|

市場調査レポート

商品コード

1892747

腹腔鏡手術器具市場の機会、成長要因、業界動向分析、および2026年から2035年までの予測Laparoscopic Instruments Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

カスタマイズ可能

|

|||||||

| 腹腔鏡手術器具市場の機会、成長要因、業界動向分析、および2026年から2035年までの予測 |

|

出版日: 2025年12月11日

発行: Global Market Insights Inc.

ページ情報: 英文 150 Pages

納期: 2~3営業日

|

概要

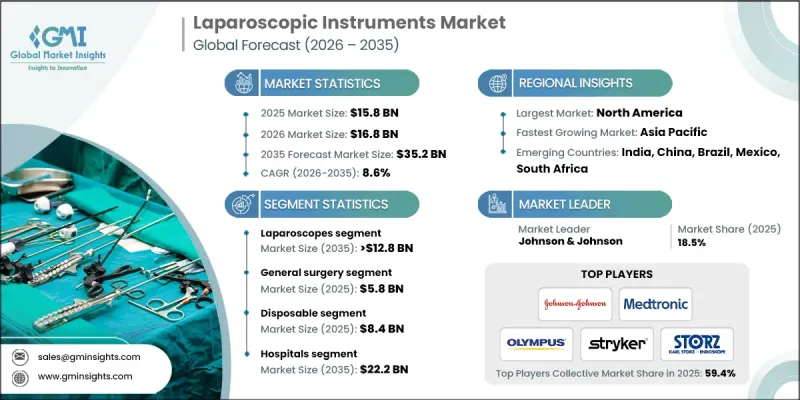

世界の腹腔鏡手術器具市場は、2025年に158億米ドルと評価され、2035年までにCAGR8.6%で成長し、352億米ドルに達すると予測されております。

市場成長は、低侵襲手術の普及拡大、外科的介入を必要とする慢性疾患の増加、および腹腔鏡機器の技術的進歩によって牽引されています。腹腔鏡手術器具は、トロカール、把持器、鋏、解剖器、エネルギーベースのデバイスなど、小さな腹部切開を通じて行われる処置用に設計された専門的な外科用器具です。これらの器具は精密な内部操作を可能にし、視認性とアクセス性を向上させると同時に、患者の外傷、回復時間、合併症リスクを低減します。肥満、消化器系、泌尿器系、大腸直腸疾患の症例増加に伴い、腹腔鏡手術に依存する手術件数が増加しています。関節式器具、高精細・3D/4K視覚化システム、エネルギーベース技術、ワイヤレスカメラなどの革新により、手術の精度と人間工学的特性が向上しています。さらに、AI支援画像診断やロボット支援腹腔鏡手術が、世界中の手術室における先進機器の導入を後押ししています。

| 市場範囲 | |

|---|---|

| 開始年 | 2025年 |

| 予測年度 | 2026-2035 |

| 開始時価値 | 158億米ドル |

| 予測金額 | 352億米ドル |

| CAGR | 8.6% |

エネルギーデバイス分野は2025年に34億米ドルの市場規模を記録し、2026年から2035年にかけてCAGR 8.8%で成長すると予測されています。外科医が手術効率の向上を図るため、精密な組織の密封・切断技術への依存度を高めていることから、これらの機器に対する需要は高い水準にあります。手術時間の短縮と患者安全性の向上を両立させる先進的な超音波システムやバイポーラシステムの導入拡大が、本分野の成長に寄与しています。

一般外科分野は2025年に58億米ドルを占め、2035年までCAGR 8.9%で成長すると予想されます。ヘルニア修復術、虫垂切除術、胆嚢摘出術などの分野における高い手術件数が、腹腔鏡器具に対する継続的な需要を牽引し続けています。視覚化技術、人間工学に基づいた設計、関節式器具の進歩により腹腔鏡手術はより安全かつ効率的となり、病院は最新機器への投資を進めています。

米国腹腔鏡器具市場は2025年に63億米ドルと評価されました。北米における低侵襲手術の普及は、患者転帰の改善、入院期間の短縮、合併症の減少によって推進されています。先進的な手術室を備えた病院や外来手術センターでは、エネルギー装置、把持器、視覚化ツールを含むハイエンド腹腔鏡システムの導入が進んでいます。ロボット支援プラットフォーム、統合型手術室、高度な画像診断システムへの投資が、同地域における市場成長を継続的に推進しております。

よくあるご質問

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 業界への影響要因

- 促進要因

- 消化器系および婦人科疾患の有病率の増加

- 低侵襲手術への選好の高まり

- 腹腔鏡装置における技術的進歩

- ロボット支援腹腔鏡手術の拡大

- 業界の潜在的リスク&課題

- 高度な腹腔鏡器具の高コスト

- 機器故障や合併症のリスク

- 市場機会

- 新興市場における導入拡大

- 再利用可能かつ持続可能な器具への需要増加

- 促進要因

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋地域

- 技術動向

- 現在の技術動向

- 新興技術

- 償還シナリオ

- 消費者洞察

- 将来の市場動向

- バリューチェーン分析

- ポーター分析

- PESTEL分析

- ギャップ分析

第4章 競合情勢

- イントロダクション

- 企業マトリックス分析

- 企業の市場シェア分析

- 世界

- 北米

- 欧州

- アジア太平洋地域

- 競合ポジショニングマトリックス

- 主要市場企業の競合分析

- 主な発展

- 合併・買収

- 提携・協業

- 新製品の発売

- 拡大計画

第5章 市場推計・予測:製品別、2022-2035

- 主要動向

- 腹腔鏡

- ビデオ腹腔鏡

- ファイバー腹腔鏡

- エネルギーデバイス

- 閉鎖装置

- 送気装置

- 手用器具

- アクセスデバイス

- 吸引システム

- 腹腔鏡用アクセサリー

第6章 市場推計・予測:用途別、2022-2035

- 主要動向

- 一般外科

- 婦人科手術

- 泌尿器外科

- 肥満外科手術

- 大腸肛門外科

- 小児外科

- その他の用途

第7章 市場推計・予測:用途別、2022-2035

- 主要動向

- 使い捨て

- 再利用可能

第8章 市場推計・予測:最終用途別、2022-2035

- 主要動向

- 病院

- 外来手術センター

- その他の用途

第9章 市場推計・予測:地域別、2022-2035

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋地域

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第10章 企業プロファイル

- B. BRAUN

- Boston Scientific

- CONMED

- COOK Medical

- FUJIFILM

- Intuitive Surgical

- Johnson &Johnson

- KARL STORZ

- Medtronic

- Microline Surgical

- OLYMPUS

- Richard Wolf

- Smith &Nephew

- Stryker

- VICTOR MEDICAL