|

市場調査レポート

商品コード

1876802

自動車用半導体市場の機会、成長要因、業界動向分析、および2025年から2034年までの予測Automotive Semiconductor Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 自動車用半導体市場の機会、成長要因、業界動向分析、および2025年から2034年までの予測 |

|

出版日: 2025年11月04日

発行: Global Market Insights Inc.

ページ情報: 英文 170 Pages

納期: 2~3営業日

|

概要

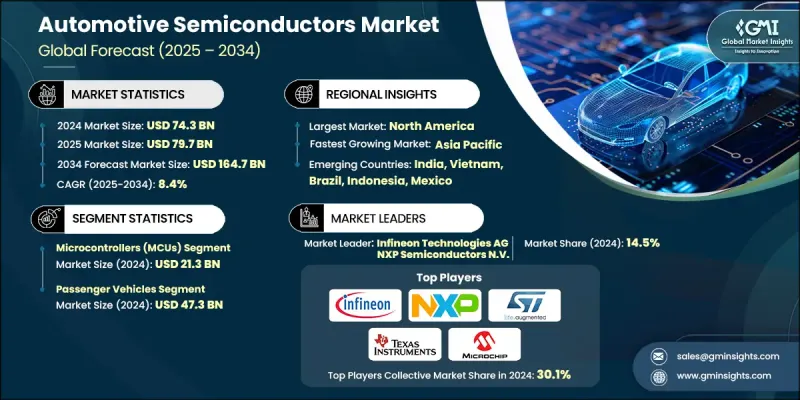

世界の自動車用半導体市場は、2024年に743億米ドルと評価され、2034年までにCAGR8.4%で成長し、1,647億米ドルに達すると予測されています。

電気自動車の普及拡大とパワートレイン技術の継続的な進化が相まって、自動車用半導体の需要を牽引しております。車両の電動化が進む中、ADAS(先進運転支援システム)や自動運転システムの急速な発展が、自動車の安全性や運用効率を変革しております。インフォテインメントシステム、車両接続ソリューション、V2X通信の統合が進むことで、半導体の採用がさらに加速しております。さらに、排出ガス規制や規制基準の強化により、自動車メーカーは燃費向上と排出ガス削減のため、半導体ベースの制御システムの導入を迫られています。電気化・知能化モビリティへの世界的な移行は、エネルギー変換、バッテリー管理、車両知能化において重要な役割を担う半導体チップが、よりスマートで持続可能な自動車エコシステムを支えることで、半導体業界の構造を再構築し続けています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測期間 | 2025-2034 |

| 開始時価値 | 743億米ドル |

| 予測金額 | 1,647億米ドル |

| CAGR | 8.4% |

マイクロコントローラー分野は、2024年に213億米ドルの規模に達しました。自動車、特に電気自動車やADAS搭載モデルにおける電子機器の増加に伴い、高性能な自動車用マイクロコントローラーの需要は引き続き高まっています。これらの部品は、パワートレイン制御、バッテリー管理、エアバッグ、インフォテインメント、ドメインコントローラーなどのシステムに不可欠です。ソフトウェア定義車両(SDV)の台頭に伴い、MCUへの依存度は拡大しています。MCUは、複数のサブシステムにわたる高速なリアルタイムコンピューティングと高度な車両協調を実現するからです。

小型商用車(LCV)セグメントは、2034年までにCAGR 7.9%で成長すると予測されています。都市配送車両の電動化とコネクテッドテレマティクスの統合が、この成長の主要な要因です。クラス2商用車の生産増加と、フリートの持続可能性への注目の高まりが、LCVの電動化とデジタル監視向けに設計された半導体に対する安定した需要を生み出しています。

米国自動車半導体市場は2024年に174億米ドルの規模に達しました。電気自動車の普及加速に加え、政府の優遇措置や厳格な規制枠組みが、国内全体の半導体需要を牽引しています。メーカー各社は、ゾーン別E/Eアーキテクチャに関するOEMの要求に応えるため研究開発戦略を見直し、安全性と信頼性に関するAEC-Q100 Grade 1規格を満たす先進的なAI・MLベースのプロセッサを開発中です。

世界の自動車用半導体市場で事業を展開する主要企業には、ZFフリードリヒスハーフェンAG、ルネサスエレクトロニクス株式会社、STマイクロエレクトロニクスN.V.、インフィニオン・テクノロジーズAG、アナログ・デバイセズ社、NXPセミコンダクターズN.V.、ローム株式会社、アドバンスト・マイクロ・デバイセズ、コンチネンタル、東芝、テキサス・インスツルメンツ社、タワー・セミコンダクター社、TEコネクティビティ、マイクロチップ・テクノロジー社、オンセミ、メレクシスN.V.、ロバート・ボッシュGmbH、マイクロン・テクノロジー、アレグロ・マイクロシステムズなどが挙げられます。主要企業は、市場での地位を強化するため、イノベーション、戦略的提携、生産能力の拡大に注力しております。電気自動車および自動運転車のアーキテクチャをサポートするチップの開発に多大な投資を行い、エネルギー効率と処理速度の向上を図っております。自動車メーカー(OEM)やティア1サプライヤーとの提携は、新興の車両プラットフォームに合わせた製品開発の実現に貢献しております。

よくあるご質問

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- バリューチェーンに影響を与える要因

- 利益率分析

- ディスラプション

- 将来の展望

- 製造業者

- 販売代理店

- 影響要因

- 促進要因

- 電動化とパワートレインの進化が自動車用半導体の需要を牽引しております

- ADAS(先進運転支援システム)および自動運転への注目の高まり

- インフォテインメントシステムと車載ネットワークの統合の進展

- 接続性とV2X(車両とあらゆるものとの通信)に対する需要の高まり

- 規制圧力と排出基準の厳格化が半導体導入を加速させております

- 業界の潜在的リスク&課題

- サプライチェーンの混乱

- 高い研究開発費およびコンプライアンスコスト

- 促進要因

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- ポーター分析

- PESTEL分析

- 技術とイノベーションの動向

- 現在の技術動向

- 新興技術

- 新興ビジネスモデル

- コンプライアンス要件

- 持続可能性対策

- 特許および知的財産分析

- 地政学的および貿易動向

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 地域別

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- 市場集中度分析

- 地域別

- 主要企業の競合ベンチマーキング

- 財務実績比較

- 収益

- 利益率

- 研究開発

- 製品ポートフォリオ比較

- 製品ラインの幅広さ

- 技術

- イノベーション

- 地域別プレゼンス比較

- グローバル展開分析

- サービスネットワークカバレッジ

- 地域別市場浸透率

- 競合ポジショニングマトリックス

- リーダー企業

- 課題者

- フォロワー

- ニッチプレイヤー

- 戦略的展望マトリックス

- 財務実績比較

- 主な発展, 2021-2024

- 合併・買収

- 提携および協力関係

- 技術的進歩

- 拡大および投資戦略

- サステナビリティ施策

- デジタルトランスフォーメーションの取り組み

- 新興/スタートアップ競合の動向

第5章 市場推計・予測:構成要素タイプ別、2021-2034

- 主要動向

- マイクロコントローラ(MCU)

- センサー

- パワー半導体

- メモリ

- アナログおよびミックスドシグナルIC

- その他

第6章 市場推計・予測:車種別、2021-2034

- 主要動向

- 乗用車

- 小型商用車(LCV)

- 大型商用車(HCV)

第7章 市場推計・予測:用途別、2021-2034

- 主要動向

- パワートレインおよび電動化

- エンジン制御ユニット(ECU)

- バッテリー管理システム(BMS)

- 車載充電器

- その他

- 安全システム

- ADAS(先進運転支援システム)

- アンチロック・ブレーキ・システム(ABS)

- 電子式安定性制御(ESC)

- その他

- 車体電子機器

- ドア、シート、窓の制御

- 照明(LED、アダプティブヘッドランプ)

- HVACシステム

- その他

- シャーシおよびサスペンション

- 電動パワーステアリング(EPS)

- サスペンション制御ユニット

- その他

- インフォテインメントおよびテレマティクス

- オーディオ処理及び増幅器

- GPSおよびナビゲーションシステム

- その他

第8章 市場推計・予測:販売チャネル別、2021-2034

- 主要動向

- OEM

- アフターマーケット

第9章 市場推計・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- ラテンアメリカ

- ブラジル

- メキシコ

- 中東・アフリカ地域

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第10章 企業プロファイル

- 世界の主要企業

- Infineon Technologies AG

- NXP Semiconductors N.V.

- STMicroelectronics N.V.

- Texas Instruments, Inc.

- Renesas Electronics Corporation

- Microchip Technology Inc.

- 地域別主要企業

- 北米:

- Advanced Micro Devices(AMD)

- Analog Devices, Inc.

- Micron Technology

- Onsemi

- 欧州:

- Continental

- Melexis N.V.

- Robert Bosch GmbH

- ZF Friedrichshafen AG

- アジア太平洋:

- Toshiba

- Rohm Co., Ltd.

- Tower Semiconductor Ltd.

- 北米:

- ニッチ/ディスラプター企業

- Allegro Microsystems

- TE Connectivity