|

市場調査レポート

商品コード

1885917

耐久性医療機器市場の機会、成長要因、業界動向分析、および2025年から2034年までの予測Durable Medical Equipment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 耐久性医療機器市場の機会、成長要因、業界動向分析、および2025年から2034年までの予測 |

|

出版日: 2025年11月20日

発行: Global Market Insights Inc.

ページ情報: 英文 130 Pages

納期: 2~3営業日

|

概要

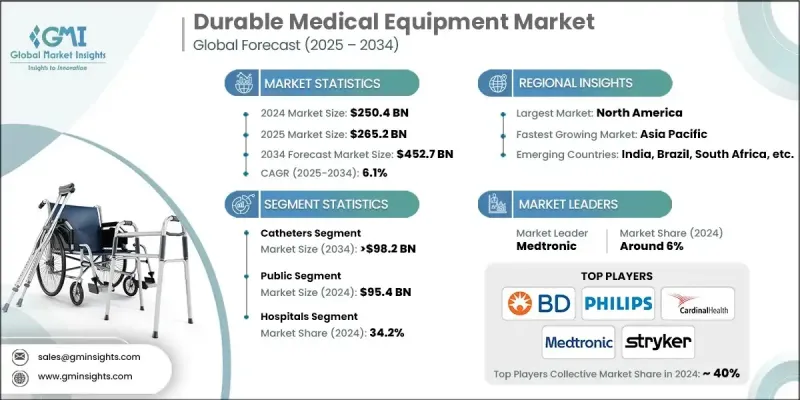

世界の耐久性医療機器市場は、2024年に2,504億米ドルと評価され、2034年までにCAGR6.1%で成長し、4,527億米ドルに達すると予測されています。

市場成長は、世界の慢性疾患の増加、医療技術の進歩、在宅医療への需要拡大、そして支援的な償還政策によって牽引されています。リハビリテーションや患者中心のケア、人間工学に基づいた使いやすい機器への注目が高まっていることも、需要をさらに後押ししています。高齢化もまた、専門機器の必要性を高める要因となっています。企業は製品革新を積極的に推進し、新素材の統合や地域パートナーシップの構築を通じて地理的拡大を図っています。技術統合が市場の核心的促進要因となりつつあり、無線モニタリング、AIを活用した診断、モバイルアプリ接続機能を備えた機器により、リアルタイムのデータ共有と個別化されたケアが可能となっています。医療がデジタル化および価値ベースモデルへ移行する中、技術強化されたDMEは効率的で患者中心の治療にますます重要となり、差別化と市場成長の新たな機会を開いています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測期間 | 2025-2034 |

| 開始時価値 | 2,504億米ドル |

| 予測金額 | 4,527億米ドル |

| CAGR | 6.1% |

カテーテル分野は、外科手術や泌尿器関連治療の増加を背景に、2024年には22.3%のシェアを占めました。カテーテルは体液の排出、薬剤投与、循環器系へのアクセス確保において重要な役割を果たします。特に尿閉、心血管疾患、透析治療中の患者様を中心に、病院、長期療養施設、在宅医療の現場で広く活用されています。

公的保険者セグメントは2024年に954億米ドルと評価されました。公的保険者には、被保険者への給付を提供する政府支援の医療プログラムや保険プランが含まれます。これらは一括価格交渉を行い、費用対効果の高い必須DME(耐久医療機器)を重視する傾向があります。公的保険者は、特に低所得地域や地方におけるアクセス拡大において極めて重要であり、償還政策が製品の入手可能性と市場需要に直接影響を与えます。

北米の耐久医療機器市場は、先進的な医療インフラ、高い医療支出、そして高齢人口の多さにより、2024年に大きなシェアを占めました。糖尿病、心血管疾患、呼吸器疾患などの慢性疾患の有病率の高さが、長期にわたる機器の使用を促進しています。在宅医療やデジタルヘルス技術の普及拡大により、携帯可能で接続機能を備えたデバイスの需要が加速しています。メディケアやメディケイドを含む政府の取り組みは、特に高齢者や障がい者層を対象に、必須DME製品へのアクセスをさらに支援しています。

よくあるご質問

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 業界への影響要因

- 促進要因

- 在宅医療に対する患者の選好の高まり

- 世界の慢性疾患の増加傾向

- 高齢化人口の増加

- 製品における技術的進歩

- 業界の潜在的リスク&課題

- 高額な医療機器コストと手頃な価格への課題

- 小児向け製品に対する需要の増加

- 機会

- AI/機械学習の統合と予測分析

- 新興市場における事業拡大とインフラ整備

- 促進要因

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋地域

- 技術とイノベーションの動向

- 現在の技術動向

- 新興技術

- 投資環境

- 償還シナリオ

- 医療提供モデルの変革

- 個別化医療および精密医療の応用

- ソフトウェアとしての医療機器(SaMD)統合分析

- ポーター分析

- PESTEL分析

- ギャップ分析

- 将来の市場動向

第4章 競合情勢

- イントロダクション

- 企業マトリックス分析

- 企業の市場シェア分析

- 世界

- 北米

- 欧州

- アジア太平洋地域

- LAMEA

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併・買収

- 提携・協業

- 新製品の発売

- 拡大計画

第5章 市場推計・予測:製品別、2021-2034

- 主要動向

- 個人用移動補助具

- 車椅子とスクーター

- 松葉杖と杖

- 歩行器

- その他の個人用移動補助具

- モニタリング・治療機器

- 酸素供給機器

- 血糖測定器

- バイタルサインモニター

- 輸液ポンプ

- 持続的気道陽圧(CPAP)装置

- ネブライザー

- その他のモニタリング・治療機器

- 浴室安全装置

- 医療用家具

- 失禁用パッド

- 搾乳器

- カテーテル

- 消耗品および付属品

- その他の製品

第6章 市場推計・予測:支払主体別、2021-2034

- 主要動向

- 公的保険

- 民間

- 自己負担

第7章 市場推計・予測:最終用途別、2021-2034

- 主要動向

- 病院

- 在宅医療

- 外来手術センター

- その他の用途

第8章 市場推計・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋地域

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ地域

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第9章 企業プロファイル

- B Braun

- Baxter

- BD

- Cardinal Health

- CAREX

- Coloplast

- COMPASS HEALTH

- convaTec

- drive DeVilbiss Healthcare

- Getinge

- graham-field

- INTCO MEDICAL

- INVACARE

- Koninklijke Philips

- MEDLINE

- Medtronic

- ResMed

- Stryker

- SUNRISE MEDICAL