|

市場調査レポート

商品コード

1982301

安全弁市場の機会、成長要因、業界動向分析、および2026年~2035年の予測Safety Valves Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

カスタマイズ可能

|

|||||||

| 安全弁市場の機会、成長要因、業界動向分析、および2026年~2035年の予測 |

|

出版日: 2026年02月16日

発行: Global Market Insights Inc.

ページ情報: 英文 180 Pages

納期: 2~3営業日

|

概要

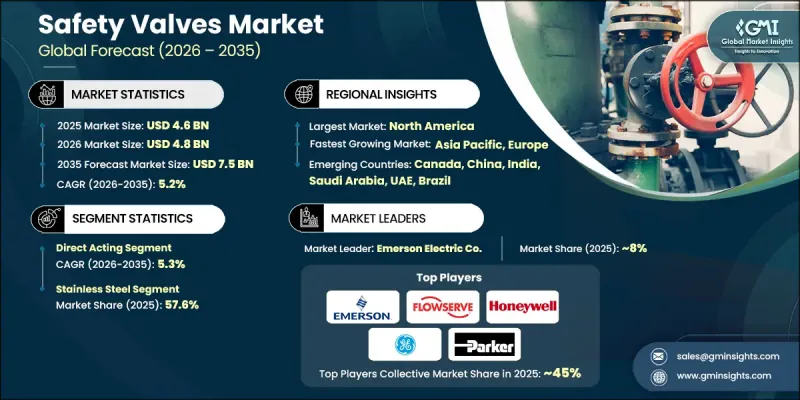

世界の安全弁市場は、2025年に46億米ドルと評価され、CAGR 5.2%で成長し、2035年までに75億米ドルに達すると推定されています。

近年、安全規制の強化、産業インフラの近代化、および重要産業における高圧処理システムの導入拡大に支えられ、市場の成長は堅調に推移しています。産業活動の複雑化や規制枠組みの厳格化に伴い、企業は信頼性の高い過圧保護システムをより重視するようになっています。安全弁は、圧力に関連する故障を未然に防ぐことで、設備、人員、および生産の継続性を守る不可欠な構成要素としての役割を果たし続けています。プラントのアップグレードへの投資拡大、老朽化した産業資産の拡張、そして運用信頼性への注目の高まりが、世界の需要を後押ししています。パイロット作動式システム、高圧直動式モデル、ベローズシール設計などの高度な構成が、進化するプロセス要件を満たすために広く採用されつつあります。しかし、技術的に高度なバルブシステムの導入は、資本集約的であることおよび大規模な施設要件が必要なことから、依然として課題となっています。こうした制約があるにもかかわらず、持続的な工業化とコンプライアンス主導の調達戦略が、安全弁市場の長期的な成長を牽引し続けています。

| 市場の範囲 | |

|---|---|

| 開始年 | 2025年 |

| 予測期間 | 2026年~2035年 |

| 開始時の市場規模 | 46億米ドル |

| 予測額 | 75億米ドル |

| CAGR | 5.2% |

直動式バルブセグメントは2025年に21億米ドルの市場規模を記録し、2026年から2035年にかけてCAGR 5.3%で成長すると予測されています。このカテゴリーは、シンプルな設計、信頼性の高い性能、および低圧から中圧システムへの適応性により、市場をリードしています。一般的な産業プロセスへの幅広い適合性により、メンテナンスや交換サイクルにおける安定した需要が支えられています。事業者が標準化された圧力保護フレームワークや規制遵守要件への適合をますます進める中、直動式バルブは、費用対効果が高く信頼性の高い安全管理のための最適なソリューションであり続けています。

ステンレス鋼セグメントは57.6%のシェアを占め、2025年には26億米ドルの市場規模を記録しました。ステンレス鋼製安全弁は、耐食性、構造強度、および高温・高圧条件下での性能が評価され、広く採用されています。過酷な稼働環境下での耐久性により、厳格なコンプライアンスと運用上の強靭性が求められる産業において不可欠な存在となっています。要求の厳しい処理システムの導入拡大に伴い、世界中でステンレス鋼製弁の採用が加速し続けています。

米国の安全弁市場は2025年に9億4,240万米ドルに達し、2026年から2035年にかけてCAGR 5.4%で成長すると予測されています。地域的な需要は、継続的な設備更新プログラム、施設のアップグレード、および定期的なメンテナンスサイクルによって支えられています。トレーサビリティ、認証、および厳格な安全基準の遵守に対する重視の高まりにより、購入者は耐食性材料や信頼できるOEMメーカーを優先するようになっています。規制順守と運用効率への注力が、産業セクター全体で安定した調達量を維持し続けています。

よくあるご質問

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- 各段階における付加価値

- バリューチェーンに影響を与える要因

- 業界への影響要因

- 促進要因

- 高度な安全弁システムのコスト上昇

- 多様な安全弁技術および用途特化型システムの普及が進んでいます

- 産業事業者における財務的負担を軽減する必要性の高まり

- 業界の潜在的リスク&課題

- 産業の近代化および設備更新に対する政府補助金

- 標準化された規制やプロセス安全の枠組みの欠如

- 業界の機会

- デジタルおよび精密技術に基づく安全技術の採用拡大

- デジタルプラットフォームおよびオンデマンド型産業安全サービスの拡大

- 促進要因

- 成長可能性分析

- 将来の市場動向

- 技術およびイノベーションの動向

- 現在の技術動向

- 新興技術

- 価格動向

- 地域別

- 製品タイプ別

- 規制情勢

- 規格およびコンプライアンス要件

- 地域別の規制枠組み

- 認証基準

- ポーターの分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 地域別

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- 地域別

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併・買収

- 提携・協業

- 新製品の発売

- 事業拡大計画

第5章 安全弁市場推計・予測:タイプ別、2022-2035

- 直動式

- ベローズ

- パイロット作動式

第6章 安全弁市場推計・予測:材料別、2022-2035

- ステンレス鋼

- 炭素鋼

- 真鍮

- プラスチック

- その他(インコネルなど)

第7章 安全弁市場推計・予測:サイズ別、2022-2035

- 1インチ以下

- 1インチ~6インチ

- 6インチ~25インチ

- 25インチ~50インチ

- 50インチ以上

第8章 安全弁市場推計・予測:圧力範囲別、2022-2035

- 35MPa未満

- 35~70 MPa

- 70~110 MPa

- 400 MPa

- 700 MPa

- 20 kpsi

- 60 kpsi

第9章 安全弁市場推計・予測:エンドユーザー別、2022-2035

- 石油・ガス

- 上下水道処理

- 電力業界

- 化学産業

- その他

第10章 安全弁市場推計・予測:流通チャネル別、2022-2035

- 直接販売

- 間接販売

第11章 安全弁市場推計・予測:地域別、2022-2035

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- ラテンアメリカ

- ブラジル

- メキシコ

- 中東・アフリカ(MEA)

- サウジアラビア

- アラブ首長国連邦

第12章 企業プロファイル

- Burkert Fluid Control Systems

- Cameron

- Crane Co.

- Emerson Electric Co.

- Flowserve Corporation

- GE Measurement &Control Solutions

- Honeywell International Inc.

- Moog Inc.

- Parker Hannifin Corporation

- Pentair plc

- Rotork Plc

- Schneider Electric SE

- Spirax Sarco Limited

- ValvTechnologies, Inc.

- Watts Water Technologies, Inc.