|

市場調査レポート

商品コード

1871296

多がん種早期検出(MCED)検査市場の機会、成長要因、業界動向分析、2025年~2034年の予測Multi Cancer Early Detection (MCED) Test Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 多がん種早期検出(MCED)検査市場の機会、成長要因、業界動向分析、2025年~2034年の予測 |

|

出版日: 2025年10月28日

発行: Global Market Insights Inc.

ページ情報: 英文 130 Pages

納期: 2~3営業日

|

概要

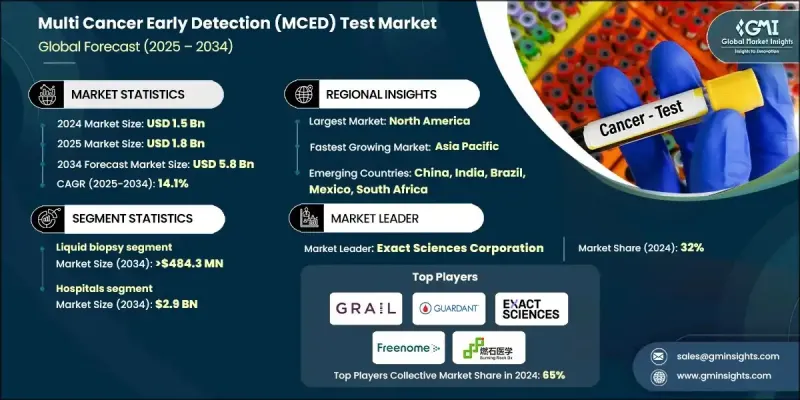

世界の多がん種早期検出(MCED)検査市場は、2024年に15億米ドルと評価され、2034年までにCAGR14.1%で成長し、58億米ドルに達すると予測されております。

世界的ながん罹患率の上昇、早期診断ソリューションへの需要増加、分子診断技術の急速な進歩により、市場は強い成長勢いを示しております。液体生検や次世代シーケンシング(NGS)などの手法を活用したMCED検査は、単一の血液サンプルから複数のがん種を検出可能とし、従来のスクリニング手法を再定義しております。これらの検査は、臨床医がより早期かつ包括的にがんを特定することを可能にし、腫瘍学を変革しています。各社は、液体生検技術の継続的な進歩、マルチオミクスデータの統合、AI駆動型分析を通じて検査の精度と臨床応用性を高め、幅広いがん種に対応する高感度・高特異性の診断ソリューションを創出しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測期間 | 2025年~2034年 |

| 開始時価値 | 15億米ドル |

| 予測金額 | 58億米ドル |

| CAGR | 14.1% |

遺伝子パネル、検査室開発検査(LDT)、およびその他の関連セグメントは、2034年までCAGR 14%で成長すると予測されています。このセグメントは、早期の商業化、特定の変異を標的とする柔軟性、ヘルスケア提供者や研究機関による採用により、市場を独占しています。これらの検査は、遺伝子変異、メチル化パターン、その他の分子シグネチャを分析し、複数のがん種にわたる個別化スクリーニングアプローチを支援します。

病院セグメントは2034年までに29億米ドルに達すると予測されています。病院は複雑な診断ワークフローと多職種連携医療の管理に最適であり、腫瘍専門医、病理医、遺伝学者が協力して検査結果を解釈します。このチームワークにより、正確な早期発見と治療計画のための実用的な知見が確保されます。予防ヘルスケアの取り組みが、このセグメントの重要性をさらに強化しています。

北米における多がん種早期検出(MCED)検査市場は、予防医療への高い意識、精密腫瘍学への堅調な投資、液体生検および遺伝子パネルベーススクリーニングの早期導入によって支えられています。同地域の先進的なヘルスケアインフラと早期診断への注力が、病院、検査機関、健康増進プログラム全体での需要を持続させています。

多がん種早期検出(MCED)検査市場の主要企業には、アンパック・バイオメディカル・サイエンス、バーニングロック・バイオテック、アーリーダイアグノスティックス、エリプタ、フリーノーム・ホールディングス、エクザクト・サイエンシズ・コーポレーション、ジェネキャスト・バイオテクノロジー、広州アンカーDxメディカル、ガーダント・ヘルス、ハービンジャー・ヘルス、グレイル、マイクロノマ、シークイン、シングラー・ゲノミクスなどが含まれます。市場をリードする企業は、検査精度向上のため、AI駆動型分析やマルチオミクス統合といった先進的診断技術への投資を通じて存在感を強化しております。臨床連携の積極的拡大、研究機関とのパートナーシップ強化、規制当局の承認取得に注力し、検査の普及促進を図っております。液体生検や遺伝子パネル検査における継続的な革新と早期商業化戦略により、企業は新たな市場を獲得しています。さらに、ヘルスケア従事者や患者様へのMCED検査の利点に関する啓発活動を優先し、予防医療キャンペーンへの投資、病院・検査機関・健康増進プログラム全体での広範な利用を保証するための流通経路の最適化に取り組んでいます。

よくあるご質問

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- バリューチェーンに影響を与える要因

- 業界への影響要因

- 促進要因

- がん罹患率の増加

- 高いがん検出率と効果的ながん診断ツールへの需要増加

- がん検診に活用されるデータ分析および人工知能(AI)の進歩

- 業界の潜在的リスク&課題

- 多がんスクリーニング検査の高コスト

- 市場機会

- 予防医療および集団健康管理プログラムへの拡大

- 促進要因

- 成長可能性分析

- 規制情勢

- 技術情勢

- 現在の技術動向

- 新興技術

- 将来の市場動向

- 価格分析、2024年

- 特許分析

- 償還シナリオ

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 世界

- 北米

- 欧州

- 企業マトリクス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併・買収

- 提携および協力関係

- 新製品の発売

- 拡大計画

第5章 市場推計・予測:タイプ別、2021年~2034年

- 主要動向

- 遺伝子パネル、LDTおよびその他

- 液体生検

第6章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 病院

- 診断検査室

- その他の用途

第7章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第8章 企業プロファイル

- AnPac Bio-Medical Science

- Burning Rock Biotech

- EarlyDiagnostics

- Elypta

- EXACT SCIENCES CORPORATION

- Freenome Holdings

- Genecast Biotechnology

- Guangzhou AnchorDx Medical

- GUARDANT HEALTH

- Harbinger Health

- GRAIL

- Micronoma

- SeekIn

- Singlera Genomics