|

市場調査レポート

商品コード

1959657

非球面レンズ市場の機会、成長要因、業界動向分析、および2026年から2035年までの予測Aspherical Lens Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

カスタマイズ可能

|

|||||||

| 非球面レンズ市場の機会、成長要因、業界動向分析、および2026年から2035年までの予測 |

|

出版日: 2026年02月13日

発行: Global Market Insights Inc.

ページ情報: 英文 163 Pages

納期: 2~3営業日

|

概要

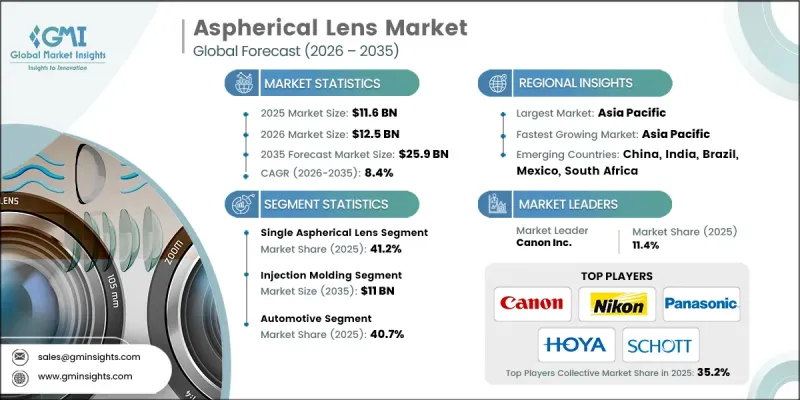

世界の非球面レンズ市場は、2025年に116億米ドルと評価され、2035年までにCAGR8.4%で成長し、259億米ドルに達すると予測されています。

この市場の成長は、戦略的提携によって促進されています。これにより、企業は新たな技術、流通ネットワーク、顧客セグメント、特に自動車用カメラや拡張現実(XR)デバイスなどの新興分野へのアクセスが可能となります。半導体製造を促進する政府の取り組みの増加も市場拡大を牽引しており、国家補助金、インセンティブプログラム、ファブ拡張政策がウェハー消費を加速させ、ウェハー再利用などのコスト効率の高い製造手法を促進しています。高度運転支援システム(ADAS)やLiDARの自動車への採用は重要な促進要因です。高精度非球面レンズは、光を正確に集光し光学歪みを低減することで、カメラやセンサーの性能を向上させます。インテリジェントで安全な車両への需要と、ADASに対する規制面の支援が相まって、自動車用途における先進的光学部品の採用をさらに促進しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2025年 |

| 予測年度 | 2026-2035 |

| 開始時価値 | 116億米ドル |

| 予測金額 | 259億米ドル |

| CAGR | 8.4% |

単一非球面レンズセグメントは、2025年に41.2%のシェアを占めました。これは、低コスト、簡素さ、統合の容易さによる人気の高さを反映しています。単一レンズは、軽量で精密な光学系が不可欠な民生用電子機器、スマートフォン、コンパクトカメラ、小型光学機器などで広く使用されています。そのコンパクトな設計と性能上の利点は、小型フォームファクターでの高解像度撮像を必要とする用途に最適です。

研磨・研削セグメントは2025年に38億米ドルと評価され、2026年から2035年にかけてCAGR7.4%で成長すると予測されています。これらの工程は、医療機器、科学機器、航空宇宙システムなどの要求の厳しい用途に使用される高精度レンズの製造に不可欠です。自動研磨およびコンピュータ制御による研削の技術進歩により、レンズの品質、精度、生産効率が向上し、メーカーはプレミアム光学機器に対する需要の高まりに対応することが可能となっています。

北米非球面レンズ市場は、2025年に27.6%のシェアを占めました。これは、民生用電子機器、自動車、医療、産業用途における非球面レンズの堅調な採用が牽引したものです。高精度光学機器の早期導入と技術革新が相まって、先進的なコーティング技術、小型化レンズ、コンパクト光学システムの開発が可能となっております。自動車分野におけるカメラ、イメージセンサー、光学機器の需要拡大が、同地域における非球面レンズの需要をさらに促進しており、北米は主要な成長拠点となっております。

よくあるご質問

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率分析

- コスト構造

- 各段階における付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- コンパクトで軽量な光学デバイスに対する需要の増加

- 市場プレゼンス拡大に向けた戦略的提携・パートナーシップ

- 自動車用ADASおよびLiDARシステムの拡大

- 産業用途における高性能光学システムへの需要増加

- 監視・セキュリティシステムの成長

- 業界の潜在的リスク&課題

- 高い製造・生産コスト

- 高品質な原材料の供給が限られていること

- 市場機会

- 小型化・高精度化が進む光学部品

- 医療用画像診断機器の拡大

- 促進要因

- 規制情勢

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- ポーターの分析

- PESTEL分析

- 技術とイノベーションの動向

- 現在の技術動向

- 新興技術

- 新興ビジネスモデル

- コンプライアンス要件

- 特許および知的財産分析

- 地政学的・貿易動向

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 地域別

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- 地域別

- 主要企業の競合ベンチマーキング

- 財務実績比較

- 収益

- 利益率

- 研究開発

- 製品ポートフォリオ比較

- 製品ラインの広さ

- 技術

- イノベーション

- 地理的プレゼンス比較

- 世界展開分析

- サービスネットワークのカバー率

- 地域別市場浸透率

- 競合ポジショニングマトリックス

- リーダー企業

- 課題者

- フォロワー

- ニッチプレイヤー

- 財務実績比較

- 主な発展, 2022-2025

- 合併・買収

- 提携および共同事業

- 技術的進歩

- 拡大と投資戦略

- デジタルトランスフォーメーションの取り組み

- 新興/スタートアップ競合の動向

第5章 市場推計・予測:レンズタイプ別、2022-2035

- 単一非球面レンズ

- 両面非球面レンズ

- 多面非球面レンズ

第6章 市場推計・予測:素材タイプ別、2022-2035

- ガラス

- プラスチック

- ハイブリッド

第7章 市場推計・予測:製造技術別、2022-2035

- 射出成形

- 研磨・研削

- その他

第8章 市場推計・予測:波長範囲別、2022-2035

- 紫外線(<400 nm)

- 可視光(400-700 nm)

- 近赤外線(700-1400 nm)

- 短波長/中波長赤外線(1,400 nm以上)

第9章 市場推計・予測:用途別、2022-2035

- 自動車

- 民生用電子機器

- デジタルカメラ

- スマートフォン

- その他

- 医療・医療機器

- 眼科光学

- 産業・計測

- 航空宇宙・防衛

- その他

第10章 市場推計・予測:地域別、2022-2035

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第11章 企業プロファイル

- 世界の主要企業

- Canon Inc.

- Nikon Corporation

- Panasonic Holdings Corporation

- Hoya Corporation

- SCHOTT

- Carl Zeiss AG

- FUJIFILM Corporation

- Konica Minolta, Inc.

- KYOCERA Corporation

- 地域別主要企業

- AGC Inc.

- ALPS ALPINE CO., LTD.

- Asahi Lite Optical Co., Ltd.

- Asia Optical Co., Inc.

- Shanghai Optics

- SUMITA OPTICAL GLASS, Inc.

- Tokai Optical Co. Ltd.

- Edmund Optics India Private Limited

- ニッチプレイヤー/ディスラプター

- Asphericon GmbH

- Avantier Inc.

- Calin Technology Co. Ltd.

- Hyperion Optics

- Jenoptik AG

- Knight Optical