|

市場調査レポート

商品コード

1892828

ガイドワイヤー市場における機会、成長要因、業界動向分析、および2025年から2034年までの予測Guidewires Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| ガイドワイヤー市場における機会、成長要因、業界動向分析、および2025年から2034年までの予測 |

|

出版日: 2025年12月05日

発行: Global Market Insights Inc.

ページ情報: 英文 188 Pages

納期: 2~3営業日

|

概要

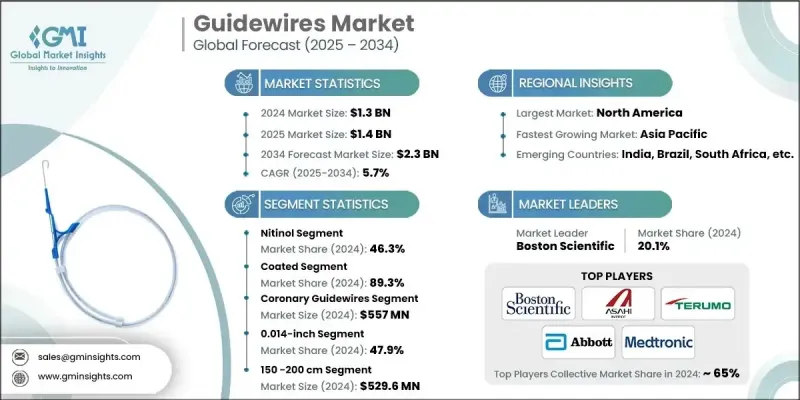

世界のガイドワイヤー市場は、2024年に13億米ドルと評価され、2034年までにCAGR5.7%で成長し、23億米ドルに達すると予測されています。

市場拡大の主な要因としては、高齢化人口の増加、生活習慣病の有病率上昇、先進国における医療保険制度の支援策、ならびに心血管疾患の罹患率上昇が挙げられます。さらに、スマートガイドワイヤーや生体吸収性モデルといった設計技術の進歩が、導入を促進しております。医療現場における従来の手術から、経皮的冠動脈インターベンション(PCI)、神経血管インターベンション、血管内治療などの低侵襲的処置への移行が、市場成長に大きく寄与しております。これらの処置は身体への負担を軽減し、入院期間を短縮し、回復を促進します。ガイドワイヤーは、複雑な血管構造を精密にナビゲートする上で臨床医を支援する重要な役割を担い、手技の成功率と患者の転帰を改善します。新興国における医療インフラの拡充も、ガイドワイヤー導入の新たな機会を創出しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測期間 | 2025-2034 |

| 開始時価値 | 13億米ドル |

| 予測金額 | 23億米ドル |

| CAGR | 5.7% |

2024年、ニチノールセグメントは46.3%のシェアを占めました。このセグメントは、有利な償還政策と、形状記憶特性や超弾性といった優れた材料特性により、心血管、末梢血管、神経血管の手術において複雑な血管内をナビゲートする際の柔軟性と屈曲抵抗性を高めることから、今後も成長を続けると予想されます。

コーティング済みセグメントは2024年に89.3%のシェアを占めました。親水性、抗血栓性、疎水性、シリコーンベースの技術を用いたコーティング済みガイドワイヤーは、その臨床効率とインターベンション処置における広範な使用から好まれています。

北米ガイドワイヤー市場は2024年に37.7%のシェアを占めました。同地域は、先進的な医療インフラ、高い手技実施件数、低侵襲的介入治療の急速な普及、継続的な技術革新の恩恵を受けています。心血管疾患、末梢動脈疾患、神経血管疾患、泌尿器疾患の高い有病率が、診断用および治療用ガイドワイヤーの需要を牽引しています。

よくあるご質問

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 業界への影響要因

- 促進要因

- 低侵襲手術手技の採用増加

- 途上国における生活習慣病の増加傾向

- 先進国における様々な償還政策

- 世界的に高齢化人口が増加傾向にあります

- 業界の潜在的リスク&課題

- ガイドワイヤーの高コスト

- 発展途上国における熟練専門家の不足

- ガイドワイヤーに関連するリスク

- 機会

- 新興経済国における医療インフラの拡充

- 画像誘導およびロボット支援インターベンションの採用拡大

- 促進要因

- 成長可能性分析

- 規制情勢

- 北米

- 米国

- カナダ

- 欧州

- 中国

- 北米

- 技術とイノベーションの動向

- 現在の技術動向

- 強化された親水性・疎水性コーティング技術

- トルク制御と操縦性最適化

- 多層複合材料の統合

- 新興技術

- ナノテクノロジー強化表面処理技術

- 磁気誘導ナビゲーションシステム

- 3Dプリントによる個別対応ガイドワイヤー試作品

- 現在の技術動向

- 将来の市場動向

- 完全統合型デジタルインターベンションスイートへの移行が加速

- 使い捨て・滅菌済み・コスト効率に優れたガイドワイヤーへの需要増加

- 低侵襲・外来ベースの治療法の拡大

- 償還シナリオ

- 地域別価格分析2024

- 素材別

- 用途別

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業マトリックス分析

- 企業の市場シェア分析

- 世界

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ地域

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併・買収

- 提携・協業

- 新製品の発売

- 拡大計画

第5章 市場推計・予測:材料別、2021-2034

- 主要動向

- ニチノール

- ステンレス鋼

- ハイブリッド

- その他の材料

第6章 市場推計・予測:コーティング別、2021-2034

- 主要動向

- コーティング

- 親水性コーティング

- 抗血栓性/ヘパリンコーティング

- 疎水性コーティング

- シリコーンコーティング

- テトラフルオロエチレン(TFE)コーティング

- 無コーティング

第7章 市場推計・予測:用途別、2021-2034

- 主要動向

- 冠動脈用ガイドワイヤー

- 末梢用ガイドワイヤー

- 泌尿器科用ガイドワイヤー

- 神経血管用ガイドワイヤー

- その他の用途

第8章 市場推計・予測:直径別、2021-2034

- 主要動向

- 0.014インチ

- 0.018インチ

- 0.025インチ

- 0.032インチ

- 0.035インチ

- 0.038インチ

第9章 市場推計・予測:長さ別、2021-2034

- 主要動向

- 80~145 cm

- 150~200 cm

- 210~300 cm

- 305cm以上

第10章 市場推計・予測:最終用途別、2021-2034

- 主要動向

- 病院

- 外来手術センター

- その他の用途

第11章 市場推計・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋地域

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ地域

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第12章 企業プロファイル

- Abbott Laboratories

- AngioDynamics

- ASAHI INTECC

- B. Braun SE

- Becton, Dickinson and Company

- Boston Scientific

- Cordis

- Cook Medical

- Medtronic

- Merit Medical Systems

- Olympus

- Stryker

- Teleflex

- Terumo