|

市場調査レポート

商品コード

1913451

自動車用デファレンシャル市場における成長機会、成長要因、業界動向分析、および2026年から2035年までの予測Automotive Differential Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

カスタマイズ可能

|

|||||||

| 自動車用デファレンシャル市場における成長機会、成長要因、業界動向分析、および2026年から2035年までの予測 |

|

出版日: 2026年01月05日

発行: Global Market Insights Inc.

ページ情報: 英文 230 Pages

納期: 2~3営業日

|

概要

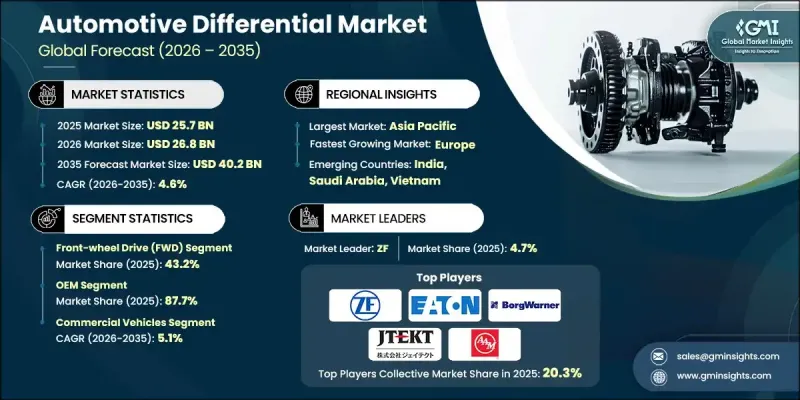

世界の自動車用デフ市場は、2025年に257億米ドルと評価され、2035年までにCAGR 4.6%で成長し、402億米ドルに達すると予測されています。

市場成長は、中産階級消費者の可処分所得水準の上昇と、運輸・物流セクターにおける継続的な拡大に牽引される世界の自動車生産の増加によって支えられています。個人移動手段と貨物輸送への需要増加は、乗用車と商用車の両方の持続的な生産に貢献しており、これが自動車用デフの需要を直接支えています。公共交通システムと物流業務の成長は、バス、バン、トラックの製造をさらに加速させ、市場の勢いを強めています。差動装置メーカーは、変化するパワートレイン構造に対応するため、車両固有のソリューション開発を強化しております。電気自動車やハイブリッド車の普及拡大により、サプライヤーは新たな駆動系要件に適した差動装置システムの再設計と統合を推進しております。技術進歩により、トルク配分、トラクション管理、車両安定性を向上させる電子制御式およびスマート差動装置システムへの注目が高まっております。車両システムがソフトウェア主導型かつセンサー統合型へと進化する中、電子制御式先進差動装置は多様な車種カテゴリーにおいて重要性を増しております。

| 市場範囲 | |

|---|---|

| 開始年 | 2025年 |

| 予測年度 | 2026-2035 |

| 開始時価値 | 257億米ドル |

| 予測金額 | 402億米ドル |

| CAGR | 4.6% |

2025年時点で、前輪駆動セグメントは43.2%のシェアを占め、111億米ドルの収益を生み出しました。前輪駆動構成は、コスト効率とコンパクト設計により広く採用されており、動力伝達部品が単一のアセンブリに統合されています。この構造は製造の複雑さと車両全体のコストを削減し、世界市場での普及を支えています。

2025年時点でOEMセグメントは87.7%のシェアを占め、2035年までに359億米ドルに達すると予測されます。OEMメーカーは、統合された車両生産戦略や進化する性能要件に適合した高品質で用途特化型のコンポーネントを提供できるため、差動装置供給の主要な供給源であり続けています。

米国自動車用デファレンシャル市場は2025年に38億3,000万米ドルに達しました。市場成長は、自動車生産活動の増加と自動車メーカーと部品サプライヤー間の連携強化によって支えられています。自社生産に伴う高い製造コストが、OEMメーカーに専門デファレンシャルメーカーとの提携を促し、カスタマイズされた駆動系ニーズに対応しています。

よくあるご質問

目次

第1章 調査手法

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- コスト構造

- 各段階における付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- 世界の自動車生産台数の増加

- SUVおよび四輪駆動車に対する需要の増加

- オフロード車およびレクリエーション車両セグメントの成長

- 商用車の普及拡大

- 業界の潜在的リスク&課題

- 車両における重量とパッケージングの制約

- 設計と保守における複雑性

- 市場機会

- 電気自動車における電気式差動装置の普及拡大

- 高性能デフに対するアフターマーケット需要の増加

- 新興自動車市場における成長

- 軽量かつコンパクトな差動装置ソリューションの開発

- 促進要因

- 成長可能性分析

- 規制情勢

- 北米

- SAE(自動車技術会)

- FMVSS(連邦自動車安全基準-NHTSA)

- ASTM International

- CSAグループ

- 欧州

- 国連欧州経済委員会(UNECE)規制(ECE)

- ISO(国際標準化機構)

- EN規格(CEN)

- TUV規格・認証

- アジア太平洋地域

- JIS(日本工業規格)

- GB/T規格(中国)

- AIS(自動車産業規格- インド)

- ラテンアメリカ

- ABNT規格(ブラジル)

- NOM規格(メキシコ)

- IRAM規格(アルゼンチン)

- 中東・アフリカ

- GSO規格(湾岸協力会議)

- SASO規格(サウジアラビア)

- SABS規格(南アフリカ)

- 北米

- ポーター分析

- PESTEL分析

- 技術とイノベーションの動向

- 現在の技術動向

- 新興技術

- 価格動向

- 地域別

- 製品別

- 生産統計

- 生産拠点

- 消費拠点

- 輸出と輸入

- コスト内訳分析

- 持続可能性と環境影響

- 環境影響評価

- 社会的影響と地域社会への貢献

- ガバナンスと企業の社会的責任

- 持続可能な金融と投資動向

- 電動化の影響評価

- EV用差動装置の設計上の差異

- E-axleの統合動向

- 電気自動車におけるトルクベクタリング

- 従来型メーカーの転換における課題

- 性能と効率のベンチマーク

- タイプ別差動効率評価

- 耐久性および寿命分析

- 騒音・振動・粗さ(NVH)性能

- 熱管理能力

- 事例研究

- 将来展望と機会

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ地域

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

- 主な発展

- 合併・買収

- 提携・協業

- 新製品の発売

- 事業拡大計画と資金調達

第5章 市場推計・予測:車種別、2022-2035

- オープン・ディファレンシャル

- リミテッド・スリップ・ディファレンシャル(LSD)

- 電子制御式リミテッドスリップデフ(ELSD)

- ロック式ディファレンシャル

- 手動ロック(ドライバー操作式)

- 自動ロック機構(車輪のスリップを感知)

- トルク差動装置

第6章 市場推計・予測:コンポーネント別、2022-2035

- 差動装置

- 差動ケース/ハウジング

- ベアリング及びシール

- 電子制御部品

第7章 市場推計・予測:車両別、2022-2035

- 乗用車

- ハッチバック

- セダン

- SUV

- 商用車

- 軽商用車(LCV)

- MCV

- 大型商用車(HCV)

第8章 市場推計・予測:駆動方式別、2022-2035

- 前輪駆動(FWD)

- 後輪駆動(RWD)

- 全輪駆動(AWD)/四輪駆動(4WD)

第9章 市場推計・予測:推進力別、2022-2035

- 内燃機関(ICE)

- 電気自動車(EV)

- ハイブリッド

第10章 市場推計・予測:販売チャネル別、2022-2035

- OEM

- アフターマーケット

第11章 市場推計・予測:地域別、2022-2035

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- ロシア

- 北欧諸国

- ベネルクス

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- ANZ

- シンガポール

- マレーシア

- インドネシア

- ベトナム

- タイ

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- コロンビア

- 中東・アフリカ地域

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第12章 企業プロファイル

- 世界企業

- ZF

- American Axle &Manufacturing(AAM)

- Dana

- BorgWarner

- GKN Automotive

- Eaton

- JTEKT

- Linamar

- Schaeffler

- Magna

- Hyundai Mobis

- Meritor(Cummins)

- Continental

- NSK

- 地域企業

- Bharat Gears

- Neapco

- Huayu Automotive Systems

- Tata Motors

- Sona Comstar

- AmTech

- Univance

- 新興企業

- Auburn Gear

- Drexler Automotive

- RT Quaife

- Xtrac