|

市場調査レポート

商品コード

1913419

自動車用ヒートシールド市場の機会、成長要因、業界動向分析、および2026年から2035年までの予測Automotive Heat Shield Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

カスタマイズ可能

|

|||||||

| 自動車用ヒートシールド市場の機会、成長要因、業界動向分析、および2026年から2035年までの予測 |

|

出版日: 2025年12月24日

発行: Global Market Insights Inc.

ページ情報: 英文 240 Pages

納期: 2~3営業日

|

概要

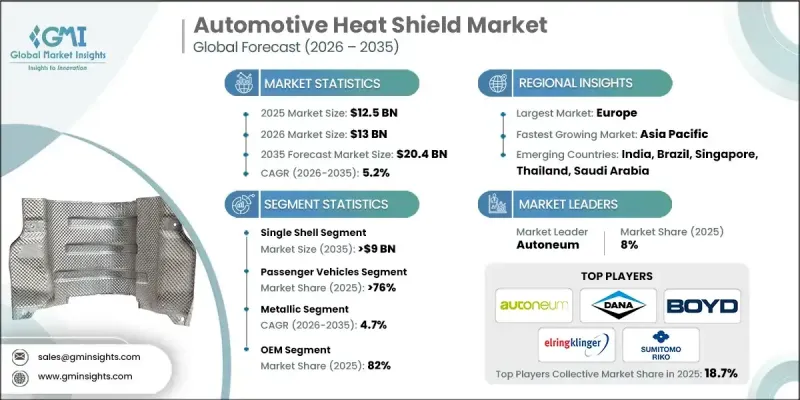

世界の自動車用ヒートシールド市場は、2025年に125億米ドルと評価され、2035年までにCAGR5.2%で成長し、204億米ドルに達すると予測されています。

市場成長は、現代の車両アーキテクチャ全体における熱管理要件の高まりによって支えられています。ガソリン車およびディーゼル車の両方で過給エンジンが採用されるケースが増加していることから、周辺部品を保護し、構造的完全性を維持し、長期的なエンジン性能を支える耐久性のある熱保護ソリューションの必要性が強まっています。同時に、電動化モビリティへの移行に伴い、バッテリー、パワーエレクトロニクス、充電システムに関連する新たな熱制御の要求が生じています。自動車用ヒートシールドは、熱分散の調整、部品寿命の延長、電気自動車およびハイブリッド車プラットフォーム全体での安全な運転のサポートのために、ますます活用されています。運転の快適性と車両の安全性に対する消費者の関心の高まりも需要をさらに強化しています。効果的な断熱材は、キャビンへの熱伝達を制限し、高温から敏感なシステムを保護するためです。規制圧力も重要な役割を果たしており、自動車メーカーは、世界市場で強化される排出ガス、火災安全、熱コンプライアンス基準を満たすために、ヒートシールドに依存しています。車両がより複雑で高出力化されるにつれて、高度な遮熱ソリューションは、性能、安全性、規制への適合性にとって不可欠であり続けています。

| 市場範囲 | |

|---|---|

| 開始年 | 2025年 |

| 予測年度 | 2026-2035 |

| 開始時価値 | 125億米ドル |

| 予測金額 | 204億米ドル |

| CAGR | 5.2% |

2025年、シングルシェルカテゴリーは47%のシェアを占め、2035年までに90億米ドルに達すると予測されています。このセグメントは、コスト効率の良さ、製造の簡便さ、そして特に大量生産車両プラットフォームにおいて、中程度の熱負荷がかかる用途での有効性から、引き続き高い採用率を維持しています。

2025年には乗用車が76%のシェアを占め、95億米ドルの市場規模を生み出しました。大量生産、排出ガス規制の強化、ターボチャージャーエンジンの普及、電動化の加速により、主流車種から高級車種に至るまで、熱管理の複雑化が進んでいます。

米国自動車用ヒートシールド市場は2025年に19億1,000万米ドルと評価され、2035年まで堅調な成長が見込まれています。ターボチャージャーエンジンとハイブリッド駆動系の継続的な普及が、先進的な排気系およびパワートレイン用ヒートシールドソリューションの需要を支えています。軽量化の優先課題により、効率目標の達成、電気走行距離の延長、連邦安全基準および排出ガス基準への適合を支援するため、複合材および多層設計の採用が促進されています。

よくあるご質問

目次

第1章 調査手法

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率分析

- コスト構造

- 各工程における付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- 排出ガス規制および熱安全規制の厳格化

- 増加する自動車生産台数と車両保有台数の成長

- ターボチャージャーおよび高性能エンジンの採用増加

- 電気自動車およびハイブリッド車における熱管理ニーズの拡大

- アフターマーケットにおける交換需要の成長

- 業界の潜在的リスク&課題

- 原材料価格の変動性

- 完全電気自動車におけるヒートシールド使用量の減少傾向

- 市場機会

- EV用バッテリー及びパワーエレクトロニクス向けヒートシールド

- 軽量化および先進断熱材料の導入状況

- アンダーボディおよびモジュラー型ヒートシールドソリューションの拡大

- 新興市場におけるアフターマーケットおよび改造需要の成長

- 成長可能性分析

- 規制情勢

- 北米

- 米国-ISO 9001品質マネジメントシステム

- カナダ-ISO 45001労働安全衛生

- 欧州

- 英国-ISO/IEC 27001情報セキュリティマネジメント

- ドイツ-ISO 50001エネルギーマネジメントシステム

- フランス-ISO 45001労働安全衛生

- イタリア-ISO 14001環境マネジメントシステム

- スペイン-ISO 22000食品安全マネジメントシステム

- アジア太平洋地域

- 中国-ISO/IEC 27001情報セキュリティマネジメント

- 日本-ISO 14001環境マネジメントシステム

- インド-ISO 45001労働安全衛生

- ラテンアメリカ

- ブラジル-ISO 14001環境マネジメントシステム

- メキシコ-ISO 45001労働安全衛生

- アルゼンチン-ISO 14001環境マネジメントシステム

- 中東・アフリカ

- UAE-ISO 14001環境マネジメントシステム

- 南アフリカ-ISO 45001労働安全衛生

- サウジアラビア-ISO 14001環境マネジメントシステム

- 北米

- ポーター分析

- PESTEL分析

- 技術とイノベーションの動向

- 現在の技術動向

- 新興技術

- 生産統計

- 生産拠点

- 消費拠点

- 輸出と輸入

- コスト内訳分析

- 開発コスト構造

- 研究開発コスト分析

- マーケティング及び販売コスト

- 特許分析

- 持続可能性と環境面

- 持続可能な実践

- 廃棄物削減戦略

- 生産におけるエネルギー効率

- 環境配慮型イニシアチブ

- 将来の市場展望と機会

- OEMの設計所有権と調達意思決定の枠組み

- OEM指定型とサプライヤー設計型のヒートシールド

- コスト、重量、熱性能のトレードオフ

- プラットフォームレベルでの調達戦略

- 軽量化と材料置換の動向

- 金属から複合材への動向

- 軽量化とコスト感度のバランス

- 自動車メーカーのCO2規制対応戦略への影響

- 先進材料の採用障壁

- EVが熱シールドの構成と設計進化に与える影響

- 内燃機関車・ハイブリッド車・電気自動車におけるヒートシールド需要の変化

- バッテリー、インバーター及びパワーエレクトロニクス用シールドの必要性

- 車両あたりの純含有量変化

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ地域

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

- 主な発展

- 合併・買収

- 提携・協業

- 新製品の発売

- 事業拡大計画と資金調達

第5章 市場推計・予測:製品別、2022-2035

- シングルシェル

- 二重殻

- サンドイッチ

第6章 市場推計・予測:車両別、2022-2035

- 乗用車

- ハッチバック

- セダン

- SUV

- 商用車

- 軽商用車(LCV)

- MCV

- 大型商用車(HCV)

第7章 市場推計・予測:材料別、2022-2035

- 金属

- セラミック

- 複合材料

第8章 市場推計・予測:推進力別、2022-2035

- 内燃機関(ICE)

- ハイブリッド

- 電気式

- BEV(バッテリー式電気自動車)

- 燃料電池自動車(FCEV)

- PHEV

第9章 市場推計・予測:販売チャネル別、2022-2035

- OEM

- アフターマーケット

第10章 市場推計・予測:用途別、2022-2035

- アンダーボディ・ヒートシールド

- エンジン

- 排気

- ターボチャージャー

- 伝送

- その他

第11章 市場推計・予測:地域別、2022-2035

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- ロシア

- 北欧諸国

- ポルトガル

- クロアチア

- ベネルクス

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- シンガポール

- タイ

- インドネシア

- ベトナム

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- コロンビア

- 中東・アフリカ地域

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

- トルコ

第12章 企業プロファイル

- 世界プレイヤー

- Autoneum

- Dana

- ElringKlinger

- Freudenberg Sealing Technologies

- Morgan Advanced Materials

- Sumitomo Riko

- Carcoustics

- UGN

- Adler Pelzer

- Toyoda Gosei

- Nihon Tokushu Toryo

- 地域プレイヤー

- Boyd

- Frenzelit

- Happich

- Talbros

- Design Engineering

- Thermo-Tec Automotive

- Sekisui Chemical

- Sika Automotive

- Trelleborg Automotive

- Emerging/Disruptor Players

- Alpha Engineered Components

- Anhui Parker New Material

- Heatshield Products

- Zircotec

- Pyrotek Automotive Thermal Solutions

- Unifrax