|

市場調査レポート

商品コード

1833661

スリープテックデバイスの市場機会、成長促進要因、産業動向分析、2025年~2034年予測Sleep Tech Devices Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| スリープテックデバイスの市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年09月02日

発行: Global Market Insights Inc.

ページ情報: 英文 170 Pages

納期: 2~3営業日

|

概要

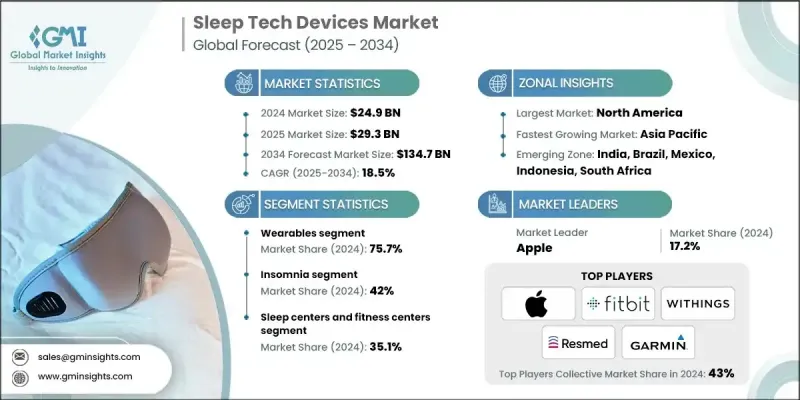

Global Market Insights Inc.が発行した最新レポートによると、世界のスリープテックデバイス市場は2024年に249億米ドルと推定され、CAGR 18.5%で2025年の293億米ドルから2034年には1,347億米ドルに成長すると予測されています。

様々な健康調査によると、現在、成人人口のかなりの部分が睡眠の質の低下や睡眠時間の不足を経験しており、多くの場合、正式に診断されていないです。このような過小診断が、個人の自己モニタリングと早期対策を可能にする、消費者向けの非侵襲性機器の需要をさらに押し上げています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 市場規模 | 249億米ドル |

| 予測金額 | 1,347億米ドル |

| CAGR | 18.5% |

ウェアラブルの普及拡大

ウェアラブル分野は2024年に注目すべきシェアを占めました。消費者は、睡眠パターン、心拍変動、酸素飽和度を夜通しモニターするために、スマートウォッチ、フィットネスバンド、その他のセンサー付きウェアラブルにますます目を向けるようになっています。この需要は、日常生活にシームレスにフィットする、継続的で非侵襲的な健康追跡への要望が主な要因となっています。センサー精度の向上とAIを活用した分析により、ウェアラブルは基本的な睡眠トラッカーから総合的なウェルネス・コンパニオンへと進化しつつあります。

不眠症の有病率の増加

何百万人もの人々が慢性的な睡眠の開始と維持の問題に悩まされているため、不眠症セグメントは2034年まで適正なCAGRで成長します。スマート枕、認知行動療法(CBT)ベースのアプリ、ノイズ・マスキング・デバイスなど、この市場に合わせたスリープテックデバイスが消費者と臨床医の双方から支持を得ています。その焦点は、副作用なしに睡眠の質を高める、薬物を使わない個別化ソリューションの提供にあります。主要企業は、より良い睡眠衛生と長期的な行動変容を促進する実用的な洞察を提供しながら、不眠症の根本原因に対処するため、エビデンスに基づく機能とデジタル治療法に投資しています。

睡眠センターとフィットネスセンターが牽引役に

2024年には、睡眠センターとフィットネスセンターが大きなシェアを占める。睡眠ラボは、睡眠研究を合理化し、臨床結果を改善するために、高度なモニタリングシステム、AIを活用した診断、コネクテッドデバイスの採用を増やしています。同時に、フィットネスセンターは、睡眠の質、身体パフォーマンス、疲労回復の直接的な関連性を認識し、より広範なウェルネスプログラムの一環として睡眠追跡サービスを統合しています。このようなパートナーシップは、メーカーに新たなB2B収益源を開き、睡眠技術の医療用とライフスタイル用アプリケーションが共存・繁栄できるハイブリッド・エコシステムを構築しています。

北米が推進力のある地域となる

北米スリープテックデバイス市場は、高い消費者意識、高度なヘルスケア・インフラ、個別化されたウェルネス・ソリューションに対する強い需要に後押しされ、2034年までに大きな収益を上げると予想されます。特に米国は、睡眠障害や慢性的な健康状態の割合が増加しており、消費者グレードと臨床グレードの両方の機器に対する継続的な需要を生み出していることから、同地域の収益の大部分を占めています。北米市場は、医療機器に対する有利な償還政策、ウェアラブル技術の革新、デジタルヘルスプラットフォームの拡大に支えられ、今後も安定した成長が見込まれます。

スリープテックデバイス市場の主要プレーヤーは、Smart Nora、Fitbit、BedJet、Withings、ResMed、Emfit、Oura Health、SleepScore Labs、Somnofy、Balluga、ChiliSleep、Apple、ReST、Itamar Medical、Huawei、Somnox、Pulsetto、Philips、Garmin、Eight Sleep、Xiaomi、Fisher &Paykel Healthcareです。

スリープテックデバイス市場における足場を固めるため、主要企業は戦略的パートナーシップ、製品イノベーション、標的を絞った買収を組み合わせて採用しています。多くの企業は、AIと機械学習を統合してより深い洞察と予測分析を提供し、ユーザーエンゲージメントと臨床的関連性を高めることに注力しています。また、健康アプリやスマートホームプラットフォームとの相互運用性を通じてエコシステムを拡大している企業もあります。ブランドの差別化は、消費者への直接販売モデル、インフルエンサーマーケティング、サブスクリプションベースのサービスモデルを通じても達成されつつあります。さらに、ヘルスケアプロバイダーや睡眠クリニックとの提携は、企業が新たな患者層や償還チャネルを開拓しながら、自社の製品を検証するのに役立っています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 業界への影響要因

- 促進要因

- スリープテックデバイスにおける技術の進歩

- スリープテックデバイスの可用性に関する認知度の向上

- 高齢化人口の増加

- ポータブルで効率的で優れたスリープテックデバイスへの需要の高まり

- 主要な市場参入企業による製品イノベーションとさまざまな戦略の採用

- 業界の潜在的リスク&課題

- スリープテックデバイスの高コスト

- 厳格な規制枠組み

- 市場機会

- 遠隔医療および遠隔患者モニタリングとの統合

- メンタルヘルスとウェルネス分野への拡大

- 促進要因

- 成長可能性分析

- 規制情勢

- テクノロジーとイノベーションの情勢

- 現在の技術動向

- 新興技術

- サプライチェーン分析

- 消費者行動の傾向

- 市場参入戦略分析

- ポーター分析

- ブランド分析

- トップ企業のビジネスモデル

- りんご

- レスメド

- PESTEL分析

- 将来の市場動向

- ギャップ分析

- 価格分析、2024

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- グローバル

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画

第5章 市場推計・予測:製品別、2021-2034

- 主要動向

- ウェアラブル

- スマートウォッチとバンド

- その他のウェアラブル

- ウェアラブル以外のも

- 睡眠モニター

- スマートベッド

第6章 市場推計・予測:用途別、2021-2034

- 主要動向

- 閉塞性睡眠時無呼吸症

- 不眠症

- ナルコレプシー

- その他の用途

第7章 市場推計・予測:流通チャネル別、2021-2034

- 主要動向

- 睡眠センターとフィットネスセンター

- ハイパーマーケットとスーパーマーケット

- eコマース

- 薬局および小売店

- その他の流通チャネル

第8章 市場推計・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋地域

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第9章 企業プロファイル

- Apple

- Balluga

- BedJet

- ChiliSleep

- Eight Sleep

- Emfit

- Fisher &Paykel Healthcare

- Fitbit

- Garmin

- Huawei

- Itamar Medical

- Oura Health

- Philips

- Pulsetto

- ResMed

- ReST

- SleepScore Labs

- Smart Nora

- Somnofy

- Somnox

- Withings

- Xiaomi