて重要な役割を果たしています。詳細かつ複雑なタスクを実行できる高度なロボットシステムへの需要の高まりが、先進的なセンシング技術の採用を後押ししています。こうした進展は、ロボットハードウェアの全体的な性能と信頼性を高め、市場におけるその重要性をさらに強めています。

2025年時点で、固定型ロボットセグメントは381億米ドルを占めており、業界におけるその確固たる存在感を示しています。このセグメントは、性能の向上と応用分野の拡大をもたらす、ロボット設計およびエンジニアリングにおける継続的な技術進歩の恩恵を受けています。固定型ロボットシステムは、高い精度と一貫性が求められる作業に広く利用されており、様々な産業プロセスにおいて不可欠な存在となっています。反復的かつ危険な作業を正確に遂行する能力は、生産性を向上させると同時に、職場の安全性を高めています。各産業が業務効率化を図るために自動化への投資を続ける中、固定型ロボットシステムへの需要は引き続き堅調であると予想されます。

北米のロボット市場は2025年に110.6%のシェアを占め、その先進的かつイノベーション主導のエコシステムを浮き彫りにしています。同地域では自動化技術の導入率が高く、ロボット開発者、インテグレーター、エンドユーザーからなる確立されたネットワークの恩恵を受けています。先進的な製造およびスマート生産環境への強力な投資が、市場の拡大を支えています。米国は、生産性向上の重視や労働力に関する課題への対応が必要とされる中、地域の成長を牽引する重要な役割を果たしています。継続的な技術革新と戦略的な投資により、ロボット市場における同地域のリーダーシップが維持されると予想されます。

よくあるご質問

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- コスト構造

- 各段階における付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- Eコマースと物流需要の急増

- 人件費の高騰と労働力不足

- 医療分野におけるロボットの活用拡大

- ロボティクス・アズ・ア・サービス(RaaS)の人気の高まり

- 急速な技術開発

- 業界の潜在的リスク&課題

- 高い初期費用

- ロボットに伴う技術的複雑性

- 市場機会

- 中小企業における協働ロボット(コボット)の普及

- ロボット工学へのAIおよび機械学習の統合

- 促進要因

- 成長可能性分析

- 規制情勢

- ポーター分析

- PESTEL分析

- 技術およびイノベーションの動向

- 現在の技術動向

- 新興技術

- 価格動向

- 地域別

- 製品別

- 価格戦略

- 新興ビジネスモデル

- コンプライアンス要件

- 特許および知的財産分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 地域別

- 市場集中度の分析

- 主要企業の競合ベンチマーキング

- 財務実績の比較

- 売上高

- 利益率

- 研究開発(R&D)

- 製品ポートフォリオの比較

- 製品ラインの幅

- 技術

- イノベーション

- 地域展開の比較

- 世界展開の分析

- サービスネットワークのカバー範囲

- 地域別市場浸透率

- 競合ポジショニングマトリックス

- リーダー

- チャレンジャー

- フォロワー

- ニッチプレイヤー

- 戦略的展望マトリックス

- 財務実績の比較

- 主な発展

- 合併・買収

- 提携および協業

- 技術的進歩

- 事業拡大および投資戦略

- デジタルトランスフォーメーションの取り組み

- 新興/スタートアップ競合企業の動向

第5章 市場推計・予測:タイプ別、2022-2035

- 産業用ロボット

- 多関節ロボット

- スカラロボット

- 直交ロボット

- デルタロボット

- 協働ロボット(コボット)

- パラレルロボット

- その他

- サービスロボット

- パーソナルサービスロボット

- 業務用サービスロボット

第6章 市場推計・予測:コンポーネント別、2022-2035

- ハードウェア

- 機械部品

- 駆動・駆動部品

- 関節・ベアリングシステム

- ばね・弾性部品

- 締結・接続部品

- エンドエフェクタおよびツーリング

- その他

- 電子部品

- モーターおよびアクチュエータ

- センサー

- コントローラおよびプロセッサ

- 電源およびバッテリー

- その他

- 機械部品

- ソフトウェア

- サービス

- エンジニアリングおよび設置

- 保守・サポート

- トレーニングおよび教育

第7章 市場推計・予測:移動手段別、2022-2035

- 固定型ロボット

- 移動型ロボット

- ヒューマノイドロボット

第8章 市場推計・予測:用途別、2022-2035

- 組立・生産

- 検査・品質管理

- マテリアルハンドリング

- 溶接・はんだ付け

- 包装・パレタイジング

- 医療支援

- セキュリティ・監視

- 小売・顧客対応ロボット

- 教育

- その他

第9章 市場推計・予測:最終用途産業別、2022-2035

- 製造・産業

- 自動車

- エレクトロニクス・半導体

- 食品・飲料

- 医薬品

- 金属・機械

- その他

- ヘルスケア

- 防衛

- 農業

- 家庭用

- 小売・Eコマース

- ホスピタリティ

- 物流

- その他

第10章 市場推計・予測:地域別、2022-2035

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- その他欧州地域

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- その他アジア太平洋地域

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- その他ラテンアメリカ地域

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

- その他中東・アフリカ地域

第11章 企業プロファイル

- 世界の主要企業

- ABB Ltd.

- Fanuc Corporation

- KUKA AG

- Yaskawa Electric Corporation

- Mitsubishi Electric Corporation

- Omron Corporation

- Intuitive Surgical

- Medtronic

- 地域別主要企業

- Clearpath Robotics

- MiR(Mobile Industrial Robots)

- Staubli Group

- Universal Robots

- Aethon

- ニッチプレイヤー/ディスラプター

- Boston Dynamics

- Blue Ocean Robotics

- Ecovacs Robotics

- iRobot Corporation

- Knightscope, Inc.

- Segway Robotics

- SoftBank Robotics