|

市場調査レポート

商品コード

1801899

スマート水栓の市場機会、成長促進要因、産業動向分析、2025~2034年の予測Smart Faucet Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| スマート水栓の市場機会、成長促進要因、産業動向分析、2025~2034年の予測 |

|

出版日: 2025年08月14日

発行: Global Market Insights Inc.

ページ情報: 英文 136 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

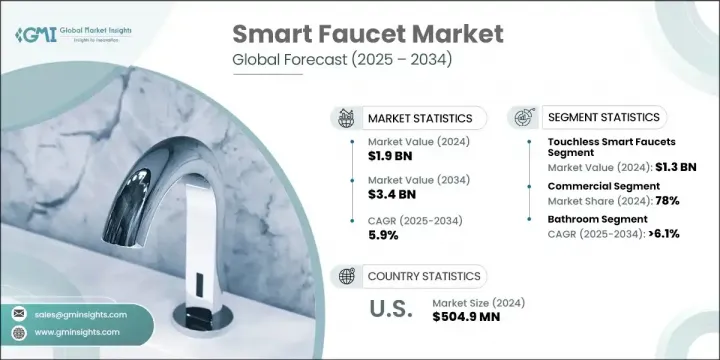

スマート水栓の世界市場規模は2024年に19億米ドルとなり、CAGR 5.9%で成長し、2034年には34億米ドルに達すると予測されています。

この成長を後押ししているのは、水効率をめぐる懸念の高まりと、環境に配慮したソリューションを求める声の高まりです。消費者も企業も同様に、持続可能性の目標をサポートしながら水の浪費を最小限に抑える技術を優先しています。スマート水栓は、ユーザーフレンドリーな制御とインテリジェントな自動化を組み合わせた節水機能を提供し、求められる技術革新となっています。センサーベースのシステム、音声対応コマンド、IoT機能の統合は利便性を高め、拡大するスマートホームのトレンドに合致しています。

需要の高まりは衛生意識の高まりとも関連しており、タッチフリー操作は住宅、商業、ヘルスケア環境全体で重要な機能となっています。これらの蛇口は、物理的な接触を排除することで、より清潔で安全なユーザー体験を提供します。都市化と進行中の建設活動は、近代的な住宅および商業開発におけるスマート水栓の需要を高め続けています。不動産所有者は、建築環境の価値を高めると同時に、資源の節約を支援するプレミアムな技術対応ソリューションにますます注目しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025年~2034年 |

| 開始金額 | 19億米ドル |

| 予測金額 | 34億米ドル |

| CAGR | 5.9% |

タッチレススマート蛇口は、2024年に13億米ドルを生み出し、2034年までCAGR 6.1%で成長すると予測されています。このセグメントは、衛生を第一に考えた設計により市場をリードしており、健康の安全を優先するユーザーにアピールしています。これらのシステムは、モーションセンサーを使用して自動的に水流を作動させるため、物理的な相互作用を排除し、二次汚染を減らすことができます。清潔さが公共空間と私的空間の両方で重要な要素となっている現在、ハンズフリー水栓システムは広く採用されており、市場での継続的な優位性を支えています。

2024年の商業部門のシェアは78%で、2034年までのCAGRは5.8%と予測されています。商業用途のスマート蛇口は、水の使用量を制御し、エネルギー消費量を削減することで、施設の運営コストを削減するのに役立ちます。ホテル、公共トイレ、オフィスビル、病院など、人の出入りが多い空間の事業者は、ユーザーエクスペリエンスを向上させながら効率を高めるためにこれらのシステムを採用しています。これらの蛇口は、水漏れを防ぎ、メンテナンスを最適化し、長期的なコスト削減を実現します。

米国のスマート水栓市場は77%のシェアを占め、2024年には5億490万米ドルを生み出しました。米国の成長は、ホームオートメーションに対する消費者の強い関心、強固なインフラ、有利な規制イニシアチブによって支えられています。スマートホームの高度な統合により、同国は採用の最前線に位置付けられ、住宅所有者はインテリジェントな水設備を接続された生活環境の一部として受け入れています。音声起動、遠隔アプリ・モニタリング、水使用量分析などの機能は、消費者の関心を引き続き高め、市場浸透を強化しています。

スマート水栓の世界市場における主要メーカーは、LIXIL、Delta Faucet、TOTO、Moen、Hansgrohe、Masco、Kohler、Roca Sanitario、ASSA ABLOY、House of Rohl、KWC、Oras、BRIZO Kitchen &Bath、Gessi、Villeroy &Bochなどです。スマート水栓市場のトップ企業は、市場シェアを拡大するため、イノベーション、デザイン、スマートテクノロジーの統合に注力しています。AI、モーションセンサー、音声制御機能への投資が製品開発戦略の中心となっています。また、開発大手各社は、不動産デベロッパー、ホスピタリティチェーン、公共インフラプロジェクトとの提携を通じてブランドの存在感を高めています。製品ラインは、エネルギー効率、節水、設置のしやすさなど、最終消費者と商業購買者の双方に配慮したものが増えています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク&課題

- 機会

- 成長可能性分析

- 将来の市場動向

- テクノロジーとイノベーションの情勢

- 現在の技術動向

- 新興技術

- 価格動向

- 地域別

- タイプ別

- 規制情勢

- 標準とコンプライアンス要件

- 地域規制枠組み

- 認証基準

- ポーターの分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 地域別

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画

第5章 市場推計・予測:タイプ別、2021年~2034年

- 主要動向

- タッチレススマート蛇口

- タッチ対応スマート蛇口

第6章 市場推計・予測:材料別、2021年~2034年

- 主要動向

- メタリック

- プラスチック

- その他

第7章 市場推計・予測:用途別、2021年~2034年

- バスルーム

- 台所

第8章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 住宅用

- 商業用

- ホテル&レストラン

- 病院

- 企業オフィス

- 公衆トイレ

- その他

第9章 市場推計・予測:流通チャネル別、2021年~2034年

- 主要動向

- オンライン

- eコマース

- 企業のウェブサイト

- オフライン

- スーパーマーケット/ハイパーマーケット

- 専門小売店

- その他(個人小売店など)

第10章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第11章 企業プロファイル

- ASSA ABLOY

- BRIZO Kitchen &Bath

- Delta Faucet

- Gessi

- Hansgrohe

- House of Rohl

- Kohler

- KWC

- LIXIL

- Masco

- Moen

- Oras

- Roca Sanitario

- TOTO

- Villeroy &Boch

The Global Smart Faucet Market was valued at USD 1.9 billion in 2024 and is estimated to grow at a CAGR of 5.9% to reach USD 3.4 billion by 2034. This growth is being fueled by rising concerns around water efficiency and the increasing push for eco-conscious solutions. Consumers and businesses alike are prioritizing technologies that help minimize water waste while supporting sustainability goals. Smart faucets have become a sought-after innovation, delivering water-saving features combined with user-friendly control and intelligent automation. The integration of sensor-based systems, voice-enabled commands, and IoT capabilities enhances convenience and aligns with the expanding smart home trend.

The rising demand is also linked to heightened hygiene awareness, with touch-free operation becoming a critical feature across residential, commercial, and healthcare environments. These faucets offer a cleaner, safer user experience by eliminating physical contact. Urbanization and ongoing construction activity continue to elevate demand for smart water fixtures in modern residential and commercial developments. Property owners are increasingly turning to premium, tech-enabled solutions that help conserve resources while also enhancing the value of built environments.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.9 Billion |

| Forecast Value | $3.4 Billion |

| CAGR | 5.9% |

The touchless smart faucets generated USD 1.3 billion in 2024 and is anticipated to grow at a CAGR of 6.1% throughout 2034. This segment leads the market thanks to its hygiene-first design, which appeals to users prioritizing health safety. These systems activate water flow automatically using motion sensors, eliminating physical interaction and reducing cross-contamination. With cleanliness now a critical factor in both public and private spaces, hands-free faucet systems are being adopted widely, supporting their continued dominance in the market.

The commercial sector held 78% share in 2024 and is projected to grow at a CAGR of 5.8% through 2034. Smart faucets in commercial applications help facilities reduce operating costs by controlling water usage and lowering energy consumption. Businesses in high-traffic spaces such as hotels, public restrooms, office buildings, and hospitals are adopting these systems to enhance efficiency while improving user experience. These faucets help prevent leaks, optimize maintenance, and offer long-term cost savings-making them a practical upgrade across commercial operations.

United States Smart Faucet Market accounted for 77% share and generated USD 504.9 million in 2024. Growth in the U.S. is supported by strong consumer interest in home automation, robust infrastructure, and favorable regulatory initiatives. A high level of smart home integration has positioned the country at the forefront of adoption, with homeowners embracing intelligent water fixtures as part of their connected living environments. Features such as voice activation, remote app monitoring, and water usage analytics continue to drive consumer interest and strengthen market penetration.

Key manufacturers in the Global Smart Faucet Market include LIXIL, Delta Faucet, TOTO, Moen, Hansgrohe, Masco, Kohler, Roca Sanitario, ASSA ABLOY, House of Rohl, KWC, Oras, BRIZO Kitchen & Bath, Gessi, and Villeroy & Boch. Top companies in the smart faucet market are focusing on innovation, design, and smart technology integration to expand their market share. Investments in AI, motion sensors, and voice control capabilities are central to product development strategies. Leading players are also strengthening brand presence through partnerships with real estate developers, hospitality chains, and public infrastructure projects. Product lines are increasingly being tailored to offer energy efficiency, water conservation, and ease of installation-catering to both end consumers and commercial buyers.

Table of Contents

Chapter 1 Methodology and scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 By type

- 2.2.3 By material

- 2.2.4 By application

- 2.2.5 By end use

- 2.2.6 By distribution channel

- 2.3 CXO perspectives: strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls & challenges

- 3.2.3 Opportunities

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By type

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Type, 2021 - 2034 ($Billion, Million Units)

- 5.1 Key trends

- 5.2 Touchless smart faucets

- 5.3 Touch-enabled smart faucets

Chapter 6 Market Estimates & Forecast, By Material, 2021 - 2034 ($Billion, Million Units)

- 6.1 Key trends

- 6.2 Metallic

- 6.3 Plastic

- 6.4 Others

Chapter 7 Market Estimates & Forecast, By Application, 2021 - 2034 ($Billion, Million Units)

- 7.1 Bathroom

- 7.2 Kitchen

Chapter 8 Market Estimates & Forecast, By End Use, 2021 - 2034 ($Billion, Million Units)

- 8.1 Key trends

- 8.2 Residential

- 8.3 Commercial

- 8.3.1 Hotels & restaurants

- 8.3.2 Hospitals

- 8.3.3 Corporate offices

- 8.3.4 Public washrooms

- 8.3.5 Others

Chapter 9 Market Estimates & Forecast, By Distribution Channel, 2021 - 2034 ($Billion, Million Units)

- 9.1 Key trends

- 9.2 Online

- 9.2.1 E-commerce

- 9.2.2 Company websites

- 9.3 Offline

- 9.3.1 Supermarkets/hypermarket

- 9.3.2 Specialty retail stores

- 9.3.3 Others (independent retailer etc.)

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($Billion, Million Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 Japan

- 10.4.3 India

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 ASSA ABLOY

- 11.2 BRIZO Kitchen & Bath

- 11.3 Delta Faucet

- 11.4 Gessi

- 11.5 Hansgrohe

- 11.6 House of Rohl

- 11.7 Kohler

- 11.8 KWC

- 11.9 LIXIL

- 11.10 Masco

- 11.11 Moen

- 11.12 Oras

- 11.13 Roca Sanitario

- 11.14 TOTO

- 11.15 Villeroy & Boch